Overview

According to the Ministry of External Affairs, over 15.85 million NRIs living across the world, financial protection for families back in India has become more important than ever. Term insurance for NRIs offers global coverage, high sum assured options, and easy online purchase from anywhere, helping families stay financially secure despite geographical distance.

In the next few minutes, you’ll understand how NRI term insurance works, which plans stand out, what documents you need, and how to file a claim.

What Is Term Insurance for NRIs?

Term insurance for NRIs is one of the simplest and most affordable ways to financially protect your family. You pay a regular premium, and if you pass away during the policy term, your nominee receives a lump sum payout called the Sum Assured (SA).

The policy is issued in Indian Rupees (INR), and claim payouts are settled in Indian rupee-denominated bank accounts. In most cases, the nominee is a family member who receives the payout directly in INR. To ensure smooth claim settlement and faster fund transfer, the nominee should ideally have an active Indian bank account.

Best Term Insurance Plans for NRIs in India (2026): Ditto’s Pick

1) Bajaj Life eTouch II

Bajaj Life eTouch II is a practical option for NRIs who want affordable premiums with reliable core protection. Bajaj Life Insurance claim settlement ratio stood at 99.32% in FY 2024-25. The insurer has one of the strongest solvency ratios of 4.37x (average FY 2022-25) in the industry, which reflects solid financial strength.

Key Features

- Early payout on diagnosis of terminal illness, up to ₹2 crore, subject to policy terms.

- Premium break option for up to a year under eligible conditions while keeping the policy cover active.

- Health management services like teleconsultations and health checkups, at no extra cost.

- Future premiums will be waived in specified cases of accidental disability or terminal illness.

Riders Offered

- Family Protect Rider, which pays the parents of the life assured an additional amount in case of demise or accidental total permanent disability of the policyholder.

- The Accidental Partial/Total Permanent Disability Rider pays a lump sum amount if the life assured suffers permanent disability due to an accident. Full rider cover is paid for total permanent disability, while 50% of the rider cover is paid for partial permanent disability.

2) Axis Max Life Smart Term Plan Plus

Smart Term Plan Plus is a strong all-around option for NRIs who want flexible features along with long-term financial protection.

Key Features:

- Accelerated terminal illness payout of up to ₹1 crore, subject to policy terms.

- Instant claim support with advance payout of up to ₹2 lakhs at claim intimation from the death benefit, subject to conditions.

- The Smart Cover variant offers 1.5x life coverage for the first 15 years of the policy.

- Health management services like teleconsultations and related services via the Axis Max Life app.

Riders Offered

- Waiver of future premiums on specified disability or 11 listed illness events.

- Critical illness rider with lump sum payout for up to 64 listed illnesses for a fixed coverage period of 20 years.

3) HDFC Life Click 2 Protect Supreme Plus

Click 2 Protect Supreme Plus is a strong option for NRIs who value insurer stability, flexible protection, and long-term reliability.

Key Features

- Life stage benefit that allows eligible policyholders to increase cover after milestones like marriage, childbirth, or home loan without fresh medical underwriting.

- Premium break option that permits a temporary one-year premium pause with repayment later, subject to policy conditions.

Riders Offered

- Critical illness rider offering payout for up to 60 listed illnesses for a fixed 15-year benefit period.

- Waiver of premium rider where future premiums are waived on 60 specified critical illness or disability events while policy coverage continues.

Note: You can explore the Term Insurance Data Lab which serves as a central repository of term insurance information sourced from public insurers and IRDAI reports, helping readers access the data behind our findings and conclusions.

At Ditto, our primary recommendations for NRIs applying from overseas are usually Bajaj Life and Axis Max Life because of their relatively smooth NRI onboarding processes, support for overseas medical test arrangements, and cost-reimbursement options for eligible medical expenses. Every term insurance plan goes through a six-point evaluation framework. To explore more, refer to Ditto’s cut.

Note: For NRIs earning in stronger currencies like the United States Dollar (USD), the Great British Pound (GBP), or the United Arab Emirates Dirham (AED), Indian term insurance can become even more cost-effective over time when the rupee weakens. Since premiums remain fixed in Indian rupees, a gradually weakening rupee often means the same premium requires fewer dollars, pounds, or dirhams in future years.

How Much Does NRI Term Insurance Cost? (Sample Premiums)

According to Ditto’s research, NRIs sometimes face higher premiums based on their country of residence or occupation. Insurers account for country-specific mortality risks, higher underwriting costs, and claim servicing expenses. However, these factors are acceptable because term plans in a foreign country of residence are more expensive than those offered by Indian life insurers.

Premiums Across Profiles

Note: The annual premiums below are for non-smoking NRIs living in the US earning $80,000 (₹76.16 lakhs) per annum with their nominees in Delhi (110010). The illustrative figures are for a ₹2 crores cover, with coverage up to age 70 and without 1st year discounts.

NRIs may need a higher sum assured than resident Indians if their income, family dependency, loans, or global lifestyle justify it. The correct cover is one of the key factors to consider when purchasing a term plan. For a clearer understanding, use our online term cover calculator to get an estimate of it.

Let’s see how premiums increase as the sum assured increases. The indicative premiums (coverage up to age 70, without 1st-year discounts) are for Bajaj Life eTouch II for non-smoking NRIs in the US, with their nominees in Delhi (110010).

Premiums Across Profiles

Note: For a 35-year-old male, when moving from a ₹2 crores SA to a ₹5 crores SA, the premiums increase 2.36x times while the term cover increases by 2.5x times. This shows that higher cover slabs can sometimes offer better protection efficiency per rupee of premium, especially for younger buyers with long-term financial responsibilities.

Key Features of NRI Term Insurance Plans

- Global Coverage: Most NRI term insurance plans provide worldwide coverage. If the policyholder passes away in India or abroad, the nominee receives the payout.

- High Coverage Flexibility: NRI term plans typically start at around ₹50 lakhs and can go up to ₹10 crores.

- Lower Premiums Than Overseas Policies: Term insurance in India is often much cheaper than similar plans in countries such as the US, the UK, the UAE, and Singapore. Indian plans also lock premiums for the full policy term, unlike many foreign policies, where premiums can be repriced and increase sharply after 20 to 30 years.

- Easier Claim Settlement for Families: Claims are generally settled in India, which makes the process simpler for families living here. Nominees can directly contact the insurer’s Indian branch or online support team.

- Useful Features: Many insurers now offer in-built features like terminal illness benefits, premium break options, and instant claim support.

- Riders Offered With NRI Term Insurance: NRI term plans may offer riders like critical illness cover, waiver of premium, and total or permanent disability protection. The availability of these riders depends on the country of residence, occupation, age, and insurer underwriting rules.

Take a look at the infographic to get an understanding of which add-ons to purchase and which to avoid.

Countries Where NRI Term Insurance Is Restricted

There is no single IRDAI-approved list of restricted countries for NRI term insurance. Every insurer follows its own internal risk classification based on factors such as mortality rates, political stability, medical infrastructure, claim verification standards, and occupation-related risks in that country.

For example, many private life insurers like Bajaj Life and Axis Max may not offer NRI term insurance coverage to applicants residing in countries like Pakistan or Bangladesh due to internal underwriting, geopolitical, or claim verification risks.

Documents Required for NRI Term Insurance

- Identity and residency proof, such as a copy of a valid passport, visa, work permit, or residence permit. You may also need to submit overseas address proof, such as a utility bill or rental agreement. Some insurers ask for a Foreign Tax Identification Number (FTIN) or an equivalent declaration.

- Proof of income, such as recent salary slips, employment contracts, overseas bank statements, or tax returns filed in your country of residence.

- Most insurers require NRE, NRO, or Foreign Currency Non-Resident (FCNR) account details for premium payments and future claim settlement.

- Depending on your age, coverage amount, country of residence, and health profile, insurers may request medical test reports and a self-declared health questionnaire. Most insurers start with a tele/video medical evaluation and then decide if physical tests are needed.

- NRIs are generally required to complete the Foreign Account Tax Compliance Act (FATCA) or Common Reporting Standard (CRS) declarations along with the proposal form. It is important to accurately disclose details related to occupation, travel, smoking habits, income, existing policies, and medical history.

Did You Know?

Talk to an expert

today and

find

the right

insurance for you.

How to Buy Term Insurance as an NRI: Step-by-Step

1) When Abroad

Step 1: Confirm Country Eligibility

Before comparing premiums, first check whether the insurer accepts applicants from your current country of residence.

Step 2: Choose the Right Cover Amount

Select coverage based on your family’s financial responsibilities, loans, future goals, and income replacement needs.

Step 3: Shortlist Insurers with a Strong NRI Process

Choose insurers that can support overseas medicals, video medical examinations, and foreign claim settlement processes. Also, look out for the insurer’s metrics while comparing the best term insurance companies in India.

Step 4: Keep Documents Ready

NRI applications usually require additional paperwork such as a passport, a visa, overseas address proof, income documents, Indian bank account details, and tax declarations.

Step 5: Fill the Proposal Form Honestly

Clearly mention your overseas address, country of residence, occupation, income, travel history, smoking status, medical history, and existing insurance policies.

Step 6: Complete Medical Tests

Depending on age, country, coverage amount, and health profile, insurers may arrange video medicals, overseas medical tests, or tests during your India visit.

Step 7: Pay Through Approved Banking Channels

Premiums are generally paid through NRE, NRO, or FCNR accounts. Maintain a clean payment trail and avoid unrelated third-party payments to prevent compliance issues.

2) When in India

- Do Pre-Screening Before Travelling: Before visiting India, shortlist insurers and confirm whether they accept your country of residence and occupation.

- Carry All Required Documents: Keep both physical and digital copies of important documents such as passport, visa, overseas address proof, salary slips, tax returns, bank statements, existing insurance details, medical records, and nominee information.

- Apply as an NRI, not as a Resident Indian: Even if you apply while physically present in India, you must disclose your actual overseas residence, occupation, and country of stay.

- Complete Medical Tests in India: One major advantage of buying during an India visit is easier medical coordination at no extra cost.

- Resolve Underwriting Queries Before Departure: Insurers may ask additional questions regarding income, overseas employer details, travel history, medical reports, or existing insurance policies.

- Pay Premium Through the Correct Banking Route: Use approved payment channels such as NRE, NRO, FCNR accounts, or permitted foreign remittance routes.

Premium Payment Options for NRIs

NRIs can usually pay premiums for their term insurance plan through NRE, NRO, or FCNR accounts. Many insurers also accept international debit or credit cards and, in some cases, direct foreign bank transfers through approved payment channels.

Several insurers now also allow payments through regular Indian savings accounts using UPI, net banking, or standard online banking methods, subject to insurer and banking compliance rules.

Tax Benefits of NRI Term Insurance in India

NRIs also receive tax benefits on term insurance under Indian tax laws, subject to eligibility conditions.

- Section 80C: Under Section 80C of the old regime, premiums paid for NRI term insurance qualify for a tax deduction of up to ₹1.5 lakh.

- Section 10(10D): The death benefit paid to your nominee is tax-free under Section 10(10D) in India, subject to applicable laws.

Note: Tax treatment may differ in your country of residence, so it is advisable to also check local tax laws, remittance rules, and reporting requirements.

How to File a Claim on NRI Term Insurance?

Claim Intimation

The nominee should inform the insurer about the claim as early as possible through the insurer’s website, email, branch office, or customer support channel.

Document Submission

The nominee usually needs to submit documents such as the claim form, policy document, death certificate, nominee identity proof, bank details, and relevant medical or hospital records. If the death occurs abroad, overseas documents may need confirmation or translation.

Claim Evaluation

The insurer reviews the policy terms, disclosures made during purchase, and submitted documents. Overseas claims may involve additional verification depending on the country and cause of death.

Claim Payout

Once approved, the insurer transfers the death benefit to the nominee’s Indian bank account, subject to applicable RBI and FEMA guidelines.

Who Should Buy NRI Term Insurance?

NRIs with financial dependents in India or those planning to eventually return and settle in India. Young and healthy overseas NRI earners with stable long-term income and professionals with INR-linked goals, such as parents’ retirement or children’s education. NRI term plans also suit individuals managing home loans or other liabilities in India.

Note: An Indian term insurance policy can continue even after the policyholder obtains permanent residency or foreign citizenship, provided the insurer’s disclosure and servicing requirements are properly followed.

Who Should Avoid NRI Term Insurance?

People with no financial dependents or long-term obligations in India may not need large India-based cover. NRIs primarily managing foreign-currency liabilities, such as a US mortgage, may require protection aligned to overseas obligations instead. Applicants who cannot provide stable income proof or salary documents can face underwriting challenges. Individuals nearing retirement with minimal liabilities and sufficient accumulated assets may also find limited value in long-duration term insurance.

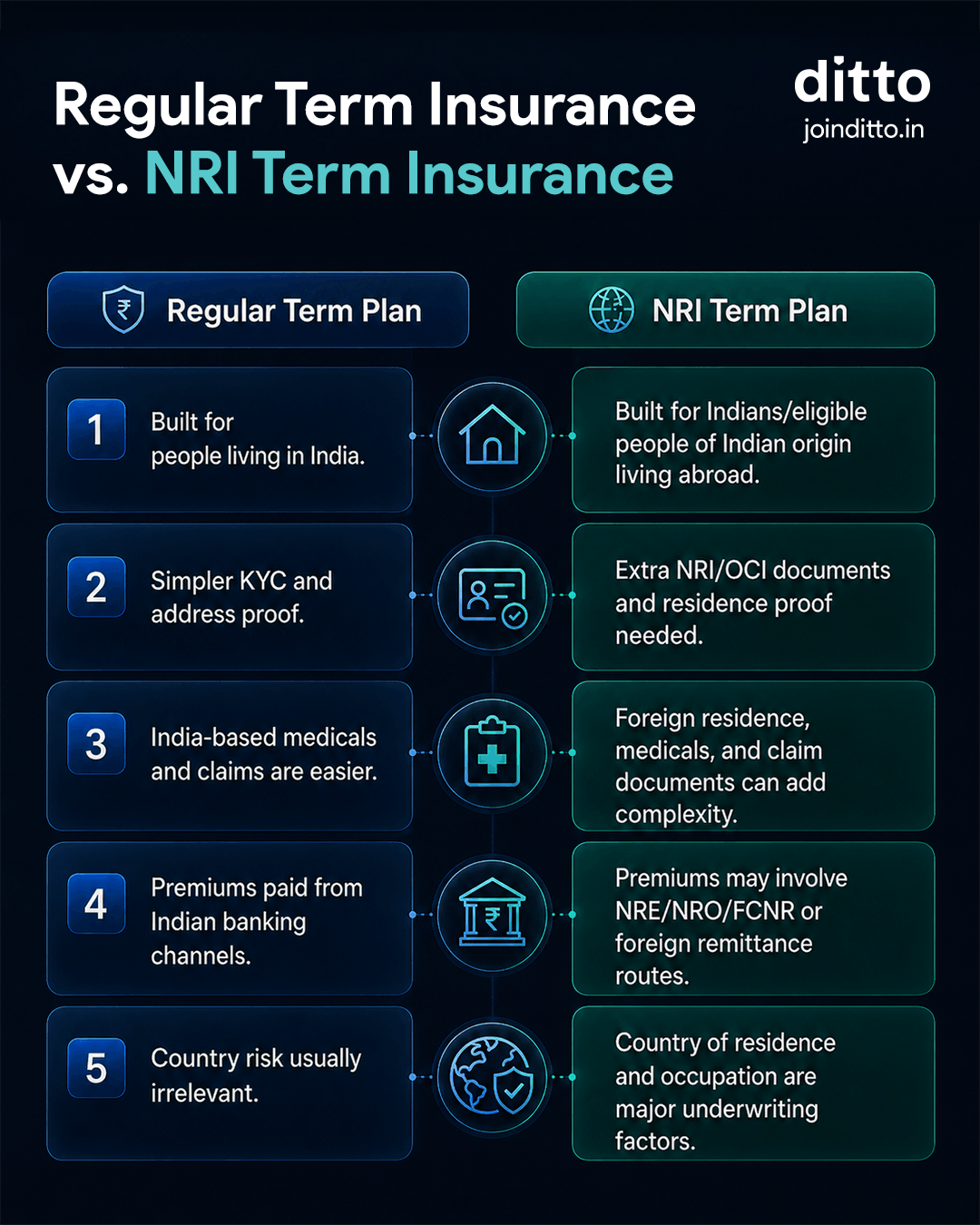

NRI Term Insurance vs. Regular Term Insurance: Key Differences

The core structure of NRI term insurance and regular term insurance remains largely similar. The biggest differences usually come from disclosures, underwriting, documentation, premium payment routes, and servicing processes.

Temporary overseas travel for work or vacations is generally covered under regular term policies. However, if you move abroad for an extended period, insurers should be informed so that records, underwriting, and future claim servicing remain smooth and compliant.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 25,000+ happy customers

- Backed by Zerodha

- Dedicated Claims Support Team

- 100% Free Consultation

If you'd like to learn more about how Ditto helps you find the best term insurance for NRIs, you can check our detailed guide.

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Ditto’s Take on Term Insurance for NRIs

At Ditto, we strongly believe NRIs should consider term insurance because it offers affordable long-term financial protection backed by India’s well-regulated insurance framework. Buying early also helps lock in lower premiums, since term insurance costs are usually much cheaper at younger ages.

In our experience at Ditto, we have come across several NRI term cases, and here’s what we see and suggest:

- NRIs who apply while visiting India gain access to a wider range of insurers, since medicals and underwriting coordination are much easier during a stay of around 2 to 4 weeks.

- Over the years, many NRIs we have assisted have preferred limited premium payment options rather than paying throughout the policy tenure. Higher overseas disposable income often allows them to finish premium commitments earlier.

- For most individuals, choosing a policy term extending to ages 60 to 70 generally works well, since this is usually the stage when major liabilities decrease, children become financially independent, and retirement planning becomes more stable. However, some NRIs choose longer tenures considering delayed retirements and longer life expectancy abroad.

Frequently Asked Questions

Customer Reviews

Last updated on: