Quick Overview

Choosing the right life insurer can be confusing, given the number of options and varying claim performance. HDFC Life aims to simplify this with strong backing from HDFC Bank and a wide distribution network of 500+ partners across India. In this HDFC Life review, we’ll assess its key metrics, pricing, product range, and overall value.

HDFC Life Performance Metrics

Key Insights on HDFC Life’s Performance Metrics

- HDFC Life’s CSR has consistently stayed around the 99–100% range, well above the industry mean, meaning that customers can rest assured knowing that their genuine claims will be settled.

- The insurer reported a high average ASR, indicating that it treats high- and low-value claims equitably.

- HDFC Life’s annual business volumes are significantly higher than the industry median, suggesting its large scale of operations.

- HDFC Life has dramatically low complaint volumes, indicating comparatively fewer customer grievances.

- The company’s solvency ratio is slightly below the industry median, but still comfortably above the IRDAI’s minimum requirement of 1.5×, which suggests sufficient capital buffers.

Note: Explore Ditto Data Lab if you want to review insurer and IRDAI statistics in detail. The term insurance data has been sourced from official publications and curated by our team.

Top Plans Offered by HDFC Life

Note: The list above covers the popular plans and does not provide a complete view of all plans offered by HDFC Life.

Now that we’ve covered the lineup, let’s zoom in on HDFC Life’s flagship term plan, especially since term insurance is the route we recommend at Ditto to protect your financial dependents. This is because it offers high coverage at low costs and represents the simplest form of life insurance.

Spotlight: HDFC Life Click 2 Protect Supreme Plus Term Plan (C2PSP)

Key Features:

HDFC Life Click 2 Protect Supreme Plus is a feature-rich term insurance plan that offers:

- Flexible cover options (including level or increasing life cover)

- Life-stage benefits

- Premium break options

- Instant claim payout

- Wellness services

- Smart exit option

- Multiple variants (Life, Life Plus, and Life Goal)

- A return of premium option

- Spouse coverage option

If you want a deeper breakdown of the plan’s features, eligibility, riders, and pricing, you can read our detailed guide on HDFC Life Click 2 Protect Supreme Plus.

Premium Comparison for HDFC Life’s Flagship Term Plan

Profile Considered: Premiums are based on a ₹2 crore sum assured, with coverage up to age 70 for a non-smoking male, with no added riders or 1st-year discounts. Also, the above-mentioned premiums are illustrative and may vary based on age, medical history, and insurer underwriting criteria.

Insights: HDFC Life Click2Protect Supreme Plus is typically priced higher than peers like Bajaj Life eTouch II and ICICI Pru iProtect Smart Plus, with Axis Max Smart Term Plan Plus in the mid-range. However, the higher cost reflects better customization, stronger claim metrics, a wider rider range, and greater operational ease, making C2PSP one of our top recommendations.

Riders Available in HDFC Life Plans

- Critical Illness Rider (Health Plus)

Provides a lump sum payout if the policyholder is diagnosed with any of the 60 listed critical illnesses, subject to a 90-day waiting period and a 15-day survival period. A critical illness rider is highly recommended by Ditto.

- Waiver of Premium (WOP) Rider

Waives all future premiums if the policyholder is diagnosed with a covered critical illness or a specified disability, provided the policy remains active. For women, it also waives all future premiums if the husband dies due to an accident, while the policy continues. The WOP rider is also strongly recommended by Ditto.

- Accidental Income Benefit Rider

Pays 1% of the rider's sum assured every month for 10 years if the policyholder suffers total and permanent disability due to an accident.

- LiveWell Rider

Offers a bundle of benefits, including accidental death cover, personal accident protection, hospitalization cash, and surgical care, depending on the option chosen.

- Education Income Benefit Rider

Provides annual payouts to a child beneficiary after the policyholder’s death, continuing until the policy term ends or the child turns 25, whichever occurs earlier.

- Parent Protect Care Rider

Allows the death benefit to be split between a lump sum payout and regular income, with the income portion payable only to parents or grandparents.

Note: These riders are specific to the Click 2 Protect Supreme Plus plan, and some may not be available across other HDFC Life products. Since rider terms, limits, and eligibility conditions can be complex, it’s best to review the Click 2 Protect Supreme Plus official brochure for full details before opting for them.

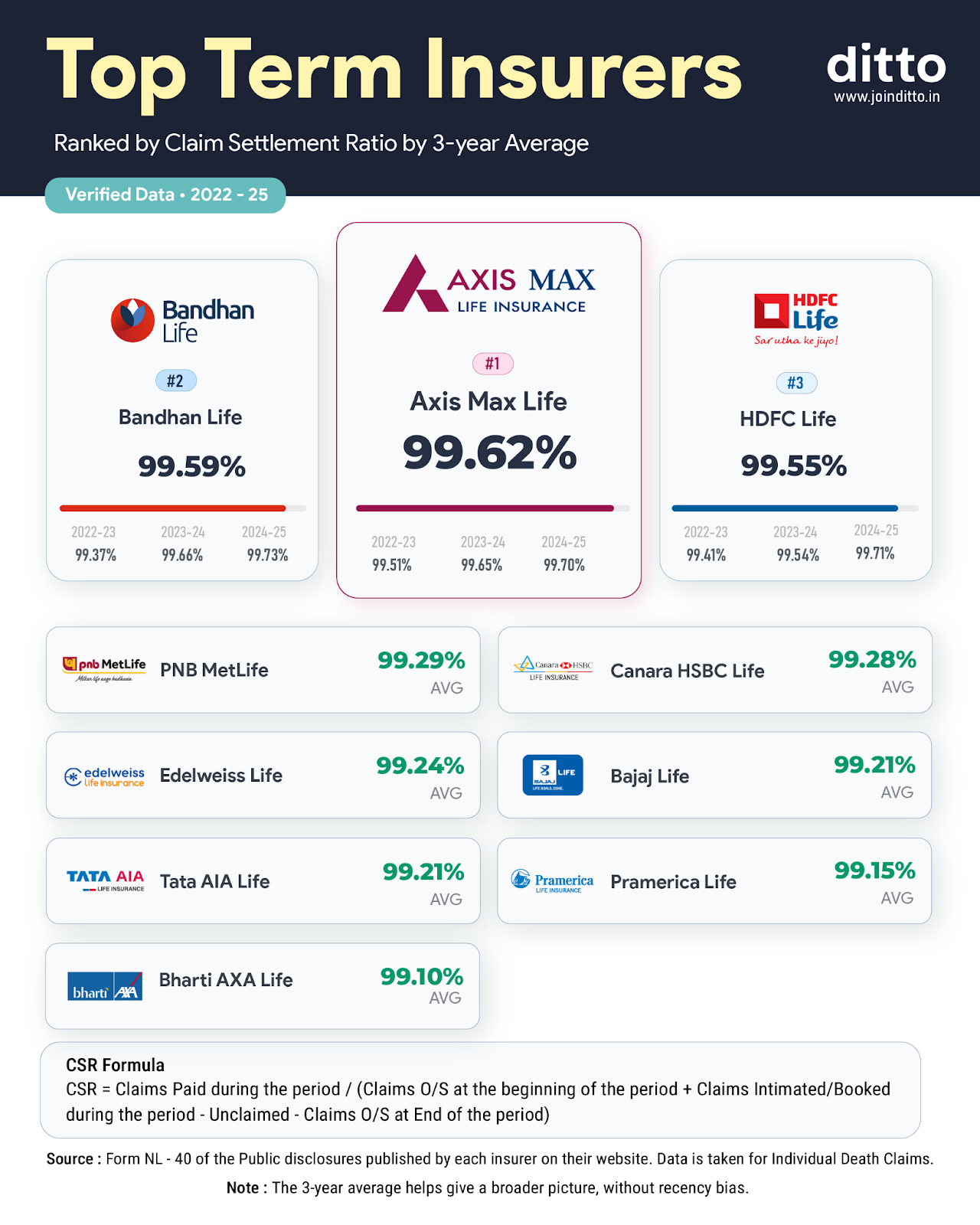

Top 10 Life Insurance Companies in India by Claim Settlement Ratio

Disclaimer: CSR reflects the overall claim settlement performance of the insurer across all life insurance products, including term plans, and is not specific to any single policy or policy category. For complete exclusions, benefits, and conditions, always refer to the official policy documents before making a decision.

Insights: HDFC Life ranks third among the top 10 term insurers by CSR, which is commendable given its large business volumes.

From Ditto’s Claims Desk: Rider Claim With HDFC Life

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right term insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or WhatsApp us now, slots fill up fast!

Conclusion

HDFC Life is one of India’s largest and most established insurers, with Click 2 Protect Supreme Plus offering strong customization and multiple riders. Underwriting is relatively stringent, often requiring detailed medical and financial checks, which can lead to slightly longer approval timelines but help ensure smoother claims later. On the servicing side, HDFC Life performs well and does not have strict negative pincode restrictions. Overall, it suits buyers who prioritize reliability and ease of operation, while more price-sensitive buyers can consider alternatives such as the Axis Max Smart Term Plan Plus or the ICICI Pru iProtect Smart Plus.

Disclaimer

Frequently Asked Questions

HDFC Life Customer Reviews

Last updated on: