Unit-Linked Insurance Plans (ULIPs) involve several charges that affect your market-linked returns, including policy administration, premium allocation, fund management, mortality, surrender, switching, etc.

While some charges are deducted upfront, affecting the total amount invested, others are deducted throughout the policy term.

In this guide, we break down ULIP charges, what they are, how they affect your policy, and whether there are better insurance and investment options out there. It’s perfect for buyers looking for a ULIP charges list, helping you make more informed decisions before choosing or comparing the plans.

If you’ve ever come across a ULIP, you were probably impressed by the insurance + investment two-in-one combo. It sounds neat, but in reality, these plans can be more complicated than they first appear.

According to the IRDAI Annual Report for FY 2024-25, life insurers recorded 26,667 complaints related to Unfair Business Practices (UFBP), a 14% increase from the previous year. These include cases where products are misrepresented, returns are overstated, or buyers feel pressured to purchase. ULIPs have historically ranked among the most-cited products in such complaints.

Why? Because ULIP plan charges aren’t always obvious upfront, and they can quietly reduce your returns over time if you don’t understand how they work.

To see how this plays out in practice, let’s take a closer look at the different ULIP charges and their impact.

Are you confused between a ULIP and term insurance? Book a call or chat on WhatsApp with our IRDAI-certified advisors.

Types of ULIP Charges You Must Know

Charge

What It Is

When It's Deducted

Premium Allocation Charge

To cover agent commission, underwriting, and distribution costs.

At every premium payment (higher in earlier years).

Fund Management Charge (FMC)

For investing your money in market-linked assets. It’s like the expense ratio in mutual funds, except ULIPs charge more.

Daily, before NAV is calculated (so you never get to see it as a direct deduction).

Policy Administration Charge

A flat fee simply to keep your policy active.

Charged monthly by canceling units from your fund.

Mortality Charge

The actual price of your life insurance cover inside the ULIP. The older you are, the higher this gets.

Charged monthly by canceling units from your fund.

Surrender/Discontinuance Charge

A penalty the insurer applies if you exit the policy before completing the 5-year lock-in. It's meant to discourage early exits and recover the insurer's upfront costs.

On premature surrender or if you stop paying premiums mid-lock-in.

Fund Switching Charge

ULIPs let you move your money between equity, debt, and balanced funds based on your risk appetite. Most insurers give you 4-6 free switches a year. After that, each switch costs a small fee.

Per switch, once your free annual limit is exhausted.

Partial Withdrawal Charge

After the 5-year lock-in, you can withdraw a portion of your funds without surrendering the entire policy. Some insurers charge a small fee for this convenience.

At the time of each partial withdrawal.

Top-Up Premium Charge

If you want to invest extra money over and above your regular premium (like a one-time lump sum), the insurer takes a small percentage off that additional amount before investing it.

On each top-up payment.

Miscellaneous/Alteration Charge

A flat fee for making structural changes to your policy mid-term, like increasing your sum assured, changing your premium payment mode, or switching from annual to monthly payments.

At the time of each alteration.

Out of the above-mentioned ULIP charges, the ones that impact you the most are:

Premium Allocation Charge

This charge tends to be higher in the first few years and reduces over time. So if you're paying ₹1 lakh a year and the allocation charge is 5%, only ₹95,000 actually gets invested in year one.

Fund Management Charge

For context, direct mutual and index funds typically charge 0.1% to 0.7%, and NPS charges even less. So ULIPs are more expensive in terms of fund management.

Policy Administration Charge

It might seem small (say ₹100 per month), but over 20 years, it adds up.

Mortality Charge

Unlike a term insurance plan, where your premium stays fixed for the entire duration, mortality charges in a ULIP go up every year as you get older. It's calculated on your "sum at risk." The sum at risk equals the fund value minus the sum assured.

How ULIP Charges Impact Your Returns

Let's look at a real-world example using a standard ULIP illustration.

For an annual premium of ₹1 lakh with a policy term of 20 years, the total money you put in is ₹20 lakh. Let’s assume the fund grows at 8% gross returns per year.

After all charges, your net return could be between 5.8% and 6.6% per annum. That's a reduction of roughly 1.4% to 2.2% every year. Now let's put that in perspective:

Net Return (After Charges)

Maturity Value

No charges (hypothetical scenario)

₹45.8 lakh

6.6% (low-charge ULIP)

₹39.3 lakh

5.8% (high-charge ULIP)

₹36 lakh

In a high-charge ULIP at 8% gross, you lose ₹9.8 lakh purely to charges, which is nearly 50% of your premiums.

Note: Charges vary by insurer, plan, age, premium, sum assured, policy term, fund, riders, and benefit structure.

Premium Allocation Charge: Cannot exceed 12.5% of annualized premium in any policy year.

Policy Administration Charge: IRDAI mandates that this charge cannot exceed ₹500 per month.

Fund Management Charge: Capped at 0.50% per annum for discontinued policy funds and 1.35% of the fund value per annum for others.

Surrender/Discontinuance Charge: IRDAI caps discontinuance charges through a year-wise table. The charge is highest in the early policy years, subject to rupee limits, and becomes nil from the 5th policy year onward.

Front-loading restriction: Charges must be evenly distributed during the lock-in period, meaning insurers cannot pile all the charges in the early years.

Overall Net Reduction in Yield (RIY): The difference between what your ULIP fund’s gross earnings are and what actually reaches you after all charges are deducted. For example, if the fund grows at 8% but you effectively earn 5.8%, the RIY is 2.2%. IRDAI caps this number on a sliding scale to prevent insurers from loading excessive charges. For example, the maximum reduction in yield is 3.00% at policy year 10 and 2.25% from policy year 15 onward.

How to Minimize ULIP Charges

01

Compare the Fund Management Charge First

This charge compounds most aggressively because it's applied to your entire growing corpus, not just the premium. If all other features are the same across two ULIPs, choose the one with a lower FMC. Even a 0.30% difference can translate into lakhs in expenses over 20 years.

02

Choose a Plan with Zero or Low Premium Allocation Charges

Many newer ULIPs, especially online ones, have reduced or zero allocation charges. This means more of your money gets invested from day one.

03

Stick to the Full Tenure

Surrender charges apply for the first 5 years, and discontinuance funds earn very limited returns. If you start a ULIP, plan to stay for the full term.

04

Look for Return of Mortality Charges (RoMC) ULIPs

If you're comparing two similarly priced ULIPs, the one with ROMC is objectively better. It means all the mortality charges come back to you at the end.

05

Read the Benefit Illustration Before Buying

Insurers are required to show you a benefit illustration with returns projected at 8% and 4%. Look at your fund's value after charges in years 10 and 20. That number tells the real story.

06

Ask for the Net Yield or IRR

Ask your advisor, “What is the internal rate of return if I stay invested for 20 years at an 8% gross return?" If they can't or won't answer that, walk away.

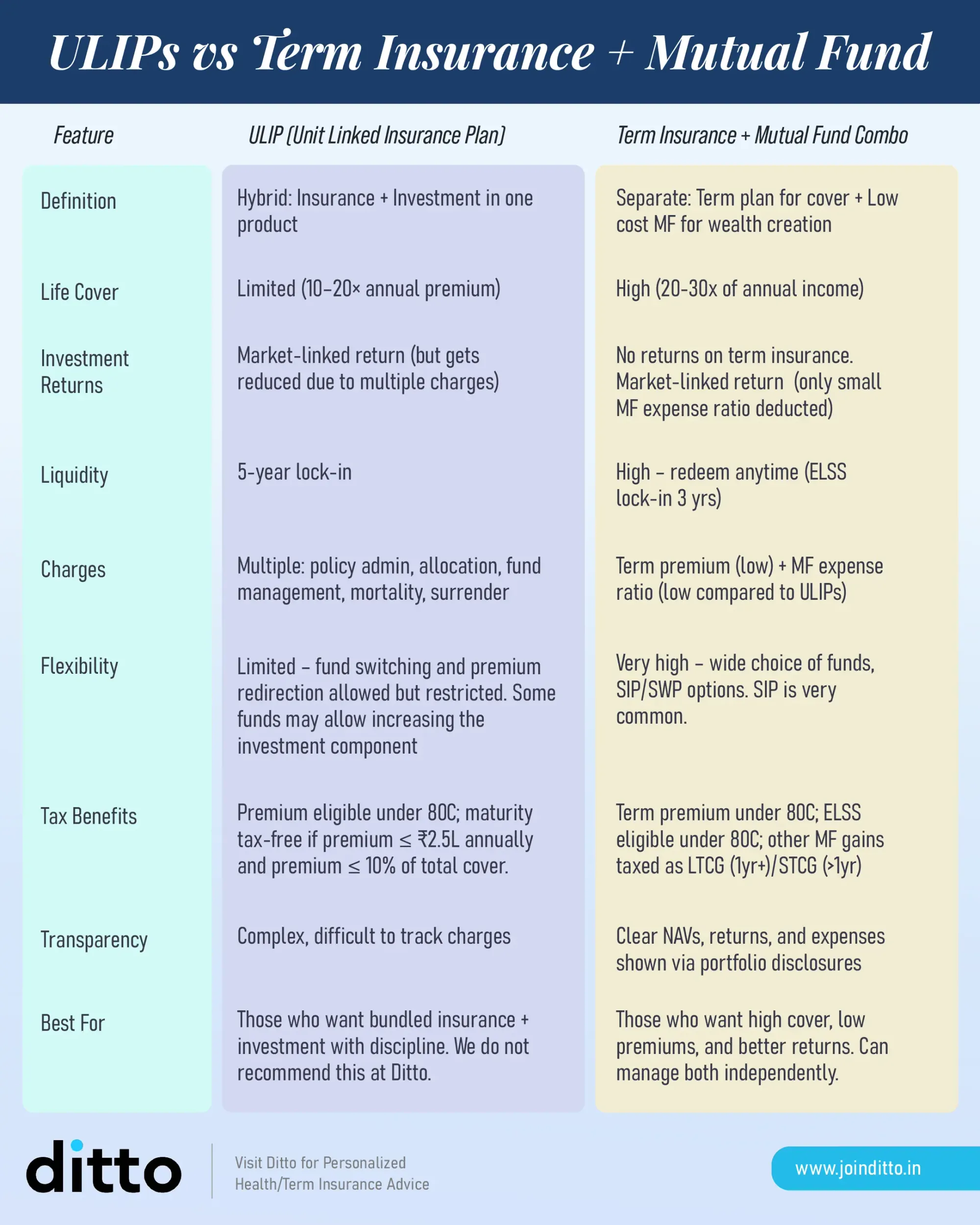

A Smarter Alternative: Term Insurance + Separate Investments

ULIPs exist because, in theory, one product doing two jobs sounds convenient. In practice, it means you're paying for both, and neither comes at the best price. The best way to avoid charges is to avoid ULIPs altogether.

Instead:

Buy a term insurance plan for your life cover. A ₹1 crore term cover for a healthy 30-year-old costs roughly ₹12,000 to ₹14,000 a year. The premium is fixed for the entire duration. No mortality charge increases with age. No complex charge structure. You can check our detailed guide on the best term insurance plans in India to find the right pick for you.

Invest the rest in direct mutual funds or the National Pension System (NPS). A direct equity mutual fund charges 0.1% to 0.7% in expenses. NPS charges even less, around 0.09% for equity schemes. In comparison, ULIP charges are massive.

This strategy works pretty well for disciplined, self-directed investors.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

ULIPs combine insurance and investment, but that convenience comes at a cost. Multiple charges in ULIP, ranging from fund management to mortality and administration, can reduce your effective returns by 1.4% to 2.2% annually. Even with caps set by the IRDAI, the long-term impact can run into lakhs. A better alternative to investing in ULIPs is to buy a plan from the best term insurance companies in India and invest separately in mutual funds.

Frequently Asked Questions

What are ULIP charges?

ULIP charges are the fees deducted from your premium or fund value throughout the policy term of a Unit-Linked Insurance Plan. They include the premium allocation charge, fund management charge, policy administration charge, mortality charge, and surrender/discontinuance charge, among others. Some are deducted upfront before the investment happens, while others are deducted periodically. Together, they silently compound the cost. Understanding all charges in a ULIP before buying is critical because, at an assumed 8% gross return, your net returns after all ULIP charges can fall to just 5.8%- 6.6%, depending on the plan.

Do ULIPs have tax benefits?

Unit-Linked Insurance Plans no longer enjoy the strong tax advantages they once had. Under the 2021 Finance Act, policies with annual premiums exceeding ₹2.5 lakh no longer qualify for the Section 10(10D) tax exemption, and their maturity gains are now taxed as capital gains. Additionally, the 2023 budget made the new tax regime the default, reducing the relevance of Section 80C deductions for many taxpayers. As a result, ULIPs now face standard investment taxation, making them less tax-efficient compared to earlier years.

What is the Fund Management Charge (FMC) in a ULIP?

The Fund Management Charge (FMC) in a ULIP is the annual fee the insurer charges for managing your investments in market-linked assets. It works like the expense ratio in mutual funds. Under IRDAI Regulations 2024, the FMC is capped at 1.35% per annum of fund value. Alternatively, direct mutual funds typically charge 0.1%- 0.7%, while the National Pension System (NPS) charges as little as 0.09% for most schemes.

Are fund boosters in ULIPs actually useful for long-term returns?

Fund boosters and guaranteed additions in ULIPs may sound appealing, but they offer limited real value over time. These benefits are usually one-time credits of about 1% to 3% of the fund value, given at fixed intervals. Meanwhile, charges like fund management and mortality costs are deducted regularly and compound over a long period, such as 20 years. This continuous deduction often outweighs the small periodic boosts, meaning these features do not significantly improve overall returns for most investors.

What is the mortality charge in a ULIP?

The mortality charge in a ULIP is the actual cost of the life insurance cover inside the plan. Unlike a term insurance premium that stays fixed for the entire duration, the mortality charge in a ULIP increases every year as you age. It is calculated on the "sum at risk," which is the sum assured minus your current fund value. This charge stops once your fund value exceeds the sum assured. Some newer ULIPs also offer Return of Mortality Charges (ROMC), in which all mortality charges deducted during the term are refunded at maturity.

What does IRDAI say about ULIP charges?

IRDAI has set strict caps on ULIP charges under its Insurance Products Regulations 2024. The premium allocation charge cannot exceed 12.5% per year. The fund management charge is capped at 1.35% per annum. The policy administration charge cannot exceed ₹500 per month. Surrender/discontinuance charges become nil from the 5th policy year onward. There is also a cap on the overall net reduction in yield: a maximum of 3.00% at policy year 10, and 2.25% from year 15 onward. These regulatory caps exist to protect investors from excessive fee deductions over the policy term.

How much do ULIP charges reduce your actual returns?

ULIP charges can significantly reduce your maturity value. With an annual premium of ₹1 lakh over 20 years at 8% gross returns, a high-charge ULIP may deliver only 5.8% net, while a low-charge ULIP may deliver around 6.6%. That is a reduction of 1.4% to 2.2%. In rupee terms, a high-charge ULIP yields about ₹36 lakh at maturity versus ₹45.8 lakh without any charges: a loss of ₹9.8 lakh, which is nearly 50% of all premiums paid.

What is the surrender charge or discontinuance charge in ULIP?

The surrender/discontinuance charge is a penalty you pay if you exit a ULIP before completing the mandatory 5-year lock-in, or if you stop paying premiums during this period. It is highest in the early policy years and is designed to recover the insurer's upfront distribution costs. Under IRDAI Regulations 2024, the charge follows a year-wise cap structure and becomes nil from the 5th policy year onward. The funds in a discontinued policy earn very limited returns during this period. Starting a ULIP without a clear plan to stay invested through the full term is a costly mistake.

Are ULIP charges higher than mutual funds?

Yes, ULIP charges are generally significantly higher than those of direct mutual funds. The ULIP fund management charge alone is capped at 1.35% per annum under IRDAI rules, while direct equity mutual funds typically charge 0.1% to 0.7%. NPS charges as little as 0.09% for government schemes. Beyond FMC, ULIPs add layers of premium allocation charges, mortality charges, and policy administration charges, none of which exist in mutual funds. This multi-layered cost structure is why net returns from a ULIP are typically 1.4%-2.2% lower than the gross return, even after IRDAI-mandated caps.

What is the Return of Mortality Charges (ROMC) in a ULIP?

Return of Mortality Charges (ROMC) is a feature in some newer ULIPs where all mortality charges deducted during the policy term are refunded as a lump sum at maturity. Normally, mortality charges are a permanent cost as they pay for the life insurance cover embedded in the ULIP and are never recovered. With ROMC, these charges come back to you at the end of the policy. If you are comparing two similarly priced ULIPs, the one with ROMC is the better deal, since it effectively makes your life insurance cover free over the long term.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.