Many of us assume that our employer’s health insurance fully covers us. But the truth? It often falls short, especially when you need it the most. Maybe it doesn’t cover pre-existing conditions, perhaps you’re between jobs, or maybe you’re thinking long-term, and your company policy simply won’t keep up.

At Ditto, we hear this all the time. Our advisors speak to over 1,000 salaried professionals every month, and this is one of the biggest concerns that comes up. That’s why we decided to dig deep. We went through product brochures, premium charts, and claim settlement terms from 20+ top insurers. We also looked at real-life cases from people we've helped to figure out which policies truly deliver.

The result? A handpicked list of the best individual health insurance plans for salaried individuals in 2025, ranked by coverage, flexibility, premium value, and long-term benefits. Let’s get into it.

Heads up: It takes an average person up to 5 hours to read and analyze a policy and 10 hours or more to compare different plans and decide.

We propose a better alternative: a 30-minute FREE consultation with Ditto’s certified advisors. We have a spam-free guarantee and will never push you to buy a plan. Don’t delay—we have limited slots daily, so book a quick call here before they run out.

Why Corporate Health Insurance Policy is not Enough?

Before we get to the best individual health insurance plans for salaried individuals, let’s address a common question: “Why should I even bother buying personal health insurance when my company already gives me one?”

Here’s what a senior advisor at Ditto has to say about it:

“At first glance, a corporate health insurance policy seems like a great deal. It’s free, covers your family, and you don’t have to lift a finger to get it. But, here’s the catch: it’s not yours.

Corporate cover is tied to your job. The moment you switch jobs, retire, or if your company decides to cut costs, that insurance can vanish overnight, leaving you stranded. Worse, many of these policies offer limited coverage, sometimes just ₹2-3 lakhs, which may not be enough if a medical emergency strikes.

Moreover, let’s not forget about pre-existing diseases or maternity. Many corporate plans have long waiting periods or don’t cover these at all. Even when they do, the terms can be vague, and you might end up paying out of pocket.

In short, corporate health insurance works well until it doesn’t. That’s why more and more salaried professionals are choosing to supplement their employer coverage with an individual health policy, something they can genuinely rely on, regardless of their job status.”

Now that you know why your company policy might not be enough, we’ll break it down further by showing how a corporate plan compares with an individual health insurance plan.

Corporate Health Insurance Policy Vs Individual Health Insurance Policy

While one is the health cover your employer provides, the other is the policy that you buy and own yourself. Both have their benefits, but they’re built for different purposes. Understanding how they differ can help you decide whether relying only on your company policy is enough.

Here’s a quick comparison between your corporate health insurance policy and your individual one.

| Feature | Corporate Health Insurance | Individual Health Insurance |

|---|---|---|

| Ownership | Tied to your employer | Fully owned by you |

| Coverage Continuity | Ends when you leave the job or retire | Stays with you for life (Lifelong renewability) |

| Coverage Amount | Limited (₹2-5 lakhs) | You can choose the sum insured, which can go up to ₹1-2 crores |

| Premium Payment | Paid by employer or shared | Paid by you (eligible for tax benefits) |

| Customisation | Limited flexibility | Highly customizable with add-ons, super top-ups, etc |

| Pre-Existing Diseases | May not cover or come with more extended waiting periods | Can be covered with a proper 1-3 year waiting period |

| Maternity Coverage and OPD Coverage | Rare or restricted | Available in many plans |

| Claim Process | Managed by employer/TPA | Directly with the insurer or through your advisor/agent |

| Tax Benefits (Under 80D) | Not Available | Available |

The table clearly indicates how corporate health insurance is excellent for basic coverage while you’re employed, but it’s not built for long-term security. With limited coverage, no control over features, and the risk of losing it when you need it the most (like during job switches or retirement), it leaves a lot of gaps.

On the other hand, an individual policy is a safety net that stays with you no matter where you work or even if you stop working altogether. You not only get to choose the coverage to customize it to fit your lifestyle and needs, but also enjoy tax benefits.

| Put simply, corporate health insurance is limited and ends with your job. An individual plan stays with you, offers better coverage, and can be customized to your needs. |

At Ditto, we often advise folks to keep their corporate cover and buy a personal plan in their 30s. That way, you avoid high premiums loadings (say due to PEDs) later and serve waiting periods early.

Here are two real-life examples:

- Sneha’s Wake-Up Call

Sneha, a 32-year-old marketing manager, had always relied on her company’s health insurance. But when she quit her job to take a short sabbatical, she suddenly found herself uninsured.

Two months in, she had a minor surgery that cost ₹2.8 lakhs, entirely out-of-pocket. That’s when she decided to buy her own individual plan and got in touch with us. Today, even after joining a new company, she keeps both her employer’s policy and her own personal cover.

- Mr. Rao’s Retirement Reality Check

Mr. Rao, a 60-year-old retired employee, had always depended on his employer’s group health insurance. It worked fine until retirement. That’s when he decided to buy an individual health policy to stay protected. But here’s what happened:

- The premium was significantly higher because of his age.

- He had developed hypertension in his late 50s, which was now considered a pre-existing disease (PED).

- Due to this condition, many insurers either rejected his proposal or offered a plan with long waiting periods and a loading fee (extra premium).

Had Mr. Rao bought an individual policy in his 30s or 40s, his premiums would have been lower, and any pre-existing conditions would have already served their waiting periods by the time he needed the cover.

This is a wake-up call for many salaried individuals: the earlier you buy your own policy, the easier and cheaper it is. Waiting until retirement can cost you both money and peace of mind.

To sum it up, corporate health insurance is helpful, but it’s not designed for complete or lifelong protection. On the other hand, individual health insurance gives you control, consistency, and peace of mind, especially when life throws curveballs.

Now that you’ve seen the risks of relying only on your corporate plan, let’s answer the big question: why should salaried individuals start thinking about personal health insurance right now, even if they feel healthy and secure today?

Why do Salaried Individuals Need Individual Health Insurance Policies?

By now, it’s clear that employer-provided health insurance often leaves gaps, especially when your life changes. So, why exactly should salaried professionals take that extra step to buy their own individual policy? Here are the key reasons:

1) Portability and Continuity

Your individual plan is yours, regardless of your job changes, sabbaticals, or retirement. It renewable lifelong, year after year without a hitch, and your coverage stays intact even during transitions.

2) Flexibility to Choose the Right Coverage

Corporate plans are one-size-fits-most. But your life is unique, whether you’re single, married, planning a family, or have specific health concerns. With a personal policy, you get to choose:

- Sum insured that matches your lifestyle

- Add-ons like consumables cover, air ambulance, maternity, OPD, etc.

3) Better Premiums When You’re Younger

Buying a plan in your 30s or early 40s means lower premiums. The younger you are, the cheaper it is, so you should buy your health insurance before your age increases the premium costs.

4) Coverage for Pre-Existing Conditions

Most corporate plans have long waiting periods or exclude coverage for conditions like diabetes, hypertension, or thyroid disorders. An individual policy gives you a fresh waiting period and complete control, plus clarity on what’s covered and when.

5) Tax Advantages

Premiums for individual health policies qualify for deductions under Section 80D of the Income Tax Act (Under the old regime). That means you get health protection and save on taxes, something corporate cover doesn’t offer directly.

Salaried individuals who invest in an individual health policy get a reliable safety net, personalized coverage, long-term affordability, and tax benefits. These are advantages that corporate insurance just can’t fully provide.

| Think of your individual health plan as financial armor: portable, flexible, and future-ready. |

Now that we’ve nailed down why individual health insurance matters, it’s time to pinpoint which plans deliver the best value.

Best Individual Health Insurance Policies for Salaried Individuals in 2025

We shortlisted the best individual health insurance plans for salaried individuals using a practical, three-step approach. First, we studied detailed policy brochures and terms from 20+ top insurers, all updated as of May 2025. Then, we dug into real customer experiences, specifically analyzing over 1,500 claims filed by Ditto users in the last financial year to see how policies perform when it counts.

Finally, we rated each plan on key parameters like sum insured flexibility, hospital network strength, claim settlement process, room rent limits, and overall value for money. The result? A curated list of policies that offer the most reliable protection for salaried professionals today.

| Plan Name | PED Waiting Period | SI Waiting Period | Restoration | Renewal Bonus | Network Hospitals | CSR | ICR |

|---|---|---|---|---|---|---|---|

| HDFC ERGO Optima Secure | 3 years (add-ons reduce) | 2 years | 100% of base SI, once/year (addon: unlimited) | 50% pa, up to 100% (irrespective of claims) | 13k+ | 98% | 86% |

| Care Supreme | 3 years (add-ons reduce) | 2 years | Up to base SI, unlimited times | 50% pa, up to 100% (addon: up to 500% or unlimited accumulation) | 11.4k+ | 90% | 59% |

| Aditya Birla Activ One Max | 3 years (add-ons reduce) | 2 years | 100% of base SI, unlimited times | 100% pa, up to 500% (irrespective of claims) | 12k+ | 95% | 68% |

| Niva Bupa Aspire Titanium+ | 3 years (add-ons reduce) | 2 years | Unlimited restoration after first claim | Booster+: Carry forward unused cover up to 10x | 10k+ | 91% | 58% |

| ICICI Elevate | 3 years (add-ons reduce) | 2 years | Unlimited restoration of base cover | Addon: Up to unlimited renewal bonus | 10.2k+ | 85% | 83% |

In short, if you’re looking for features like maternity or OPD coverage, look for plans with strong add-on flexibility and low waiting periods. These features aren’t common in employer-provided plans, but many individual covers offer them as optional upgrades.

Not sure which plan to pick? Get in touch with us and we’ll help you find a policy that best fits your needs.

Why Choose Ditto for Health Insurance?

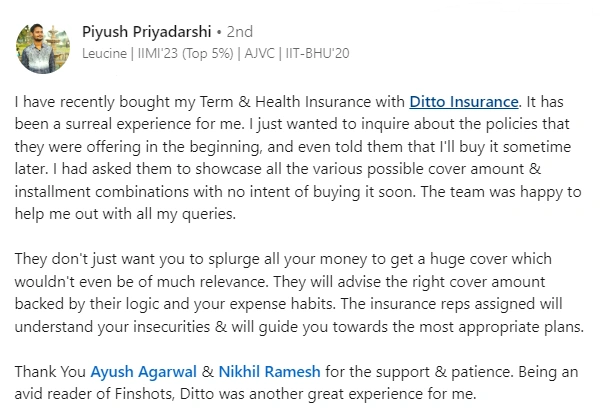

At Ditto, we’ve assisted over 7,00,000 customers with choosing the right insurance policy. Why customers like Piyush below love us:

✅No-Spam & No Salesmen

✅Rated 4.9/5 on Google Reviews by 12,000+ happy customers

✅Backed by Zerodha

✅100% Free Consultation

You can book a FREE consultation here. Slots are filling up quickly, so be sure to WhatsApp or book a call now.

Conclusion

Relying solely on your corporate health insurance can leave you vulnerable when life takes an unexpected turn, be it a job change, sabbatical, or retirement. An individual health insurance policy, on the other hand, offers consistent, customizable, and lifelong coverage that grows with your needs. The sooner you invest in one, the better protected and more financially secure you’ll be in the long run.

Key Takeaways:

- Corporate cover isn’t permanent: It ends when your employment does, leaving you exposed during transitions.

- Buying early saves money: Premiums are lower and loadings can be avoided, and waiting periods can be served while you’re healthy.

- Individual policies offer control: You get to choose the coverage, add-ons, and enjoy tax benefits under Section 80D.

Ready to protect your health beyond your job? Book a free 1:1 call with a Ditto advisor and get unbiased, expert help in choosing the perfect health insurance policy for you. No spam. No pressure. Just clarity.

Last updated on: