Overview

ULIPs promise life cover with market-linked returns in one plan. But behind this pitch lies a 5-year lock-in and limited access to your money. Do they really build wealth efficiently or restrict your flexibility? This article breaks down ULIP lock-in rules, exit options, long-term benefits, and how ULIPs compare with term insurance, so you can make a clear and informed decision.

Rules Around ULIP Lock-In Period

- 5-Year Lock-In: ULIPs have a strict 5-year lock-in period that begins on the policy start date. During this period, you cannot withdraw or access your fund value, except in case of death or specific policy conditions. IRDAI sets the lock-in to encourage long-term financial discipline and wealth accumulation.

- Minimum Term and Premium Commitment: ULIPs must have a minimum policy term of 5 years. For regular pay premium plans, you must continue paying premiums for at least 5 years, which creates a fixed financial commitment in the early years. For non-single-premium plans, the premium payment term must also be at least 5 years.

- Withdrawals After Lock-In: Once the 5-year lock-in ends, you can make partial withdrawals from your fund value. This adds flexibility, but frequent withdrawals may reduce your long-term investment potential and overall returns.

- Loan Facility: Loans are not allowed directly from insurers during the ULIP lock-in period. You cannot borrow against the policy within the first 5 years. After lock-in, loans may be taken via banks or Non-Banking Financial Companies (NBFCs) against surrender value, with limits based on fund type and value.

- Top-Ups Have Separate Lock-In: Each top-up investment stays locked for 5 years from its own start date. This means newer investments may still be restricted even after the base policy completes its lock-in period.

Note: ULIPs require patience and long-term commitment. However, ULIP charges can reduce overall returns, and liquidity is limited in the first 5 years. Furthermore, restrictions on withdrawals can make them less suitable if you need flexibility or short-term access to funds.

Can You Exit a ULIP Before the Lock-In Period Ends?

Yes, you can surrender or stop your ULIP before 5 years, but you will not receive the money immediately. The insurer moves your fund value, after charges, to a discontinued policy fund. Your life cover stops, and the payout is released only after the 5-year lock-in ends.

Here’s a summary of what the ULIP lock-in period means:

Note: If you miss premiums in the first five years and do not pay within the grace period, the ULIP usually moves to discontinuance. The fund value shifts to a discontinued policy fund after applicable charges are deducted.

Benefits of Staying Invested Beyond the ULIP Lock-In Period

- Better Liquidity: After 5 years, you can withdraw a portion of your fund value whenever needed. This gives you more control over your money compared to the strict restrictions in the initial years.

- Lower Charges Over Time: ULIP charges are higher in the early years and reduce later. Staying invested helps you benefit from lower ongoing costs, which can improve your overall returns over time.

- Stronger Compounding Effect: When you stay invested for 10 to 15 years, your money gets more time to grow. This helps offset early charges and improves the long-term wealth creation potential.

- Flexible Fund Switching: You can switch between equity, debt, or balanced funds based on market conditions and your goals. This allows better risk management without exiting the policy.

- Tax-Efficient Access: Withdrawals after 5 years are usually tax-free under Section 10(10D), subject to conditions like the premium-to-sum assured ratio being tightly regulated. It is capped at 20% for older policies and 10% for newer ones, ensuring a minimum level of meaningful life cover. This makes ULIPs more tax-efficient if you stay invested for the long term.

Note: Most other investment options also have lock-ins, but they usually offer better liquidity or clearer exit rules. This table helps you compare how easily you can access your money across these products.

Why the ULIP Lock-In Can Work Against You?

Your Money Is Not Easily Accessible

Once you invest, you lose flexibility. If your needs change or you face an emergency, you cannot access your money freely in the early years. This makes ULIPs unsuitable without strong backup savings.

Does Not Match Real-Life Needs

Life can change at any time. Job loss, medical expenses, or business issues can arise. A product that restricts access to your own money during such times adds pressure.

You Pay High Costs Upfront

Most charges apply in the initial years. If you exit early, you bear these costs but do not get enough time for your investment to recover or grow.

Hard to Exit a Wrong Decision

Many people realize later that the product does not suit them. The lock-in keeps you stuck, with limited options to correct the decision.

The lock-in does more than enforce discipline. It reduces flexibility, locks in early costs, and limits your choices. If you value control and clarity, ULIPs may not be the right fit.

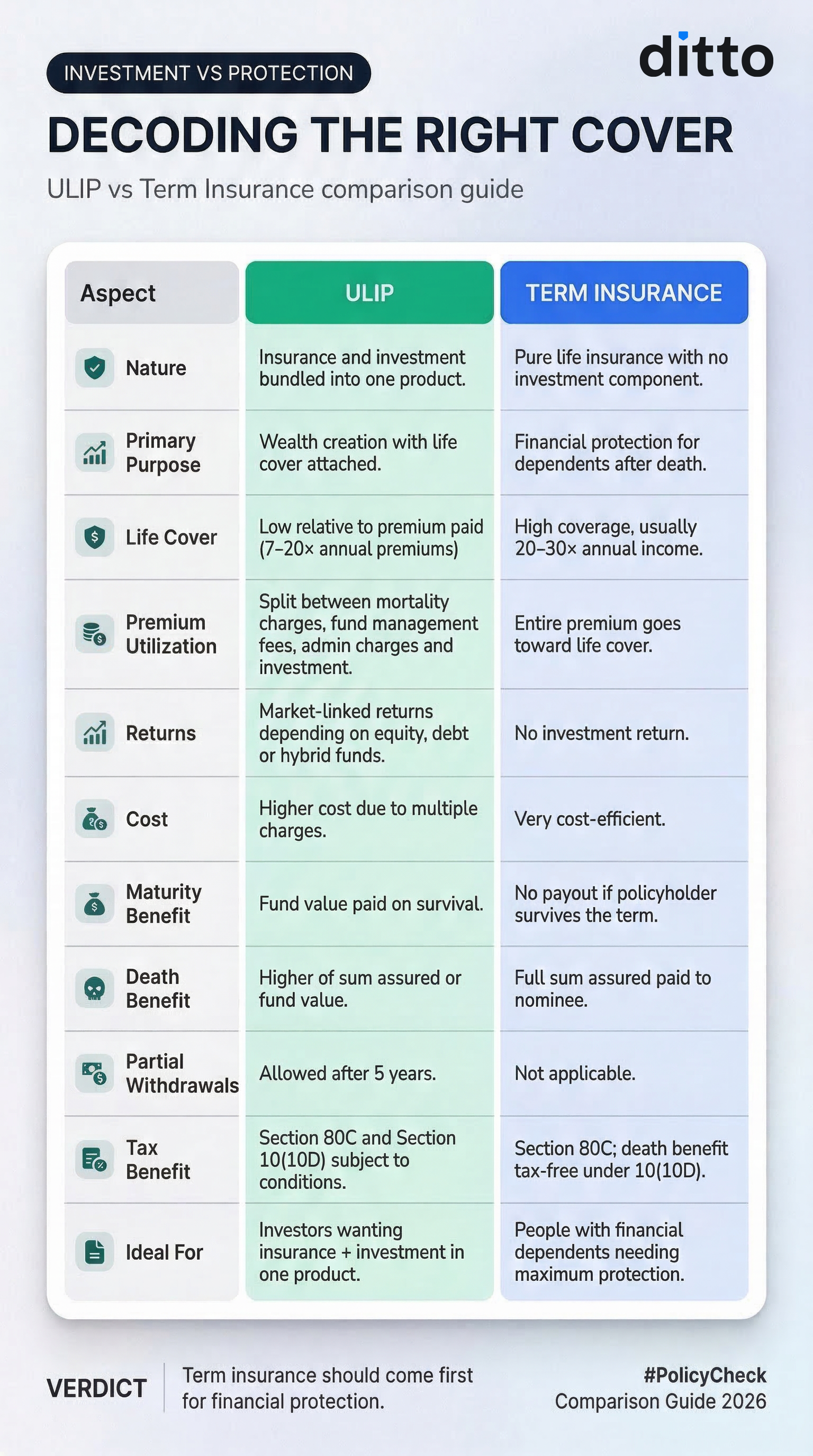

ULIP vs. Term Insurance: Which Is Better?

From a protection standpoint, term insurance is far more effective. An HDFC Life ULIP for a 25-year-old may cost around ₹1 to ₹2 lakh a year and offer about ₹20 lakh cover. In comparison, a pure term plan like HDFC Life Click 2 Protect Supreme Plus can provide ₹2 crore or more cover for roughly ₹19,000 to ₹22,000 annually.

From an investment perspective, ULIPs come with multiple charges that reduce long-term returns. Low-cost options like index funds or NPS usually perform better over time. Keeping insurance and investments separate gives you higher cover, better returns, and more flexibility.

For more information, you can check out our comprehensive guide on term insurance vs ULIPs or take a look at the infographic below:

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

The 5-year ULIP lock-in is not just a rule. It shapes the entire product. You lose liquidity, access to your money stays restricted, and you commit to the long term even if your needs change.

If you are certain about staying invested for 10 to 15 years and understand the costs, a ULIP can work. But if you want flexibility, clear costs, and stronger protection, a term plan with separate investments is usually the better choice. Invest in suitable options such as mutual funds, NPS, PPF, and Fixed Deposits (FDs) based on your risk profile, investment horizon, liquidity needs, and tax planning requirements.

If you are looking for a term plan from established insurers, we recommend the best term insurance plans, which align with your future goals.

Frequently Asked Questions

Last updated on: