The HDFC Life Smart Protect Plus is a Unit Linked Life Insurance Plan (ULIP) that combines life cover with market-linked investment growth. It offers four plan variants, optional capital guarantee features, flexible premium payment options, and access to 11 fund options depending on the selected variant. Like all ULIPs, it comes with a mandatory 5-year lock-in period.

The plan also includes features such as return of mortality charges, premium allocation charge refunds, fund management charge rebates, and maturity boosters that help reduce the long-term impact of charges.

For example, a 30-year-old paying ₹1 lakh annually for 10 years under a 40-year policy term with ₹1 crore cover may see an effective net return of around 7.01% at an assumed 8% gross return.

Looking for a plan that combines life cover with market-linked wealth creation? HDFC Life Smart Protect Plus is designed to offer both in a single product. However, before buying, it is important to understand how the ULIP works, the charges involved, and whether it delivers better value than simpler alternatives.

This article covers the plan variants, fund options, charges, returns, tax benefits, and eligibility criteria, along with a comparison against separate term insurance and mutual fund investing.

HDFC Life Smart Protect Plus is a ULIP that combines life insurance with market-linked investments. Your premium is used partly for life cover and partly for investment in funds, depending on the plan option and fund choices available to you.

The plan is not a traditional guaranteed-return product. Since it is a ULIP, the investment risk is borne by the policyholder, and the fund value can rise or fall depending on market performance.

Eligibility Criteria for HDFC Life Smart Protect Plus

Criteria

Details

Plan Type

ULIP (Life cover + market-linked investment)

Variants

Level cover, Level cover with capital guarantee, Decreasing cover, Decreasing cover with capital guarantee

Entry Age

Minimum: 0 years (30 days for minors), maximum: 60 years

Maturity Age

Minimum 25 years, maximum 99 years.

Policy Term

25 years to 99 minus age at entry

Premium Payment Term

Limited Pay (5 to 20 years) or Regular Pay

Sum Assured

5-10x Annual premiums (minimum)

Lock-in Period

5 years

Fund Options

The plan has 11 funds overall. However, Options A and C offer access to 9 funds, while the capital guarantee options invest through 2 funds: Capital Growth Fund and Capital Secure Fund

Coverage Type

Individual

This plan may suit investors who are comfortable with market-linked returns, prefer a bundled insurance and investment product, and are willing to stay invested for the long term.

Along with plan features, it is also important to consider the insurer’s claim settlement track record, service quality, and overall reliability. For a more detailed evaluation, you can also explore our review of HDFC Life Insurance.

Key Features of HDFC Life Smart Protect Plus

Life Cover from Day One: Death cover begins from policy inception for adults. For minors, it commences immediately or later, as specified in the policy schedule. If death occurs before the commencement of risk cover, the benefit payable is restricted to the fund value.

Loyalty Additions and Charge Recovery: A portion of charges, such as mortality and premium allocation, is returned to your fund over time, helping improve long-term value.

Flexible Premium Structure: You can choose between Limited Pay and Regular Pay options, depending on how you want to structure your cash flows.

Partial Withdrawals and Top-Ups: After the 5-year lock-in, you can withdraw funds or add top-up investments within defined limits.

Capital Guarantee Options: Under Option B and Option D, the plan guarantees at least the total premiums paid, adjusted for partial withdrawals, at maturity. However, this is not a guaranteed return. If the fund value plus loyalty additions is higher, the higher amount is paid. In exchange, investments are limited to the Capital Growth Fund and Capital Secure Fund, allocation is managed by HDFC Life Insurance, and a 0.50% annual guarantee charge applies.

Tax Efficiency: Premiums are eligible for deductions under Section 80C under the old tax regime. Death benefit payouts to nominees are tax-exempt, while maturity proceeds are tax-free, subject to conditions under Section 10(10D).

Rider Add-Ons: The plan allows riders such as HDFC Life Income Benefit on Accidental Disability Rider, Protect Plus Rider, Health Plus Rider, Waiver of Premium Rider, and LiveWell Rider, subject to eligibility and rider terms.

Flexible Payout Options: You can receive benefits as a lump sum or staggered payouts over up to five years.

CTA

Plan Options Under HDFC Life Smart Protect Plus

Option

Cover Type

Capital Guarantee

Best For

A-Level Cover

Fixed throughout the policy term

No

Those seeking steady cover with higher return potential

B-Level Cover with Capital Guarantee

Fixed throughout the policy term

Yes

Conservative investors want downside protection

C-Decreasing Cover

Reduces after “Level Cover Period”

No

Those with reduced liabilities, like home loans

D-Decreasing Cover with Capital Guarantee

Reduces after the Level Cover Period

Yes

Conservative investors with reduced cover needs

How the Four Plan Options Work

1) Option A: Level Cover

This option keeps your life cover fixed throughout the policy term. It gives you wider control over fund selection and may be better suited for investors who are comfortable with market risk and want higher long-term growth potential.

2) Option B: Level Cover with Capital Guarantee

This option keeps your life cover fixed and adds a capital guarantee at maturity. It may suit conservative investors who want a minimum maturity protection, but the upside may be lower because the insurer controls the fund allocation.

3) Option C: Decreasing Cover

This option starts with a level cover period. After that period, the life cover reduces every year. It may suit people whose financial liabilities are expected to fall over time, such as those repaying a home loan.

4) Option D: Decreasing Cover with Capital Guarantee

This combines decreasing life cover with a capital guarantee at maturity. It may suit conservative investors who want cover aligned with reducing liabilities and also want downside protection on maturity proceeds.

IRR Analysis: What returns can you actually expect?

A 30-year-old opting for Option A (Level Cover) under the HDFC Life Smart Protect Plus with a ₹1 crore sum assured, ₹1 lakh annual premium, 10-year premium payment term, and 40-year policy term may see a projected maturity value of around ₹1.13 crore at an assumed 8% gross return.

However, actual returns are lower once charges are considered. The effective Internal Rate of Return (IRR) works out to roughly 7.01% at the 8% assumption, mainly due to premium allocation, fund management, mortality, and policy administration charges.

Compared to a pure term plan with separate equity mutual fund investments, the long-term corpus could potentially be lower. Still, ULIPs offer benefits such as tax-efficient fund switching, single-product convenience, and a structure that encourages long-term investing discipline.

HDFC Life Smart Protect Plus vs Term Insurance Plus Mutual Funds

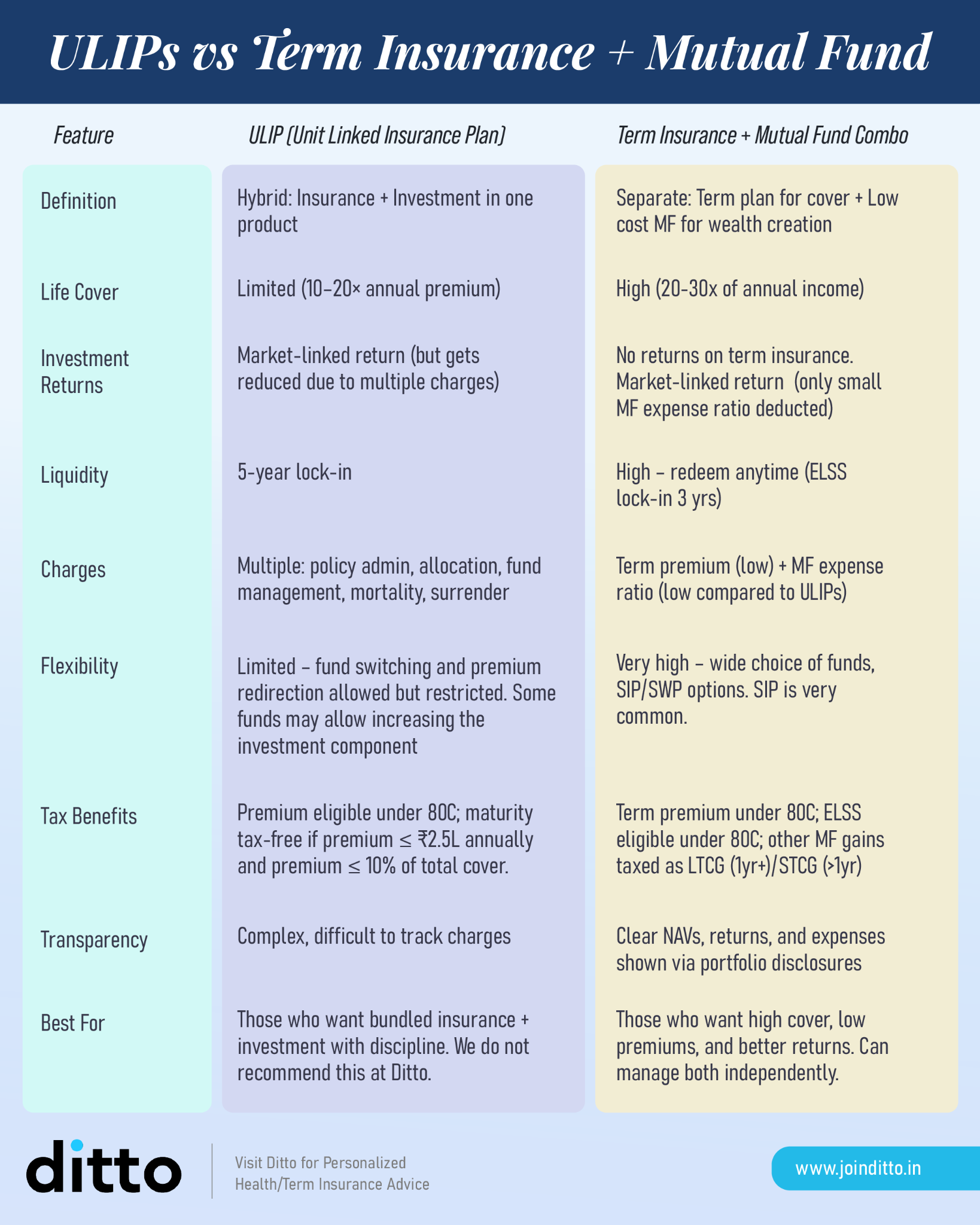

One of the biggest decisions while evaluating the HDFC Life Smart Protect Plus is whether to choose a bundled ULIP or keep insurance and investments separate through a term plan and mutual funds.

A ULIP combines life cover and investing into a single product, while the term insurance plus mutual fund approach separates protection from wealth creation. Both approaches have different trade-offs when it comes to returns, flexibility, liquidity, charges, and convenience.

Take a look at the infographic below to understand the broader difference between ULIPs and term insurance plus mutual funds.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

So, is the HDFC Life Smart Protect Plus actually worth considering? Here’s the honest take:

It is one of the modern ULIPs in the market today. If held consistently until maturity, several charges, such as mortality charges, premium allocation charges, and fund management charges, are partially or fully reversed through loyalty additions and boosters, which help improve long-term returns.

What Works Well:

Backed by HDFC Life Insurance, which has a strong claim settlement track record

Multiple plan options, including capital guarantee variants, give flexibility based on risk appetite

Loyalty additions and charge recoveries help improve returns over the long term

Tax-efficient switching between funds without triggering capital gains tax

What to Watch Out For:

Effective returns (Internal Rate of Return) are lower than headline illustrations due to multiple charges

A 5-year lock-in reduces liquidity in the early years

Investment performance depends on market conditions, with risk borne by the policyholder

Capital guarantee options deliver lower returns due to higher debt allocation

If you value simplicity, want insurance and investment bundled together, or prefer tax-efficient fund switching with optional capital protection, this plan can work. However, if your primary goal is maximizing long-term wealth creation, a combination of a pure term plan and low-cost mutual fund investments may deliver better outcomes. You can also explore our guide on the term plan insurance plans to compare standalone protection options before making a decision.

Frequently Asked Questions

What is HDFC Life Smart Protect Plus, and how does it work?

The HDFC Life Smart Protect Plus is a Unit Linked Insurance Plan that combines life insurance with market-linked investments. Your premium is split into two parts: one provides life cover, and the other is invested in funds such as equity, debt, or hybrid options. Returns depend on how these funds perform over time. The plan also includes features like fund switching, partial withdrawals after five years, and loyalty additions. It is designed for long-term goals like retirement or education, while ensuring financial protection for your family in case of an unfortunate event.

Is HDFC Life Smart Protect Plus worth buying?

This plan can work for individuals who want a bundled product offering both insurance and investment in one structure. It provides flexibility, tax benefits, and loyalty additions that help offset charges over time. However, the effective Internal Rate of Return is lower than headline projections due to multiple charges. For example, net returns may be around 7% at an assumed 8% growth rate. Many financially disciplined investors may achieve better outcomes by combining a pure term plan with mutual fund investments. Ultimately, whether it is worth buying depends on your need for simplicity versus your focus on maximizing long-term returns.

What are the plan options available under HDFC Life Smart Protect Plus?

The plan offers four options: Level Cover, Level Cover with Capital Guarantee, Decreasing Cover, and Decreasing Cover with Capital Guarantee. Level Cover keeps your life cover constant throughout the policy term, while Decreasing Cover reduces it after a chosen period, often aligning with liabilities like loans. Capital Guarantee options ensure that at maturity, you receive at least the total premiums paid, subject to conditions. Options without guarantees provide greater control over fund selection and potentially higher returns, while guaranteed options prioritize safety by limiting investment flexibility and shifting allocation toward lower-risk assets.

What returns can you expect from HDFC Life Smart Protect Plus?

Returns depend on fund performance, but the benefit illustration provides a benchmark. For a typical scenario, a 30-year-old investing ₹1 lakh annually for 10 years may see an effective Internal Rate of Return of around 7.01% at an assumed 8% gross return, and about 3.67% at a 4% assumption. The difference arises due to charges such as premium allocation, fund management, mortality, and policy administration costs. While these returns may be reasonable for a bundled insurance-investment product, they can be lower than what low-cost equity mutual funds or the National Pension System (NPS) may potentially generate over the long term. It is important to evaluate returns based on actual cash flows rather than headline projections.

What charges are applicable in HDFC Life Smart Protect Plus?

The plan includes several charges that impact returns over time. These typically include premium allocation charges deducted upfront, fund management charges applied daily, mortality charges for life cover, and policy administration charges. For capital guarantee options, an additional guarantee charge may apply. While some of these costs are partially offset through loyalty additions in later years, they still reduce the effective return compared to gross fund performance. Understanding these charges is essential because they directly influence the Internal Rate of Return and explain why actual returns are lower than projected figures.

How does HDFC Life Smart Protect Plus compare with term insurance plus mutual funds?

A ULIP like this combines insurance and investment, while the alternative approach separates them. A pure term plan provides life cover at a much lower cost, allowing you to invest the remaining amount in mutual funds. This often results in higher potential returns and better liquidity. However, the ULIP offers convenience, tax-efficient fund switching, and a disciplined investment structure due to its lock-in period. The right choice depends on whether you prioritize simplicity and structure or higher returns and flexibility through separate financial products.

What is the lock-in period for HDFC Life Smart Protect Plus?

The plan comes with a mandatory lock-in period of five years, as per regulatory guidelines for ULIPs in India. During this period, you cannot fully surrender the policy or make partial withdrawals. If you exit early, the fund value is moved to a discontinued policy fund and paid out only after the lock-in ends, subject to applicable charges. After completing five years, you can make partial withdrawals and access your funds with fewer restrictions. This lock-in is designed to encourage long-term investing and prevent premature withdrawals.

What are loyalty additions in HDFC Life Smart Protect Plus?

Loyalty additions are benefits provided by the insurer to reward long-term policyholders. In this plan, they may include refunds of mortality charges, premium allocation charges, and other cost components at specific intervals. These additions are credited as extra units to your fund, which helps improve the overall fund value over time. They become more meaningful in the later years of the policy, especially after the 10th year. While they help offset the impact of charges, they do not eliminate the cost difference compared to direct investments.

Who should consider buying HDFC Life Smart Protect Plus?

This plan is suitable for individuals who want a combination of life insurance and market-linked investment in a single product. It works best for long-term investors who are comfortable with market risk, prefer structured investing, and value tax efficiency. It may also appeal to those who want features like a capital guarantee or do not want to actively manage separate investment and insurance products. However, it may not be ideal for investors whose primary goal is maximizing returns, as separating insurance and investments often delivers better long-term outcomes.

Does HDFC Life Smart Protect Plus offer a capital guarantee?

Yes, the plan offers a capital guarantee under specific options, namely Level Cover with Capital Guarantee and Decreasing Cover with Capital Guarantee. Under these variants, the maturity benefit is at least equal to the total premiums paid, adjusted for any withdrawals. To provide this guarantee, the insurer manages the fund allocation and typically invests more in debt instruments. This reduces downside risk but also limits upside potential compared to equity-heavy options. Therefore, while these variants offer safety, they generally result in lower long-term returns than non-guaranteed options.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.