Buying term insurance in India means matching your cover to your income and liabilities, comparing plans across insurers for features and riders, submitting KYC and medical details, and paying the premium online. Coverage of ₹1 crore for a healthy 25-year-old non-smoker starts around ₹800– ₹ 1,100 per month.

Steps to Buy Online

Calculate Cover: Use an online calculator to size your cover against income, loans, and goals (commonly 10–25x annual income).

Compare Plans: Check features and riders across insurers like Axis Max Life, HDFC Life, and ICICI Prudential.

Submit Details and Pay the Premiums: Provide accurate medical and lifestyle information to avoid claim rejections, and pay the premium.

Complete Medical Checks: Higher covers require tests; lower covers may qualify for no-medical plans.

Key Benefits & Features

Affordable, High Coverage: Especially when bought early.

Tax Savings: Deductions under Section 80C, with tax-free payouts.

Riders: Critical Illness and Waiver of Premium add extra protection.

India's life insurance penetration stood at just 2.7% of GDP in FY 2024-25, according to IRDAI's annual report. That means an overwhelming majority of Indian families have no financial safety net if the breadwinner passes away unexpectedly.

If something happens to you tomorrow, your family does not just lose you. They lose your income, their ability to pay the home loan EMI, fund your child's education, and manage day-to-day expenses.

This is exactly why buying term insurance is one of the most important financial decisions you can make. And the best time to do it was yesterday.

This guide covers term insurance basics, Ditto’s top 2026 picks, key buying tips, steps for an online purchase, and the required documents.

Need help to buy term insurance online? Book a free call or chat on WhatsApp with a Ditto advisor who can guide you through each step.

What Is Term Insurance?

Term insurance is the simplest form of life insurance. You choose a cover amount and a policy term, which means the number of years your family stays protected. If you pass away during this term, your nominee gets the sum assured.

Imagine you are 28, recently married, and have a ₹50 lakh home loan. You buy a ₹2 crore term plan for 30 years. If something happens to you in year 10, your family gets ₹2 crore. This can help them repay the loan, manage living expenses, and fund future goals, such as your child’s education.

Key Features of a Term Plan:

Fixed premiums throughout the policy tenure, so the earlier you buy, lower the premium you lock in

Let’s take a look at the infographic below to understand how term insurance works.

Ditto's Pick for Best Term Insurance Plans in 2026

At Ditto, we evaluate every plan through our own policy and insurer rating framework, which assesses insurer reliability (claim settlement ratio, amount settlement ratio, solvency, complaint volumes) and policy quality (features, rider flexibility, premium competitiveness).

It balances important features, competitive pricing, and strong performance metrics. The plan offers optional riders such as critical illness cover for up to 64 illnesses and a waiver of premium. Along with in-built benefits like terminal illness payout of up to ₹1 crore, cover continuance, instant payout at claim intimation, and health management services through the Axis Max Life app.

Axis Max Life

Smart Term Plan Plus

4.7

Overall Rating

Insurer Rating

5.0/5

Customer Service

5.0/5

Feature Rating

4.1/5

Premium Rating

5.0/5

02

HDFC Life

Click2Protect Supreme Plus

It is a polished, feature-heavy term plan for buyers who value reliability, service, and flexibility over the cheapest premium. The plan offers useful riders such as waiver of premium, critical illness cover, and income benefit payout on disability. It also has built-in benefits such as life-stage cover boosts, premium break, Smart Exit, instant partial payout, and wellness services. It is a strong choice if you are comfortable paying a slightly higher premium for a smoother long-term experience.

HDFC Life

Click2Protect Supreme Plus

4.4

Overall Rating

Insurer Rating

4.5/5

Customer Service

5.0/5

Feature Rating

4.4/5

Premium Rating

3.0/5

03

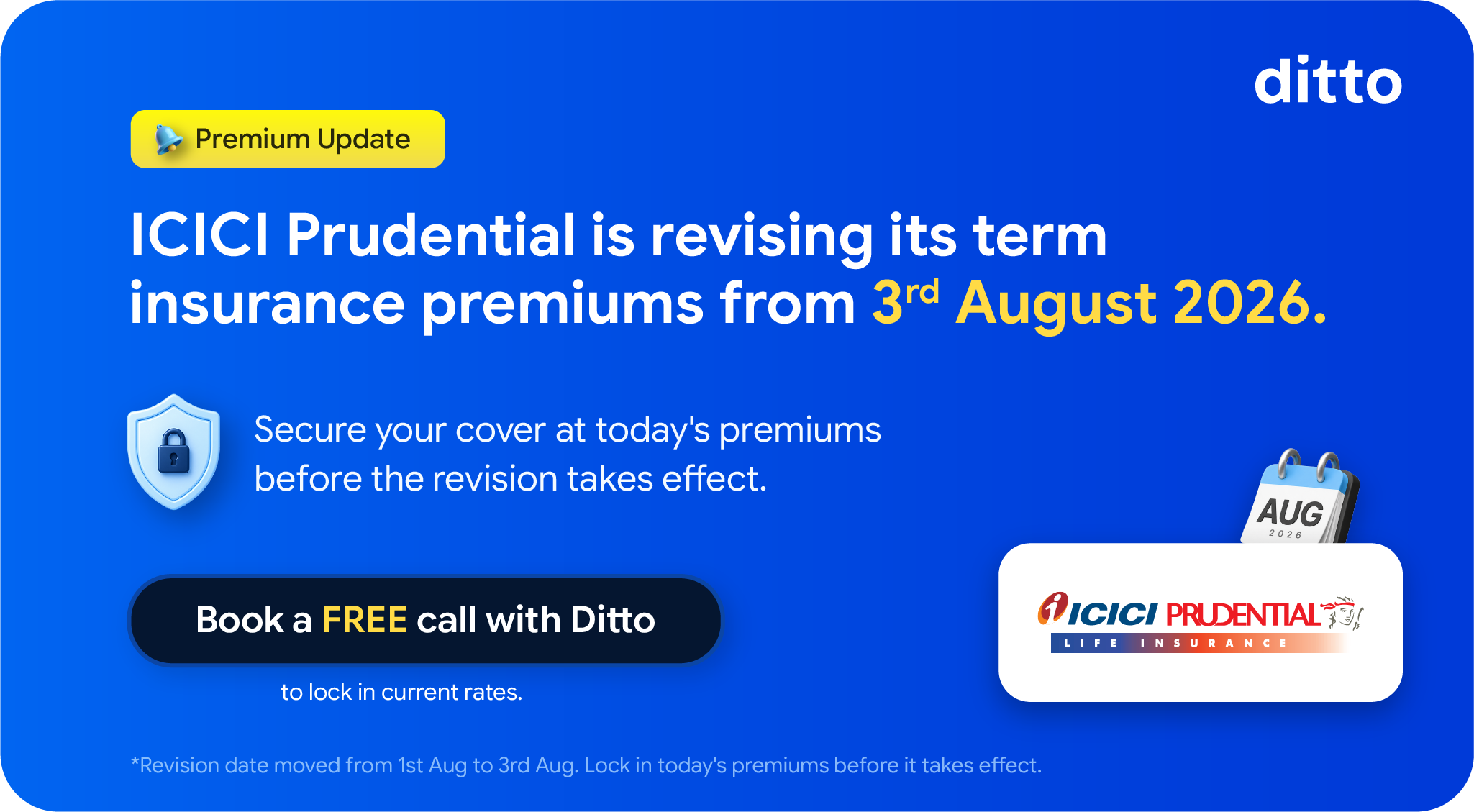

ICICI Prudential

iProtect Smart Plus

It is a simple term plan for buyers who want affordability without sacrificing important features. The plan lets you increase cover during major life events like marriage, childbirth, or home loan disbursement, and also offers smart exit, premium break, instant partial payout, and flexible payout options for nominees. This plan suits salaried buyers who want a trusted brand, decent features, and strong value.

ICICI Prudential

iProtect Smart Plus

4.3

Overall Rating

Insurer Rating

4.4/5

Customer Service

5.0/5

Feature Rating

3.8/5

Premium Rating

5.0/5

04

Bajaj Life

eTouch II

It is a simple, competitively priced term plan that covers the essentials well. The plan offers built-in benefits, including a terminal-illness payout, a waiver of premium for accidental disability and terminal illness, an early-exit value, and health management services. It also has optional riders such as a premium break and a lump-sum payout upon diagnosis of a listed critical illness. This is a good fit if your priority is keeping premiums low while still getting a reliable and reasonably feature-rich policy.

Bajaj Life

eTouch II

4.2

Overall Rating

Insurer Rating

4.4/5

Customer Service

5.0/5

Feature Rating

3.4/5

Premium Rating

5.0/5

05

Aditya Birla Sun Life

Super Term Plan

It offers optional accelerated critical illness cover for 42 illnesses, terminal illness payout, accidental total and permanent disability premium waiver, life-stage flexibility, cover continuance, early exit value, and fast partial payout upon claim intimation. It works best for buyers who want flexibility and built-in illness protection without adding too many separate riders.

Aditya Birla Sun Life

Super Term Plan

4.0

Overall Rating

Insurer Rating

3.7/5

Customer Service

5.0/5

Feature Rating

4.3/5

Premium Rating

5.0/5

Talk to an expert today and find the right insurance for you.

For the above example, we’ve considered healthy, non-smoking, salaried individuals living in a tier-1 city such as Delhi (pincode: 110010), covered for a sum assured of ₹2 crore until age 65. The premiums are indicative and can vary based on your age, health conditions, lifestyle choices, and underwriting decisions.

Why Is Buying Term Insurance Important in 2026?

Premiums Have Been Rising

Over the years, premiums have gradually increased due to higher demand, richer plan features, medical inflation, and evolving underwriting norms. Post-COVID-19, this rise became more noticeable as insurers reassessed mortality trends, so delaying by even a year could mean paying more for the same cover.

Financial Responsibilities Are Growing Faster

Home loan EMIs, dependents, and education costs are all rising. A ₹1 crore cover that worked in 2015 may fall short today for metro-based primary earners.

Health Conditions Are Being Detected Earlier

Routine checkups now flag issues like pre-diabetes, blood pressure, or cholesterol much earlier. Once diagnosed, insurers may increase your premium or restrict your coverage, so buying early helps lock in your premium.

Buying Term Insurance Online Has Become Simpler

Digital KYC, online medical forms, and paperless onboarding have made term insurance easier to buy. Many standard profiles are now issued faster, sometimes almost instantly.

Ditto’s Expert Insights on Buying Term Insurance in India

Buy Early and Buy Young

Term insurance is cheaper when you buy it young and healthy because insurers price your premium based on your age, health, and risk profile at the time of purchase. Waiting until later may mean higher premiums, stricter underwriting, or even difficulty getting adequate cover if health issues develop.

Most People Underestimate How Much Cover They Need

Many buyers choose a round number, such as ₹1 crore, because it sounds large. But the right cover depends on your age, expenses, loans, coverage duration, dependents, and future goals. Use Ditto’s term insurance cover calculator to estimate your actual need instead of guessing.

The Cheapest Plan Is Rarely the Best Plan

A low premium should not be your only filter. Saving ₹2,000 a year means little if the insurer handles claims poorly or provides poor service. Your family will deal with the insurer at the worst possible time, so reliability matters more than a small difference in premium. Check out our detailed guide on the best term insurance companies to find a reliable insurer.

Do Not Depend Only on Corporate Cover

Your employer-provided life cover may feel convenient, but it is usually limited and tied to your job. If you switch jobs, lose employment, or take a career break, this cover may stop. A personal term insurance plan ensures your family has independent protection that continues regardless of where you work.

Riders Should Be Chosen Carefully

Critical illness and waiver of premium riders each solve a different problem. Adding every rider can inflate your premium without adding meaningful value. Choose riders in term insurance based on your occupation, lifestyle, and existing emergency fund and health insurance cover.

Disclosure Is Everything

This is one of the biggest mistakes buyers make. Do not hide health conditions, family history, smoking, or occasional tobacco use. If the insurer later finds material non-disclosure, they can reject the claim, so honest disclosure protects your family more than any plan feature.

Discuss the Plan With Your Spouse and Inform Nominees

Discuss the cover amount with your spouse and inform your nominees about the policy, insurer, claim process, and where the documents are stored so they are not left confused during an already difficult time.

Benefits of Buying Term Insurance

Let’s take a look at the infographic below to understand the benefits of buying a term insurance plan.

Things to Keep in Mind Before You Buy Term Insurance

01

Evaluate the Insurer, Not Just the Plan

Check the insurer’s 3-year average Claim Settlement Ratio (CSR), Amount Settlement Ratio (ASR), and solvency ratio. Ideally, CSR should be above 97%, ASR above 90%, low complaints volume (less than 20 per 10,000 claims), and solvency above the IRDAI-mandated 1.5x. A good insurer with average features is better than a feature-rich plan from a weak insurer.

02

Choose the Right Sum Assured

At Ditto, we suggest choosing a cover based on your expenses, liabilities, dependents, and future goals. Two people with the same income may need very different levels of cover because their EMIs, household costs, family responsibilities, and savings can differ widely.

03

Pick the Right Policy Tenure

Your term plan should cover your peak-earning and liability years, ideally through at least age 60 to 65. Factor in home loans, children’s financial independence, and other long-term responsibilities. Longer tenure costs more, especially beyond age 70, since it crosses India’s average life expectancy.

04

Be Honest in Your Medical Disclosure

Disclose pre-existing conditions, family history of heart disease, diabetes, or cancer, smoking, alcohol use, and risky occupations. Non-disclosure is a common reason for claim disputes. A slightly higher premium is far better than a claim being rejected.

05

Avoid Return-of-Premium Plans

ROP plans refund premiums if you survive the policy term, but they often cost up to 2 times more than standard term plans. In most cases, investing the extra premium elsewhere can deliver better value, making standard term plans the smarter choice for most buyers.

Why Is Having an Intermediary Important While Buying Term Insurance?

Buying term insurance directly from an insurer is possible, but first-time buyers often miss important details:

Pick the first plan on a comparison site while ignoring the claim track record

Choose the wrong riders

Underestimate cover

Missed disclosures that can hurt the claim later

A good, non-commission-driven intermediary like Ditto helps you compare plans objectively, understand fine print, choose the right cover, and disclose everything correctly. Moreover, our support continues even at claim time, which is when the policy matters most.

How to Buy Term Insurance Online Through Ditto: Step-By-Step

Buying term insurance online through Ditto is straightforward. Go to Ditto's website to schedule a call, or WhatsApp us to speak with an IRDAI-certified advisor.

Note: When you buy term insurance through Ditto, you pay no extra charges, and the premium remains the same as what you would pay on the insurer’s website.

Ditto Claims Story: Why the Right Term Plan and Paperwork Matter

A policyholder passed away during a recreational snorkeling trip abroad. Since the death happened overseas and within the first 3 years of the policy, the insurer examined the ₹5 crore term insurance claim closely and asked for multiple documents.

The spouse had to arrange a death certificate and police report from the local authorities in the foreign country. Among these, the police report became the most critical document because it helped establish the circumstances of death clearly.

Ditto coordinated with the family and the insurer through every round of documentation and follow-up. Despite the complexity, the claim was approved and settled in full within 2 to 3 months.

Takeaway: When you buy term insurance, do not just compare premiums. Check the policy’s exclusions, disclose your lifestyle honestly, and keep your documents in order. If a claim happens abroad or during the first 3 years, clear paperwork can make all the difference for your family.

Documents Required to Buy Term Insurance Online in India

To buy a term insurance policy, you need to submit documents for KYC, age proof, income verification, medical assessment, and nominee registration. In many cases, one document can serve multiple purposes.

Basic KYC Documents: Aadhaar card, PAN card, passport, voter ID, driving license, recent utility bill, bank statement, or rent agreement.

Age Proof: Birth certificate, passport, Aadhaar card, PAN card, or 10th/12th marksheet.

Income Proof: Salary slips, ITRs, bank statements, Form 16, audited accounts, or CA-certified computation of income.

Medical Documents: Medical examination report, blood/urine test results, ECG/TMT reports, or previous hospitalization records, if required.

Nominee Details: Nominee’s full name, relationship with the policyholder, and percentage share.

Photograph and Signature: Recent passport-size photograph and policyholder’s signature.

After document submission, the insurer completes KYC, reviews your medical and income details, may conduct tele/video verification or medical tests, and then issues the policy after underwriting approval. This can take anywhere from a few days to 2–3 weeks, depending on the sum assured, medical history, occupation, and other disclosures.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Take on Buying Term Insurance

Buying term insurance is not complicated. But buying it incorrectly can have consequences. Too little coverage, an insurer with a weak claims track record, or a plan with conditions your family cannot navigate under stress can undermine the entire purpose of having the policy.

Here is how to move forward:

Start with the insurer. Look for a 3-year average CSR above 97%, an ASR above 90%, and a solvency ratio comfortably above 1.5x.

Size your cover correctly. Use Ditto’s cover calculator as a starting point, which adjusts for your loans, number of dependents, and long-term goals.

Choose a policy tenure that covers your financial responsibility years, typically until 60 to 65.

Be completely honest in your disclosure (medical history and existing life insurance policies).

Add riders only if they address a real gap in your protection.

The best time to buy term insurance was when you started earning. The second-best time is right now.

Disclaimer

At Ditto, we believe in full transparency. This guide includes our partner insurers (Axis Max Life, HDFC Life, ICICI Prudential, Bajaj Life) and a non-partner insurer (Aditya Birla) because our ranking methodology is unbiased and applied consistently across all insurance companies.

Frequently Asked Questions

What is term insurance, and how does it work?

Term insurance is the simplest form of life insurance. You pick a cover amount and a policy duration, pay a fixed annual premium, and if you pass away during that period, your nominee receives the full sum assured. There are no maturity payouts in a standard plan. For example, a 30-year-old buying a ₹2 crore plan for 35 years pays a fixed premium every year, and if they pass away in year 15, the family gets ₹2 crore to cover loans, living costs, and future goals.

How much term insurance cover do I actually need?

There is no one-size-fits-all answer here. At Ditto, we recommend calculating your coverage based on your outstanding uninsured loans, monthly household expenses, the number of dependents, and long-term financial goals, such as your child's education. A round number like ₹1 crore sounds large but may not be enough for a metro-based earner with a home loan and young kids. Two people with the same income can need very different covers depending on their liabilities and lifestyle. Use our cover calculator to estimate your actual number rather than guessing.

What is a good claim settlement ratio for term insurance in India?

The Claim Settlement Ratio (CSR) tells you what percentage of claims an insurer paid out in a year. At Ditto, we recommend picking an insurer with a 3-year average CSR of at least 97%. However, CSR alone is not enough. You should also check the Amount Settlement Ratio (ASR), which should ideally be above 90%, and the solvency ratio, which must be above the IRDAI-mandated 1.5x. For example, Axis Max Life has a 3-year average CSR of 99.71% across FY 2024-2026, among the highest in the industry.

Which is the best term insurance plan in India in 2026?

At Ditto, our top pick for 2026 is the Axis Max Life Smart Term Plan Plus, rated on insurer reliability, claims performance, features, and pricing. Axis Max Life carries a 99.71% average claim settlement ratio across FY 2024-26, the plan offers optional critical illness cover for up to 64 conditions, and includes a terminal illness payout of up to ₹1 crore. HDFC Life Click2Protect Supreme Plus and ICICI Prudential iProtect Smart Plus are strong alternatives depending on your budget and feature priorities. The best plan ultimately depends on your age, health, and financial profile.

How much does a ₹2 crore term insurance plan cost per year?

For a healthy, non-smoking 30-year-old male buying a ₹2 crore cover till age 65, premiums cost ₹20,656 per year for plans like Axis Max Life Smart Term Plan Plus. For a 30-year-old female under the same profile, premiums are lower, costing ₹17,558 per year. Premiums are affected by your age, gender, smoking status, health history, city of residence, and the plan you choose. Buying earlier locks in a lower premium for the policy's full tenure.

What documents do I need to buy term insurance online?

To buy term insurance online in India, you typically need identity proof such as Aadhaar or PAN, address proof such as a utility bill or bank statement, age proof, and income proof such as salary slips or ITR copies. You also need to provide nominee details, including name, relationship, and percentage share. Depending on your age and the cover amount, the insurer may request medical reports (costs borne by the insurer), such as blood tests, ECG, or TMT results, before issuing the policy.

Is it safe to buy term insurance online in India?

Yes, buying term insurance online in India is safe, provided you purchase from an IRDAI-registered insurer directly or via a licensed intermediary. The digital process today includes KYC verification, tele- or video-verification, and secure document submission. At Ditto, we help you navigate the process without spam or sales pressure, and our support continues at claim time, which is when the policy matters most. Just make sure you disclose all health conditions accurately during the application, as non-disclosure is one of the most common reasons for claim rejection.

What happens if I hide a health condition when buying term insurance?

This is one of the most consequential mistakes a buyer can make. If an insurer finds material non-disclosure after a claim is filed, they have the legal right to reject it entirely. Common things people hide include pre-existing conditions, family history of heart disease or cancer, smoking habits, or alcohol use. At Ditto, we consistently advise that a slightly higher premium, resulting from honest disclosure, is far better than your family facing a rejected claim. The whole point of buying term insurance is to protect your family, and non-disclosure completely defeats that.

Till what age should I take term insurance cover?

At Ditto, we recommend covering yourself at least till age 60 to 65, which typically covers your peak earning and high-liability years. If you have a home loan running till 55 or children who will be financially dependent till their mid-20s, your tenure should factor that in. Going beyond age 70 significantly increases premiums, since it exceeds India's average life expectancy. The key is to make sure your policy is active for every year your family depends on your income and until your major financial liabilities are cleared, with some buffer to account for delays/disruptions.

What riders should I add to my term insurance plan?

The three most common riders are critical illness cover and waiver of premium. A critical illness rider pays a lump sum if you are diagnosed with a covered condition like cancer or heart disease. A waiver of premium rider waives future premiums if you are disabled or critically ill. At Ditto, we suggest choosing riders based on your occupation, existing health insurance coverage, and lifestyle, rather than adding every available option. Stacking riders unnecessarily inflates your premium without proportionate benefit, so each rider should solve a real gap in your financial protection.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.