Choosing an insurer with a low complaint volume can lead to a hassle-free claims experience. Industry reports indicate that HDFC Life, SBI Life, and Tata AIA lead the Indian market with low registered claim complaints. Other insurers such as IndusInd Nippon Life (formerly Reliance Nippon), Bajaj Life, Axis Max Life, and ICICI Prudential Life have consistently also reported relatively low complaints per 10,000 claims.

The top 10 term insurance companies with the lowest complaints have also maintained competitive claims performance. At Ditto, when evaluating term plans, we prefer insurers that report fewer than 20 complaints per 10,000 claims, as this can indicate a smoother claims experience and stronger grievance-resolution process. This guide suits those who want to explore term insurers who provide an excellent customer experience.

A term insurance claim is filed only once in a lifetime, which makes the reliability of an insurer's claims experience extremely important. While claim settlement ratios often grab attention, complaint data can reveal how smoothly insurers handle claims, communicate with families, and resolve disputes when it matters most.

This guide breaks down the top 10 term insurance companies with the lowest complaint volumes, explains how the rankings are calculated, and highlights other metrics that matter when evaluating insurer reliability.

Need help selecting a term insurer that offers a seamless customer experience? Book a free call or chat on WhatsApp with a Ditto advisor, and let us help you out.

How We Ranked Insurers: Complaints per 10,000 Claims

At Ditto, we place emphasis on complaints per 10,000 claims because term insurance is ultimately a product we want to judge by claims. A low complaint ratio indicates smooth claim processing and effective grievance resolution during one of the most critical interactions a family has with an insurer.

It is worth noting that insurers also publish complaints per 10,000 policies. This is a useful service-quality metric that captures broader customer experience issues such as policy servicing, premium payments, and support interactions.

Top 10 Term Insurance Companies With the Lowest Complaints

Note: The complaint data presented in the table relates to the insurer's overall life insurance business and is not limited to its term insurance products. Since insurers do not separately disclose complaint metrics for individual products, these figures should be interpreted as a measure of the insurer's overall service and claims experience. The figures are sourced from the insurer’s public disclosure.

The figures presented in the table are based on the latest publicly available data up to FY 2024–25. Data for FY 2025–26 has not yet been fully released and is currently being compiled and published by insurers.

CTA

Why Complaint Volume Predicts Claim Reliability

Claims Are the Ultimate Moment of Truth: A term insurance policy is purchased today, but its value is tested only when a death claim is filed. Complaint data offers insight into how smoothly insurers handle this crucial process.

Highlights Potential Friction Points: Higher complaint volumes can indicate delays, communication gaps, documentation issues, or disputes during the claims journey. Lower complaint ratios often suggest a more streamlined experience.

Measures Real Customer Outcomes: Unlike marketing claims or product brochures, complaint metrics are based on actual customer interactions. They reflect the experiences of policyholders, nominees, and claimants.

Provides Context Beyond Claim Settlement Ratio: A high claim settlement ratio is important, but it does not reveal how easy or difficult the claim process was. Complaint data adds another layer of insight into service quality.

Indicates Strength of Claims Infrastructure: Insurers with efficient claims teams, clear processes, and responsive support channels often report lower complaint levels. This can be a sign of stronger operational capabilities.

Did You Know?

The Bima Bharosa Portal, launched by IRDAI, allows policyholders to register, track, and escalate insurance complaints online. It provides real-time grievance status updates and serves as a centralized platform for resolving disputes across insurers.

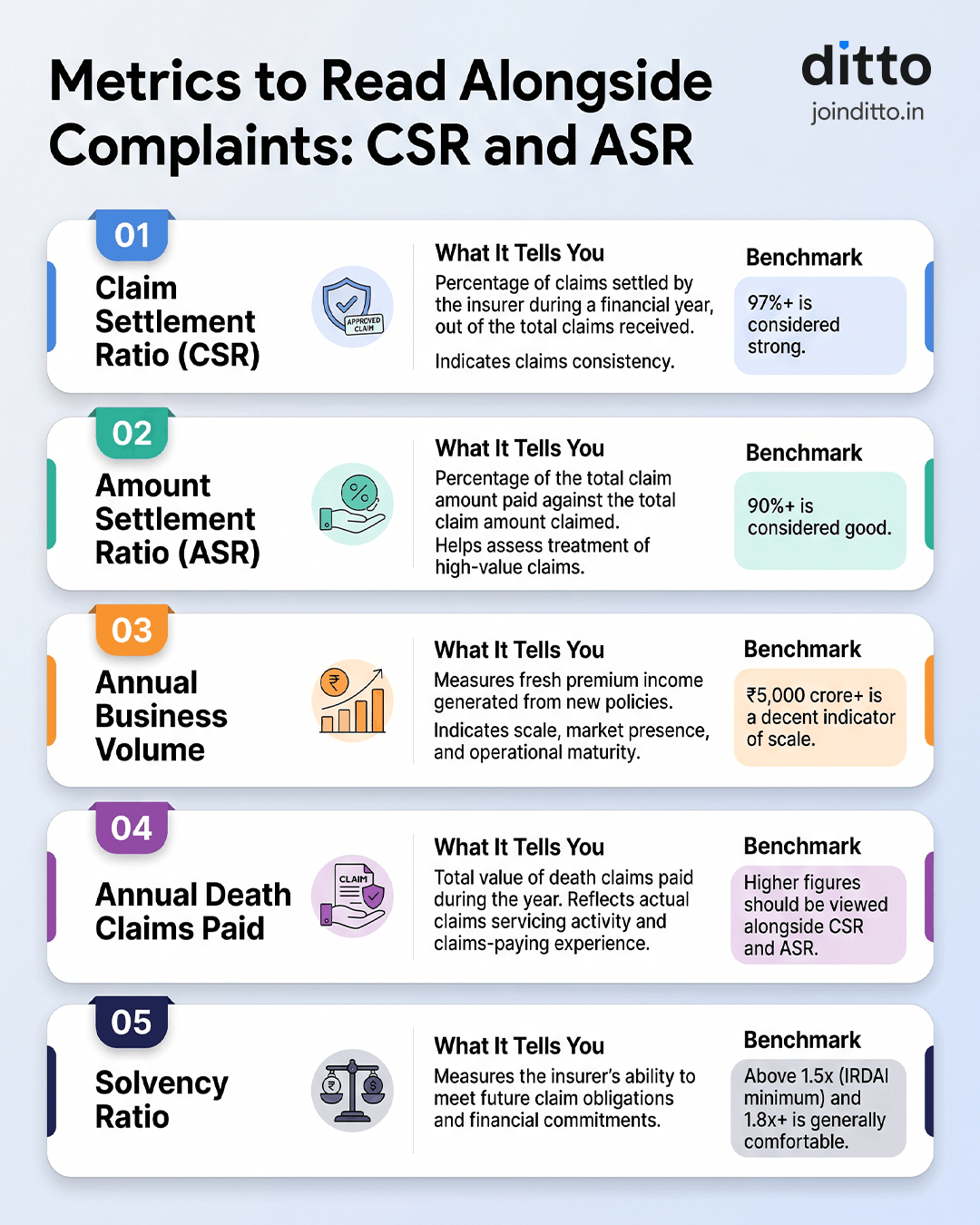

Metrics to Read Alongside Complaints: CSR and ASR

Complaint numbers tell you about customer experience, but they do not reveal the full claims picture. Claim Settlement Ratio (CSR) shows how often claims are settled, while Amount Settlement Ratio (ASR) indicates how much of the claimed amount insurers actually pay.

To get a balanced view of insurer performance, review complaints, CSR, and ASR together. The infographic below explains the insurer metrics in detail.

How to Choose the Best Term Insurance Company for You?

01

Start with Claims Performance

Look at metrics such as CSR and ASR. These provide insight into how consistently and fairly an insurer settles claims.

02

Check Complaint Levels

Review complaints per 10,000 claims to understand the quality of the claims experience. Lower complaint ratios often indicate smoother claim handling and better customer support.

03

Evaluate Insurer Scale

Consider annual business volume, annual death claims paid, and overall market presence. Larger insurers often have more established claims and servicing infrastructure.

04

Compare Product Features

Look beyond premiums. Term insurance comparison includes evaluating policy features, rider options, payout flexibility, and any exclusions or limitations that may affect coverage.

05

Review Financial Strength

Check the insurer's solvency ratio. A healthy solvency position indicates the insurer has adequate financial resources to meet future claim obligations.

Common Mistakes When Comparing Term Insurers

Confusing brand popularity with insurer quality. A heavily advertised insurer is not necessarily the best choice for claims support, underwriting, or long-term reliability.

Looking only at the insurer and ignoring the policy. Two plans from different insurers can vary significantly in terms of riders, exclusions, payout options, and flexibility.

Ignoring underwriting philosophy. Some insurers are stricter during policy issuance, while others may ask fewer questions initially but scrutinize claims more closely later.

Focusing on today's premium instead of long-term suitability. Term insurance is a decades-long commitment, so the insurer's stability and service quality often matter more than a small difference in premium.

Assuming all claim experiences are identical. The quality of communication, documentation support, and nominee assistance can vary meaningfully between insurers and may only become apparent when a claim is filed.

Comparing claim settlement ratios without checking complaint volumes, amount settlement ratios, and solvency levels.

Selecting a policy with insufficient cover that may not keep pace with future income replacement needs.

Ignoring policy wording, exclusions, waiting periods, and claim documentation requirements.

Assuming all riders add value without assessing whether they match your financial risks and goals.

Providing incomplete or inaccurate information about health, income, occupation, smoking, or lifestyle habits during the application.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 25,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Complaint ratios offer valuable insight into an insurer's real-world claims experience. While no single metric can identify the best insurer, consistently low complaints alongside strong CSR, ASR, solvency, and scale often indicate a well-run insurer. Use complaints as an important filter, but always evaluate them as part of a broader assessment.

If you wish to explore some established term insurers with a smooth customer experience, refer to our guide on the best term insurance companies in India in 2026.

Disclaimer

We make every effort to ensure that the information presented in our articles, guides, and insurer comparisons is accurate, up to date, and based on publicly available sources. If you identify any factual inaccuracies, outdated metrics, or data discrepancies, please reach out to our Editorial Team at editorial@joinditto.in for review.

Please Include:

Source URL: The exact webpage, report, or document containing the relevant information.

Identified Discrepancy: The specific metric, statement, figure, ranking, or section that you believe requires correction.

Supporting Evidence: Official regulatory filings, insurer disclosures, annual reports, statutory returns, or other credible documentation that supports the proposed update.

Frequently Asked Questions

Which term insurance company has the lowest complaints in India?

Based on FY 2022–25 public disclosures, HDFC Life, one of the top term insurance companies in India, reported the lowest complaints among major term insurers, averaging just 1.33 complaints per 10,000 claims. Aditya Birla Sun Life and IndusInd Nippon Life (formerly Reliance Nippon) also reported very low complaint levels during this period. Complaint ratios are important because they provide insight into the actual claims experience of policyholders and nominees. At Ditto, we generally prefer insurers with fewer than 20 complaints per 10,000 claims.

What are the complaints per 10,000 claims, and why does it matter for term insurance?

Complaints per 10,000 claims measures the number of grievances raised for every 10,000 claims handled by an insurer. It is one of the most practical ways to assess the quality of the claims experience. A lower number often indicates fewer disputes, better communication, and more efficient claim processing. This metric is especially relevant for term insurance because the policy's true value is tested only when a claim is filed. At Ditto, we consider complaint ratios alongside claims metrics such as CSR and ASR to identify insurers that are more likely to offer a smoother experience for nominees.

Is the term insurance Claim Settlement Ratio (CSR) enough to compare term insurers?

No. CSR is important, but it tells only part of the story. CSR measures the percentage of claims settled during a financial year, but it does not reveal how easy the process was or whether the full claim amount was paid. To get a more complete picture, you should also consider the ASR, complaint levels, solvency ratio, and overall claims reputation. At Ditto, we recommend evaluating multiple metrics together because an insurer with a strong CSR but a poor complaint record may still create challenges for policyholders and nominees during the claims process.

What is the amount settlement ratio in term insurance?

The amount settlement ratio measures the percentage of the total claim amount paid by an insurer compared to the total amount claimed during a financial year. Unlike the claim settlement ratio, which simply counts whether a claim was settled, the amount settlement ratio provides insight into whether high- and low-value claims are being treated fairly. An amount settlement ratio above 90% is generally considered strong. At Ditto, we consider the amount-settlement ratio an important complement to the claim-settlement ratio when comparing term insurers.

What is the Ditto benchmark for complaints per 10,000 claims?

At Ditto, we generally prefer insurers that report fewer than 20 complaints per 10,000 claims. This benchmark is not a regulatory requirement but a practical threshold based on our analysis of industry data. Insurers below this level often demonstrate better claims communication, smoother grievance resolution, and a more consistent customer experience. Many leading insurers fall comfortably within this range. While complaint ratios should never be viewed in isolation, they provide useful context when combined with CSR, ASR, solvency ratios, and overall claims performance. Together, these metrics help create a more balanced assessment of the insurer.

How do I choose the best term insurance company in India?

Choosing the best term insurance company requires more than comparing premiums. Start by reviewing the claim settlement ratio, amount settlement ratio, complaint levels, and solvency ratio. Next, evaluate the insurer's scale through metrics such as annual business volume and death claims paid. It is also important to review policy features, term rider options, payout flexibility, and exclusions. At Ditto, we believe no single metric can identify the best insurer. The ideal choice balances claims reliability, customer experience, financial strength, and product suitability. The goal is to find an insurer your family can depend on when a claim is eventually filed.

Why should I not just pick the cheapest term insurance plan?

The cheapest policy is not always the best value. A small premium saving today may not compensate for poor claims support, weaker customer experience, or a less suitable policy structure. Term insurance is a long-term contract that could remain active for several decades. What matters most is whether the insurer can support your family efficiently when a claim arises. At Ditto, we recommend looking beyond premiums and evaluating claims metrics, complaint ratios, solvency, and service quality. In most cases, a slightly higher premium may be worthwhile if it comes with a stronger claims experience. Additionally, premiums are locked in for the entire term once you purchase a term plan.

Where does the complaints per 10,000 claims data come from?

Complaints per 10,000 claims data come from insurer disclosures submitted to IRDAI. Insurers publish these figures through regulatory filings, including Form L41, which are available in the public domain. Because these disclosures are standardized and regulator-monitored, they provide one of the most reliable ways to compare grievance levels across insurers. At Ditto, we use publicly available data from multiple years to identify long-term trends rather than relying on a single year's performance. This helps reduce the impact of temporary fluctuations and provides a more balanced assessment of insurer service quality.

If a term insurance claim is rejected or delayed, where should I file a complaint?

A term insurance grievance follows a structured escalation process, not three separate options. First, raise the issue with the insurer's Grievance Redressal Officer (GRO). The insurer is generally expected to respond within 15 days. If the response is unsatisfactory or delayed, escalate the complaint through IRDAI's Bima Bharosa Portal, which tracks and monitors grievance resolution. If the dispute remains unresolved, you can approach the Insurance Ombudsman, a free dispute-resolution body that can hear eligible insurance complaints. For life insurance policies, nominees, legal heirs, and assignees can also file grievances.

Can the Insurance Ombudsman handle all term insurance claim disputes?

Not always. The Insurance Ombudsman can only consider complaints where the compensation sought is within the prescribed monetary limit. Many modern term insurance policies offer coverage of ₹1 crore, ₹2 crore, or even higher, which may exceed the Ombudsman's jurisdiction. In such cases, nominees may need to approach a Consumer Commission under the Consumer Protection Act, 2019, or pursue other legal remedies. This highlights why insurer selection is so important. A strong claims track record, low complaint volume, and reliable claims servicing can reduce the likelihood of your family facing a prolonged dispute over a large claim.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.