The top health insurers with low complaints have great track records. Bajaj General Insurance, IndusInd General, and New India Assurance have consistently reported some of the lowest complaint ratios. Bajaj General leads with 3.07 complaints per 10,000 claims (average FY 2022-25), followed by IndusInd General at 4.31. Other insurers among the top 10 health insurance companies with the lowest complaints include ICICI Lombard, HDFC ERGO, and Generali Central.

At Ditto, we prefer general health insurers that report fewer than 20 complaints per 10,000 claims while choosing the best health insurance plans. For Standalone Health Insurers (SAHIs), we prefer insurers with less than 40 complaints per 10,000 claims. This guide is perfect for those exploring health insurers that offer a seamless customer experience.

When it comes to health insurance, the real test begins when a claim is filed. While policy features and premiums are easy to compare, complaint data offers a deeper look into an insurer's service quality, claims handling efficiency, and overall customer experience when it matters most.

In the next few minutes, this guide will break down the top 10 health insurance companies with the lowest complaint volumes and explain other insurer metrics to evaluate alongside complaint records.

Note: For general insurance companies like HDFC ERGO, complaint data is reported at the insurer level and includes grievances across all product lines, such as health, motor, travel, and other retail insurance products. The above figures are sourced from the insurer’s public disclosure.

The figures presented are based on the latest publicly available data up to FY 2024–25. Data for FY 2025–26 has not yet been fully released and is currently being compiled and published by insurers.

How We Ranked Insurers: Complaints per 10,000 Claims

One of the key metrics we track is complaints per 10,000 claims, which measures the number of grievances raised relative to the claims handled by an insurer. We prefer this metric over complaints per 10,000 policies because it focuses on the claims experience, where health insurance delivers its real value.

To reflect the differing levels of complexity in claims handling across insurer types, Ditto applies separate complaint benchmarks and thresholds for General Insurers and Standalone Health Insurers (SAHIs).

1) General Insurance Companies: Ditto Benchmark < 20

Health insurance claims often involve pre-authorizations, medical underwriting, hospital coordination, and claim assessments. Their broader business mix and larger operational scale allow us to apply a stricter benchmark. As the complaints data is evaluated at the insurer level across all product categories, all insurers featured in our top 10 list are general insurers.

2) Standalone Health Insurers (SAHIs): Ditto Benchmark < 40

Standalone Health Insurers like Care and Aditya Birla deal primarily with health claims, which are often more complex and involve multiple stakeholders, including hospitals, doctors, and policyholders. Additionally, insurers like Manipal Cigna Health Insurance use Third Party Administrators (TPAs) for claim assistance. To account for this added complexity, we use a slightly higher threshold.

Insurer

Complaints per 10,000 Claims (Average FY 2022-25)

Aditya Birla Health Insurance

18.67

Care Health Insurance

42.00

Manipal Cigna Health Insurance

23.50

Niva Bupa Health Insurance

42.85

Star Health & Allied Insurance

52.31

Note: The above data are sourced from the insurer’s public disclosure. Data is not available for Galaxy Health Insurance and Narayana Health Insurance, as both insurers are new to the market.

Why Complaint Volume Matters More Than CSR Alone

01

CSR Shows Outcomes, Complaints Show the Journey

A claim may be marked as settled and still involve delays, repeated document requests, or communication issues. Complaint data helps reveal what customers actually experienced during the process.

02

Captures Real Customer Friction

High complaint levels often point to problems such as claim disputes, slow approvals, cashless authorization delays, or poor grievance handling. CSR alone cannot highlight these issues.

03

Reflects Service Quality During a Claim

Health insurance claims involve hospitals, TPAs, doctors, and insurers. Complaint ratios provide insight into how effectively an insurer coordinates these stakeholders when a policyholder needs assistance.

04

Highlights Consistency in Claims Handling

Two insurers may have similar CSR figures, but one may generate significantly fewer complaints. This often suggests a smoother and more predictable claims experience.

05

Measures What Policyholders Care About

Most customers remember how their claim was handled, not the insurer's CSR. Complaint data provides a practical view of responsiveness, transparency, and customer support.

Take Note: If you face delays, disputes, or unresolved issues during a health insurance claim, you can escalate the matter through IRDAI's Bima Bharosa Portal. The platform allows policyholders to register complaints, track grievance status in real time, and seek resolution directly through a regulator-backed system after exhausting the insurer's internal grievance process.

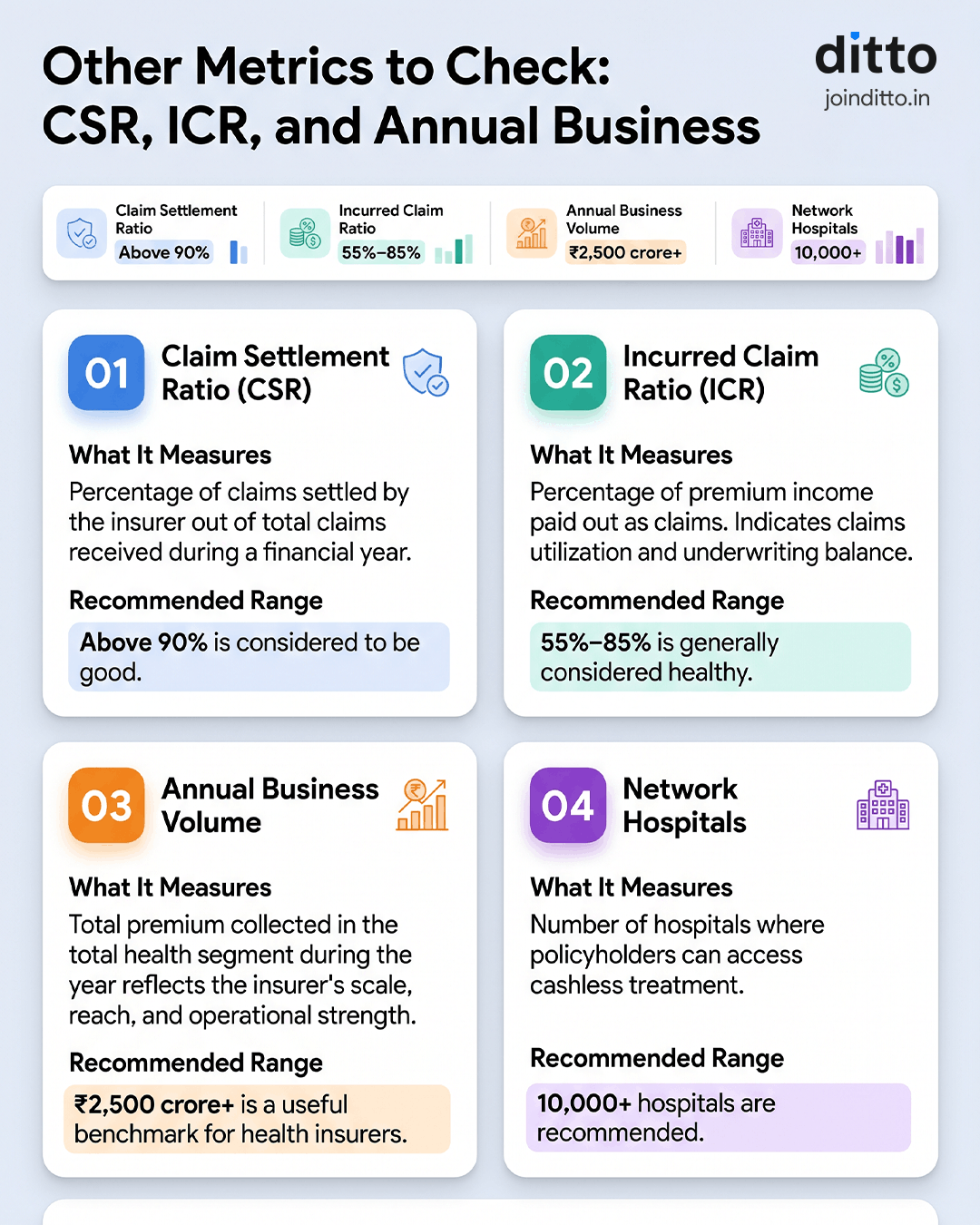

Other Metrics to Check: CSR, ICR, and Annual Business

While complaints per 10,000 claims offer valuable insight into customer experience, they should never be evaluated in isolation. A comprehensive assessment also includes the claim settlement ratio, incurred claim ratio, and annual business volume, which together help measure claims reliability, financial sustainability, and insurer scale.

See the infographic below for a quick breakdown of what each metric means and how to interpret it when comparing health insurers.

Note: If you'd like to explore the detailed figures reported by insurers and the IRDAI in their annual disclosures and public reports, visit Ditto Data Labs, our proprietary repository of health insurance data, meticulously compiled, verified, and maintained by the Ditto team over the years.

How to Choose the Best Health Insurance Company for You

Evaluate the insurer's claims track record using metrics such as CSR, ICR, and complaints per 10,000 claims.

Prefer insurers with robust network hospitals, especially hospitals that are relevant to your city and healthcare needs.

Check whether the insurer offers modern policy features such as restoration benefits, no room-rent restrictions, and a comprehensive bonus.

Review the insurer's financial strength and scale through the solvency ratio and annual business volume.

Compare the quality of customer support and claims assistance, especially during hospitalization and claim settlement.

Red Flags to Watch Out for Before You Buy

Policies with restrictive room-rent limits, disease-wise limits, or multiple hidden sub-limits.

Mandatory co-pay clauses that significantly increase out-of-pocket expenses, especially for senior citizens.

Frequent dependence on TPAs for claims management without strong insurer-led in-house claims support.

Insurers with a history of consistently high complaint ratios relative to the number of claims handled.

Policies with limited restoration benefits, especially those that do not cover related illnesses.

Why Talk to Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 24,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Conclusion

Low complaint volume does not automatically make an insurer the best choice, but it is one of the strongest indicators of a smoother claims experience. At Ditto, we believe the best health insurers combine low complaint ratios with strong claims metrics, extensive hospital networks, robust policy features, and sound financial strength.

When multiple insurers offer similar coverage and pricing, consistently lower complaints can be the deciding factor. After all, a health insurance policy is only as good as the experience you have when you need to make a claim.

Disclaimer

We strive to maintain the highest standards of accuracy across our articles, guides, rankings, and insurer comparisons. All data is sourced from publicly available disclosures, regulatory filings, and official insurer publications. If you identify any factual errors, outdated information, or discrepancies, please contact our Editorial Team at editorial@joinditto.in for review.

Please Include:

Source URL: The exact webpage, report, filing, or document containing the relevant information.

Identified Discrepancy: The specific metric, figure, ranking, statement, or section that requires correction or updating.

Supporting Evidence: Official regulatory filings, insurer disclosures, annual reports, statutory returns, or other credible documentation that substantiates the proposed change.

Frequently Asked Questions

Which health insurance company has the lowest complaints in India?

Based on IRDAI disclosures for FY 2022–25, Bajaj General Insurance reported the lowest complaint ratio among major health insurers, averaging just 3.07 complaints per 10,000 claims. IndusInd General and New India Assurance also reported relatively low grievance levels during this period. Complaint ratios offer valuable insight into the actual claims experience because they reflect disputes raised by policyholders and claimants. At Ditto, we generally prefer General Insurers with fewer than 20 complaints per 10,000 claims and Standalone Health Insurers (SAHIs) with fewer than 40. Bajaj sits comfortably within this benchmark.

What are the complaints per 10,000 claims in health insurance?

Complaints per 10,000 claims measure the number of grievances filed per 10,000 claims handled by an insurer. The metric is published through insurer disclosures submitted to IRDAI and provides insight into the quality of the claims experience. A lower ratio often indicates fewer disputes, better communication, and smoother claims servicing. Unlike marketing material or product brochures, complaint data reflects actual customer experiences after a claim is filed. At Ditto, we consider this metric particularly important because health insurance is ultimately a claims product, and its true value becomes evident only during hospitalization.

Why is the Claim Settlement Ratio (CSR) not enough to compare health insurers?

Claim Settlement Ratio (CSR) tells you how many claims an insurer settled, but it does not reveal how smooth or difficult the process was. Two insurers may report similar CSR figures while delivering very different customer experiences. Complaint data helps bridge this gap by highlighting delays, disputes, and servicing issues. At Ditto, we recommend evaluating CSR alongside Incurred Claim Ratio (ICR), complaint ratios, network hospitals, and policy features. A high CSR is certainly desirable, but relying on it alone can provide an incomplete picture of how the insurer performs when policyholders actually need support.

What is the Ditto benchmark for health insurance complaint ratios?

At Ditto, we use separate complaint benchmarks for different insurer categories. For general insurance companies, we prefer fewer than 20 complaints per 10,000 claims. For standalone health insurers, we use a slightly higher threshold of fewer than 40 complaints per 10,000 claims, given the added complexity of health-only operations. These benchmarks recognize that health claims often involve hospitals, doctors, third-party administrators, pre-authorizations, and multiple stages of documentation. While no single metric can determine insurer quality, consistently staying below these thresholds generally indicates stronger claims servicing and more effective grievance resolution.

What is the difference between General Insurers and Standalone Health Insurers?

General Insurers offer multiple insurance products, such as health, motor, and home insurance. Standalone Health Insurance Companies (SAHIs) focus primarily on health insurance products, but also offer travel and personal accident insurance. Because SAHIs handle only health-related claims, they often manage more complex claim journeys involving hospitals, medical records, and treatment approvals. This can naturally result in higher complaint levels. At Ditto, we account for these differences by applying separate complaint benchmarks. While both insurer categories are regulated by IRDAI, understanding their operating models helps buyers compare complaint ratios and claims performance more fairly.

What is ICR in health insurance, and what should it be?

ICR, or Incurred Claim Ratio, measures the proportion of premium income paid out as claims during a financial year. It is one of the key indicators of how an insurer manages risk and claims. At Ditto, we generally prefer an ICR between 55% and 85% when evaluating the top 10 best health insurance company in India. A very low ICR may suggest limited claims utilization, while an excessively high ICR could indicate pressure on profitability and sustainability. ICR works best when evaluated alongside complaint ratios, CSR, solvency ratios, and policy features to understand the insurer's overall claims performance.

How do I choose the No 1 health insurance company in India?

Start by reviewing claims-related metrics such as complaint ratios, CSR, and ICR. Next, check whether the insurer has a strong cashless hospital network, ideally with 10,000 or more hospitals. Evaluate policy features such as unlimited restoration, no-claim bonus, room-rent flexibility, and daycare coverage. Financial metrics such as the solvency ratio and annual business volume can also provide useful insights into insurer stability. At Ditto, we do not recommend insurers based on a single metric. Instead, we assess claims performance, customer experience, policy design, financial strength, and operational scale together before recommending a health insurance plan.

What is a cashless hospital network, and how many hospitals should my insurer have?

A cashless hospital network consists of hospitals where the insurer directly settles eligible treatment expenses with the hospital. This reduces the need for policyholders to make large upfront payments and seek reimbursement later. At Ditto, when evaluating the top 10 health insurance company in India, we prefer insurers with access to at least 10,000 network hospitals. However, the quality and relevance of the network matter just as much as the number. Before purchasing a policy, check whether reputed hospitals in your city are included.

How do I escalate a health insurance complaint or a rejected claim?

Health insurance grievances follow a structured escalation process. Start by raising the issue with your insurer's Grievance Redressal Officer (GRO), who is generally expected to respond within 15 days. If the resolution is unsatisfactory, escalate the complaint through IRDAI's Bima Bharosa Portal, which allows you to track the grievance and ensures regulatory oversight. If the dispute remains unresolved after the insurer's response period, you can approach the Insurance Ombudsman, a free dispute-resolution forum for eligible cases. For larger disputes or matters beyond the Ombudsman's scope, you may approach the appropriate Consumer Commission under the Consumer Protection Act, 2019.

Which health insurance company is best in India?

There is no single best health insurance company for everyone because the right choice depends on your age, medical history, city, budget, and coverage needs. The best health insurance company in India as per claim settlement is New India Assurance, but the insurer operates with very few network hospitals (3,700+). At Ditto, we recommend evaluating insurers based on a combination of factors, including CSR, ICR, complaints per 10,000 claims, network hospitals, policy features, and financial strength. Insurers such as HDFC ERGO, Care, and Aditya Birla Health Insurance perform well across multiple parameters.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.