Overview

Mortality charges in a ULIP are easy to ignore, but they quietly reduce your returns every month. If a large part of your premium goes toward insurance costs instead of investment, it raises an important question. Is a ULIP really the most efficient way to grow your money?

Recent personal finance discussions have raised concerns about ULIP mis-selling and exaggerated return projections. Many “14% return” illustrations often overlook charges like mortality costs, premium allocation fees, and other ULIP charges that reduce the actual amount invested.

In the next few minutes, we will walk you through how mortality charges work in a ULIP, how they are calculated, and how they impact your returns over time.

How Are ULIP Mortality Charges Calculated?

Mortality charges may look small, but they quietly reduce your fund every month. Here is how they are calculated.

Basic Formula

- Annual charge = Mortality rate × sum at risk ÷ 1,000

- Monthly charge = Annual charge ÷ 12

The insurer deducts this amount by canceling units from your fund.

Example

- Sum at Risk: ₹10,00,000

- Mortality Rate: ₹1.50 per ₹1,000 per year

- Net Asset Value (NAV): ₹25

The annual mortality charge works out to ₹1,500, which means a monthly deduction of ₹125. Based on a NAV of ₹25, the insurer cancels 5 units from your fund for that month, reducing your overall investment value slightly.

Note: This is a broad method. Always check your policy document, as insurers must clearly state how charges are calculated and applied.

Case Scenarios

Here are two scenarios that show mortality charges as a percentage of the sum assured.

Scenario: Type I ULIP

Note: The above table assumes a ULIP where the death benefit is the higher of the sum assured or fund value, with a sum assured of ₹10 lakh and an assumed mortality charge rate of ₹2 per ₹1,000 of the sum at risk annually, equivalent to 0.20% per year.

In a Type I ULIP, the insurer’s risk reduces as the fund value grows. As a result, mortality charges can fall sharply over time, from around 0.18% of the sum assured in the initial years to nearly 0.03% later. In some cases, charges will become zero if the fund value exceeds the sum assured.

Scenario: Type II ULIP

Note: The above table assumes a ULIP where the death benefit equals the sum assured plus the fund value, with a sum assured of ₹10 lakh and an assumed mortality charge rate of ₹2 per ₹1,000 of sum at risk annually.

Key Difference

Therefore, a 0.20% mortality charge may look small, but its impact adds up over time. Insurers deduct it each month by canceling units from your ULIP fund. This leaves less money invested for future growth. Mortality charges also rise with age, which can significantly increase long-term costs.

Note: Some sales pitches may focus on high historical or assumed returns without clearly explaining the charges involved. However, the official benefit illustration remains mandatory. It clearly discloses all charges and shows the net yield based on the IRDAI -prescribed 4% and 8% gross return scenarios. This ensures transparency and helps you in making a more informed comparison.

Why Does the Insurer Deduct Units Instead of Charging an Extra Price?

Factors That Affect Mortality Charges in ULIP

- Age: This is the most important factor. Mortality charges rise as you grow older because the risk of death increases. Insurers price this per ₹1,000 of sum at risk, so even small age differences can impact long-term costs.

- Sum at Risk: This is the gap between your sum assured and fund value. A larger gap means a higher risk for the insurer, leading to higher charges. Fund growth over time can gradually reduce this cost.

- Death Benefit Design: Plans that pay both sum assured and fund value carry higher insurer risk than plans that pay the higher of the two. This structure usually results in higher mortality charges over the policy term.

- Sum Assured Multiple: Regulations set minimum cover levels based on your premium and age. You cannot reduce coverage below this limit just to lower charges. This ensures a minimum level of protection is always maintained.

- Health and Underwriting Class: Your medical history, lifestyle habits like smoking, and job risk affect pricing. Higher perceived risk leads to additional loading on mortality charges, which increases the overall cost of the policy.

- Riders and Additional Covers: Adding riders like accidental death or critical illness increases overall cost. These charges are usually deducted monthly by canceling units, which reduces your investment value over time.

- Partial Withdrawals: Withdrawals can change the sum at risk and affect how death benefits are calculated. In some cases, recent withdrawals may reduce the payout, which can affect how mortality charges are applied.

- Settlement Option After Maturity: If you choose to receive maturity proceeds over time instead of a lump sum, the policy may continue with a small risk cover. Mortality charges apply during this period, which slightly reduces payouts.

Does the Sum Assured Affect Mortality Charges?

How to Reduce Mortality Charges in Your ULIP

Buy Early

Start your ULIP at a younger age to enter at lower mortality rates. Since charges increase with age, an early start helps keep costs lower throughout the policy term and improves overall efficiency.

Use ULIP for Investment, Not Heavy Cover

ULIPs work best as long-term investment tools with basic life cover. If you load them with high protection needs, mortality charges rise. Avoid taking very high cover within a ULIP just for comfort, as it increases charges. At the same time, do not go below the required limits. A separate term plan provides broader coverage more efficiently.

Choose the Right Death Benefit Option

The “higher of sum assured or fund value” option usually reduces charges over time as your fund grows. The “sum assured plus fund value” option gives better cover but increases the insurer’s risk and your cost.

Add Riders Only When Needed

Riders provide extra protection but come at a cost. If charges are deducted through unit cancellation, they reduce your fund value each month. Add only those riders that you truly need.

Maintain Health and Disclose Honestly

A good health profile helps you avoid extra mortality loading. Always disclose medical details truthfully, as hiding information can lead to claim rejection later.

Check the Benefit Illustration Carefully

Do not focus only on projected returns. Review the full benefit illustration to understand charges, net yield, and how they impact your long-term returns and final maturity value.

Compare Mortality Charge Tables

Different ULIPs can have different charge structures. Always review the mortality charge table in the policy document.

Having said that, the most effective way to avoid mortality charges is not to opt for a ULIP at all.

Note: Mortality charges can continue even after ULIP maturity if you choose the settlement option instead of withdrawing funds immediately, since a minimum life cover may still remain active during that period.

Did You Know?

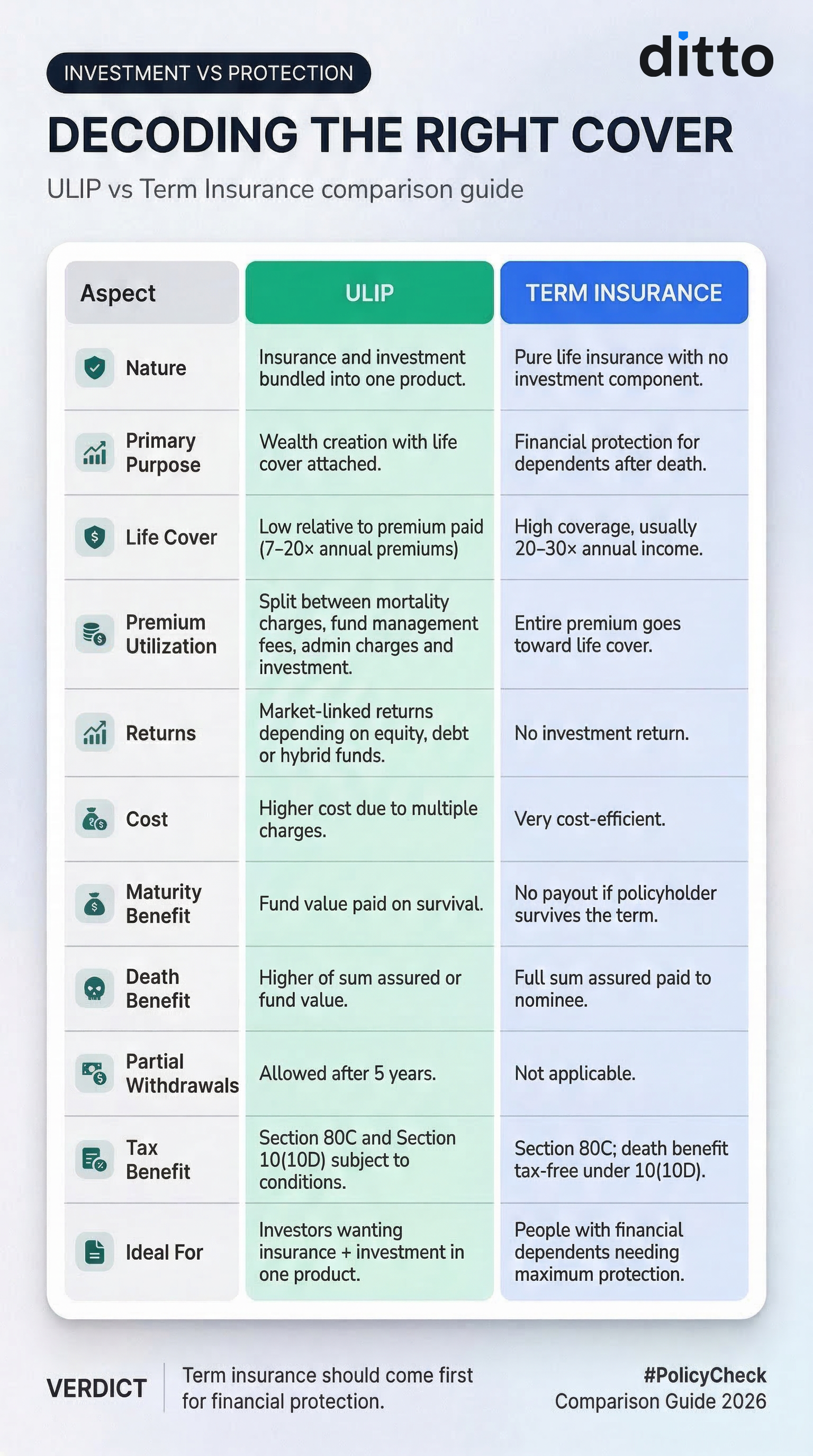

ULIP vs Term Insurance: Which Is Better?

From a protection perspective, term insurance offers significantly higher life cover at a much lower cost. For example, an Axis Max Life ULIP premium of ₹1 to ₹2 lakh a year may provide around ₹20 lakh cover, while a pure term plan such as Axis Max Smart Term Plan Plus can offer ₹2 crore or more cover for roughly ₹18,000 to ₹20,000 annually. The premiums remain fixed for the entire policy term.

From an investment perspective, ULIPs include multiple charges that can reduce long-term returns. In many cases, low-cost options such as index funds or the National Pension System (NPS) may deliver better value over time.

The infographic below clearly explains the difference.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Mortality charges may look small, but they steadily reduce your invested base and limit long-term growth. Over time, this creates a silent drag that most investors underestimate. If your goal is strong protection and efficient wealth creation, combining insurance and investment into a single product often works against you.

A simpler approach is to separate insurance and investment. Take a pure term plan for life cover and invest the premium difference in financial instruments that offer better return potential. You can choose between suitable options such as mutual funds, the National Pension System (NPS), and Fixed Deposits (FDs) based on your risk appetite, investment tenure, liquidity needs, and tax goals. If you need strong life cover, explore our guide on the best term insurance plans that match your long-term financial goals and family needs.

Frequently Asked Questions

Last updated on: