Quick Overview

Getting hospitalized is stressful enough. Figuring out how to pay for it shouldn’t add to that stress. This is where your health insurance quietly does its most important job. But here’s the catch: whether your experience is smooth or chaotic often depends on one thing: whether the hospital you choose is part of your insurer’s network.

In this blog, we’ll break down what a network hospital is and how cashless treatment actually works in practice. We’ll also show you how to find insurer-specific lists like Niva Bupa network hospital and Star Health network hospital, what to do if your claim is rejected, and how the reimbursement route works.

What Is a Network Hospital in Health Insurance?

A network hospital is a medical facility that has a tie-up with your health insurance company or its TPA (Third Party Administrator), allowing you to access cashless treatment.

Under this arrangement:

- The hospital sends your bill directly to the insurer

- The insurer pays the approved amount

- You pay only for expenses outside your policy’s coverage (like co-payments, consumables, or costs beyond limits)

However, network hospitals aren’t a single, uniform category. Most insurers maintain a standard network, but within that, there can be multiple layers:

- Preferred Provider Networks (PPN): Hospitals with pre-negotiated package rates, leading to smoother approvals and more predictable billing

- Preferred Hospital Networks: Often available for corporate/group policies with faster processing and dedicated support

- Tiered Networks: Some plans restrict access to certain hospitals or apply co-payments if you choose outside a preferred tier

- Separate OPD and Diagnostic Networks: Insurers may have different (often larger) networks for outpatient consultations and diagnostic centers

- Excluded/Blacklisted Hospitals: Facilities where cashless claims are not allowed despite being listed, usually due to billing disputes or compliance issues

A network hospital is part of a commercial agreement between the insurer and hospital, not a quality certification. Clinical outcomes or infrastructure aren’t always considered, and National Accreditation Board for Hospitals & Healthcare Providers (NABH ) accreditation isn’t mandatory. This means the “10,000+ hospitals” list can include everything from top hospitals to small nursing homes.

What really matters is whether good hospitals near you fall within the right tier, are active for cashless, and are covered under your specific plan. So, always check the type, reputation, and accessibility of hospitals near you.

How to Use Cashless at a Network Hospital

Step 1: Show Your Health Card

Step 2: Pre-Authorization Request

Step 3: Approval from Insurer

Step 4: Treatment and Discharge

Note

What If There Is No Network Hospital Nearby?

If you don’t have access to a network hospital, you can opt for reimbursement.

How It Works:

- Get treated at any hospital

- Pay the bill upfront

- Submit documents like:

- Bills and receipts

- Discharge summary

- Prescriptions

- The insurer reviews and reimburses the eligible amount

Downsides of Reimbursement:

- You need to arrange cash up front

- There is more paperwork involved

- The process takes longer than cashless claims

Note

What Are Blacklisted or Excluded Hospitals?

Insurers maintain a list of hospitals where cashless claims are not allowed, usually due to issues like overbilling, fraud concerns, or non-compliance.

- These hospitals may still appear in search results

- But cashless treatment won’t be permitted there

- You may still use reimbursement, depending on insurer rules

Benefits of Cashless Treatment at Network Hospitals

You don’t have to make a large upfront payment during a medical emergency, and the claim process is usually faster since the hospital and insurer coordinate directly, with minimal paperwork on your end.

You also get better clarity on what’s covered before discharge. However, in some cases, treatment costs may be higher for insured patients than for self-paying patients, especially for items outside fixed packages, which can affect the final bill.

For an in-depth read on the cashless claim process and benefits, refer to the linked guide.

How to Find Your Insurer’s Network Hospital List

If you're searching for terms like “HDFC Ergo Network Hospital” or “Aditya Birla Network Hospital”, here’s the easiest way:

- Go to your insurer’s official website.

- Search for “Health Insurance” if it’s a general insurer and click on the associated icon.

- Look for “network hospitals” or “cashless hospitals” as a clickable button or scroll down the page.

- Click on the “Locate Hospital Near You” button.

- Enter your city/PIN code/state.

- View the complete list.

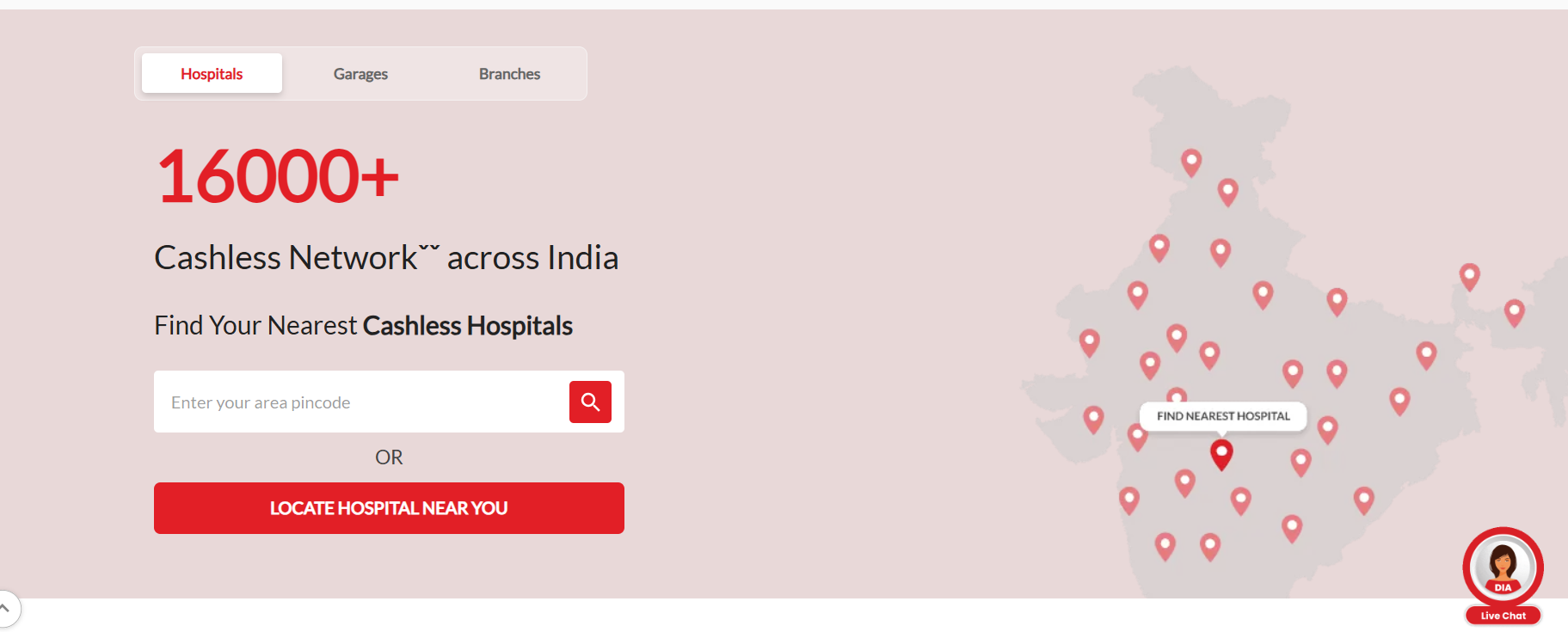

We’ve used HDFC ERGO’s website for this example. However, most insurer websites have similar steps to find their network hospital list, even though the interface may vary slightly. To save you time, here are the official links of some popular health insurers:

Direct Hospital Locator Links

Note: Some insurers like Niva Bupa go beyond basic details (like address and contact info) and also display additional insights such as number of beds, estimated treatment costs, hospital ratings, available specialties, and even claim-related statistics, making it easier to evaluate hospitals before choosing one.

If you’re comparing insurers based on hospital reach, here’s a quick snapshot:

Insurer-Wise Network Hospital Count

Note: Network hospital lists and counts are updated regularly, so it’s always best to check your insurer’s official website for the most accurate and latest details. Moreover, network hospital lists can change during the year due to pricing disputes between insurers and hospitals. A hospital listed today may not offer cashless later, so always reconfirm with them before planned admission.

Note: If you'd like to explore the detailed figures reported by insurers and the IRDAI in their annual disclosures and public reports, visit Ditto Data Labs, our proprietary repository of health insurance data, meticulously compiled, verified, and maintained by the Ditto team over the years.

Why Talk to Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- 100% Free Consultation

- Dedicated Claim Support Team

- Backed by Zerodha

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- No-Spam & No Salesmen

You can book a FREE consultation here. Slots are filling up quickly, so be sure to book a call now or chat on WhatsApp with us.

Ditto’s Take

Most people don’t think about network hospitals until they actually need one, and that’s when things get messy. In reality, a network hospital is what determines whether your experience is smooth and cashless or stressful and reimbursement-heavy.

A simple thumb rule: the best health insurance plans are the ones that give you access to the maximum number of good hospitals closest to where you live, work, or frequently travel. It’s not just about how many hospitals an insurer lists, but whether the right ones are easily accessible to you.

Behind the scenes, insurers actively negotiate with hospitals on things like which treatments are covered, disease-wise sub-limits (if any), and hospital stay costs. This helps them control rising medical expenses, but it also means your experience can vary depending on the hospital and plan you choose.

So before buying or renewing your policy, take a few minutes to check your insurer’s network hospital list, shortlist at least 4–5 reliable hospitals nearby, and prioritize accessibility over just a lower premium.

Frequently Asked Questions

Last updated on: