Quick Overview

A claim rejection often comes at the worst possible moment, right when you expect your insurance to step in. But in many cases, it is not random and traces back to small, avoidable gaps. Even a cashless denial can feel like the end, but it is not always a rejection. If treatment happens at a non-network hospital, you can file a reimbursement claim. This guide breaks down why claims get rejected and how you can reduce the risk.

Why Do Health Insurance Claims Get Rejected?

Health insurance claims are usually rejected when the treatment, timing, or documentation does not match the policy terms. Understanding these reasons can help avoid unpleasant surprises during a claim.

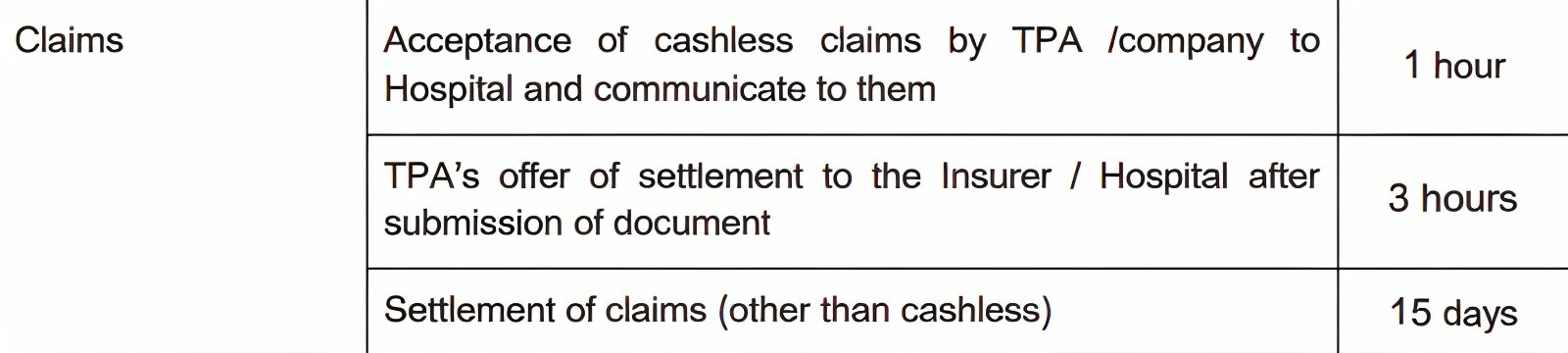

Here’s a snippet of claim settlement timelines as per the IRDAI master circular:

At Ditto, we have seen many claim denials and delays simply due to Indoor Case Papers (ICP) or a treating doctor’s note justifying hospitalization being missing. These reasons also include missing International Classification of Diseases (ICD) codes on discharge summaries and the absence of a Medico-Legal Case (MLC) report in accident cases.

Did You Know?

Top Reasons for Health Insurance Claim Rejection

- Non-Disclosure: If you do not fully disclose health conditions like diabetes, past surgeries, or habits like smoking at the time of buying the policy, the insurer can reject your claim later.

- Treatment during Waiting Period: Claims made during waiting periods are always denied. This includes the initial 30-day period, specific disease waiting periods (2 years), and PED waiting periods (3 years).

- Policy Not Active or Lapsed: If your policy has expired due to missed premium payments, claims will not be accepted. Always ensure your policy is active at the time of hospitalization.

- Non-Network Hospital Without Intimation: If you plan to get treated at a non-network hospital without informing the insurer can lead to complications or rejection. The insurer will reject your claim if you get treated at a blacklisted hospital.

- Treatment Not Covered or Excluded: Procedures like cosmetic or infertility treatments are often standard exclusions unless specifically covered. Separately, claims can also be denied if hospitalization is not medically necessary. It is important to distinguish these from permanent exclusions, which apply to specific conditions listed in your policy.

- Incorrect or Incomplete Documentation: Missing bills, wrong details, or incomplete paperwork can delay or even lead to rejection of claims. Administrative errors are more common than people realise.

- Fraud or Inflated Claims: Any sign of fake bills, inflated expenses, or manipulated records can lead to outright rejection. Insurers take fraud very seriously and may investigate such cases thoroughly. Inconsistencies between the discharge summary, doctor’s notes, diagnosis, or other medical records can lead to claim issues.

- Hospitalization Not Medically Necessary: Even if a condition is covered, claims can be rejected if the insurer’s clinical team finds the admission unnecessary. This commonly happens in cases like fever or backache treatments, where hospitalization may not be justified, and treatment can be done on an outpatient department basis.

- Cashless Claim Put on Hold for Review: A cashless request can get declined if the insurer needs more time to review the case. This usually means they require additional medical records or clarification before they can take a final call.

- Complications Linked to Waiting Period: Even if you get treated for a complication, the claim may be rejected if it is connected to a pre-existing condition that is still within the waiting period.

- Deductible Not Met in Top-Up Plans: In top-up or super top-up plans, the insurer pays only after the deductible is crossed. If your claim amount is below this limit, the claim will not be paid.

How to Avoid Claim Rejection: Key Steps Before & During Hospitalization

Disclose Everything Upfront

Be completely honest at the time of purchase. Even small omissions can lead to claim rejection later. If you are diagnosed with any new health condition after buying the policy, it is advisable to inform your insurer proactively.

Prefer Network Hospitals for Cashless

Choose a network hospital whenever possible. It simplifies the process and reduces out-of-pocket expenses. Non-network hospitals usually mean reimbursement and more paperwork.

Get Pre-authorization Early

For planned treatments, inform the insurer in advance and get approval within 1 hour. Early pre-authorization reduces last-minute stress and improves the chances of a smooth, cashless claim.

Keep Your Policy Active

Always renew on time. Continuity protects your waiting periods, bonuses, and claim eligibility. Missing a renewal can reset these benefits and create problems during claims.

Avoid Unnecessary Policy Switches

Do not replace a good policy casually. Portability helps retain benefits like waiting period credits, but frequent changes can still create confusion and gaps.

Read the Customer Information Sheet (CIS) carefully

Do not rely only on brochures. Go through the CIS to understand coverage, exclusions, and the claim process.

What to Do If Your Health Insurance Claim Is Rejected?

If your claim is rejected, stay calm and understand the exact reason. Then review and organize all documents to identify gaps and prepare for correction, resubmission, or escalation.

- Raise a Complaint with the Insurer: Submit a written grievance or approach a grievance redressal officer (GRO) along with all documents, like policy copy and discharge summary. Insurers are expected to review and respond within 30 days. You can also contact your third-party administrator, if required.

- Escalate Through Bima Bharosa: If the response is delayed or unsatisfactory, register a complaint on IRDAI’s Bima Bharosa portal. You can also reach out via helpline or email. This step helps push for faster resolution.

- Approach the Insurance Ombudsman: If the issue still remains unresolved, you can file a complaint with the insurance ombudsman. This is a free process, available if the insurer fails to respond within 30 days or if the reply is not satisfactory.

Note: As per IRDAI guidelines, claims cannot be refused without the approval of a claim review committee. You can ask your insurer for proper justifications and the exact policy clause used for claim rejection.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam and No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or connect with us on WhatsApp.

Conclusion

A claim rejection during hospitalization can feel overwhelming, but it is not the end of the road. Such issues can be resolved with the right documents and timely follow-ups. Most importantly, being completely honest during underwriting helps prevent such situations in the first place.

Choosing an established health insurer can also mean better support and fewer disputes. If you are looking for a reliable health insurer, explore our guide on the best health insurance companies.

Frequently Asked Questions

Last updated on: