Overview

Health insurers settled claims worth ₹94,248 crore during FY 2024-25 alone as per IRDAI annual reports. As medical costs surge, choosing a health plan with strong cashless support, fast approvals, and a reliable hospital network has become more important than ever.

In the next few minutes, this guide will walk you through the plans that offer cashless health coverage, their premiums, and mistakes to avoid while purchasing a cashless health policy.

What Makes a Good Cashless Health Insurance Policy?

- Strong Hospital Network: A good cashless health insurance policy should work well where you actually live and seek treatment. Instead of only checking the total number of network hospitals, verify whether your specialty centers are included in the insurer’s network. At Ditto, we recommend insurers with 10000+ network hospitals.

- Fast Cashless Approvals: Quick approvals matter during emergencies. A reliable insurer should support smooth pre-authorization and discharge processes. As per IRDAI rules, insurers have to decide cashless authorization within 1 hour and provide discharge authorization within 3 hours of the hospital’s request.

- Lower Out-of-Pocket Costs: A strong cashless policy should reduce surprise hospital expenses. Look for plans without any kind of co-payments or sub-limits.

- Adequate Sum Insured: Cashless hospitalization only helps if the sum insured is large enough. In today’s healthcare environment, metro families often need ₹15 lakh to ₹20 lakh or higher, especially if they prefer private hospitals.

- Strong Restoration Benefits: Good restoration features should ideally work for the same illness, on partial exhaustion, and even for the same insured person, instead of only after full exhaustion of the base cover.

- Strong Cumulative Bonus Growth: A good cumulative bonus feature increases your sum insured after claim-free years without proportionately increasing the premium. This creates a larger financial cushion over time and helps handle rising hospitalization and treatment costs more comfortably during cashless claims.

- Reasonable Waiting Periods and Claim Support: Always review waiting periods for pre-existing diseases and major treatments carefully. Along with this, responsive customer support and smooth hospital coordination can make a major difference during stressful situations.

Top 5 Cashless Health Insurance Plans in India [2026]

To explore more about the above plans, explore our guide on the best health insurance plans.

Sample Premiums Across Plans and Profiles

Note: In the table, A stands for Adult and C for Child. These annual premiums with recommended add-ons are based on a ₹15 lakh cover for people living in Delhi (110010). Actual premiums may change based on your health profile, selected add-ons, underwriting, and city of residence.

Key Features to Compare Across These Plans

The plans listed above are comprehensive and do not include any kind of copayment, room rent restrictions, or disease-wise sublimits. However, you may compare them on other parameters.

- Coverage for Consumables and Modern Treatments: Compare whether consumables and modern treatments are covered. Plans like Optima Secure+ and Activ One Max have in-built consumable coverage.

- Waiting Periods and PED Rules: Review pre-existing disease waiting periods and disease-specific exclusions carefully. Plans like SBI Super Health Platinum Infinite offer low waiting periods, such as 2 years for pre-existing diseases.

- Network Hospitals Near You: Check whether your preferred hospitals and specialty hospitals are part of the active cashless network.

- Cashless Everywhere Support: Check whether the insurer supports the General Insurance Council’s Cashless Everywhere framework. A strong insurer should also have a smooth pre-authorization and discharge process.

- Insurer Metrics: Review the insurer’s claim settlement ratio, complaint volume, and average claim servicing experience. Strong insurer metrics often indicate better operational efficiency.

To explore more about features you should consider with your health plan, refer to the health insurance checklist.

Take Note: Do not judge a health plan only by low premiums, large hospital counts, or high sum insured figures without carefully checking hidden limits and exclusions.

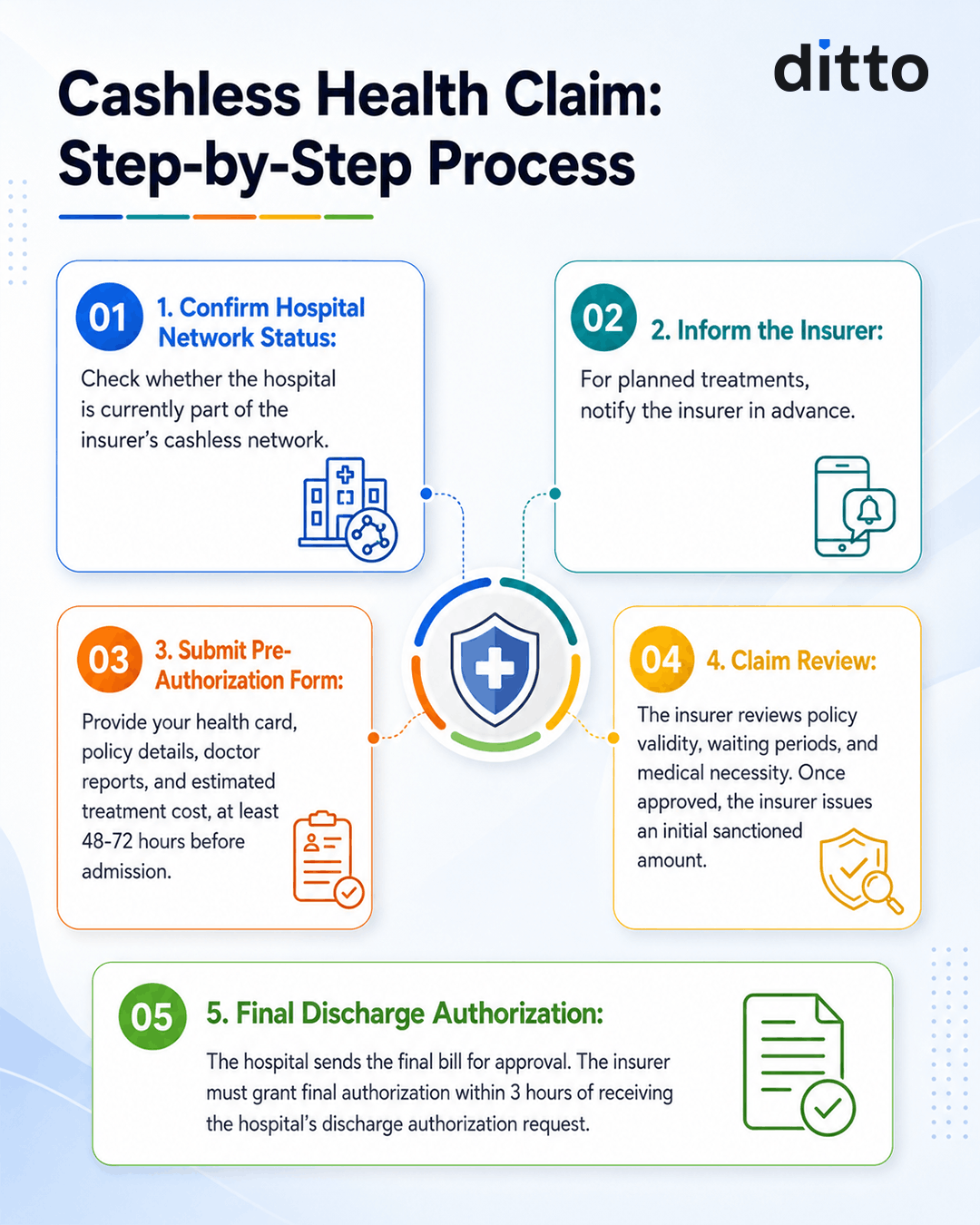

How to File a Cashless Claim: Step-by-Step

Filing a cashless health claim is simple. Take a look at the infographic to understand how the process works.

Once the insurer approves the cashless claim and treatment is completed, the hospital prepares the final bill and sends it to the insurer for settlement. Keep in mind that cashless approval does not always mean every expense is covered. You may still need to pay for non-medical consumables, co-payments, deductibles, expenses beyond policy limits, or treatments excluded under the policy terms.

Before discharge, collect all important documents, including the final bill, deduction sheet, discharge summary, investigation reports, prescriptions, and payment receipts. These records can help resolve disputes or support future claims, if required.

In case of emergencies, get admitted first and share policy details once stable. The hospital usually raises the cashless request within 24 hours. Keep documents ready, respond quickly to insurer queries, and ask the hospital to raise enhancement requests if costs increase during treatment.

Note: A rejected cashless request does not always mean the final claim is rejected. You can still file a reimbursement claim. Common reasons for health claim rejections include incomplete documentation, suspected PED non-disclosure, or medically unjustified hospitalization.

Common Mistakes to Avoid When Choosing Cashless Insurance

- Do not judge a plan only by the total network hospital count. Check whether your preferred hospitals are actually covered.

- Ignoring room-rent limits can lead to large proportionate deductions during claims.

- Cashless approval does not mean every hospital expense becomes free. Non-payable items may still apply.

- Always check co-payment clauses, especially in senior citizen and low-premium plans.

- Review disease-wise caps and waiting periods carefully before buying the policy.

- Choosing a very low sum insured can leave you exposed during major treatments in private hospitals.

- Keep policy details, nominee information, contact details, claim helpline numbers, and policy documents easily accessible for your family during emergencies.

Which Cashless Health Insurance Plan Is Best for You?

There is no single best health plan that fits every need. The right cashless health insurance plan depends on your city, healthcare preferences, family needs, age, and budget.

- Young Individual: Comprehensive base plan with ₹10 lakh to ₹15 lakh cover.

- Couple Planning Family: Plan with maternity, newborn cover, and no harsh sub-limits.

- Family With Kids: Family floater with strong restoration and bonus features.

- Parents Above 60: Senior-friendly plan with manageable co-pay (if any) and strong hospital network

A well-balanced policy should combine strong coverage, smooth claims support, and practical long-term value.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 22,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Conclusion

The best cashless health insurance in India is the one that works smoothly when you actually need hospitalization, not just on paper. Focus on coverage quality, claims experience, and hospital access.

If you buy your policy through Ditto, contact us for end-to-end support for claim assistance during stressful medical situations.

Frequently Asked Questions

Last updated on: