Overview

IndusInd General Insurance isn't among the top-tier health insurers in India, but it has a few plans worth considering. This is especially true if you're covering a large family or need health coverage that extends overseas.

You may know it better as Reliance General Insurance. The Hinduja Group acquired the company in 2025 and rebranded it. If you're an existing policyholder, nothing about your coverage has changed.

The new ownership has also put in ₹100 crore in fresh capital, nudging the solvency ratio up from 1.59x to 1.73x by September 2025. It's not the strongest in the industry, but it does show that the new promoters are investing in the company's financial health.

So is IndusInd worth buying? This review covers what the insurer does well, where it falls short, and whether Ditto recommends its plans.

IndusInd Health Insurance: Performance Metrics

Source: IRDAI annual reports and IndusInd’s public disclosures.

Note: The complaint numbers here aren't exclusive to health insurance. IndusInd General Insurance publishes a single complaint figure across all its products (health, motor, and others) combined.

Key Insights

- CSR: IndusInd’s CSR is below the ideal 90% benchmark, meaning a relatively higher number of claims don't get settled. If you file a claim, there's a real chance it could be delayed, receive a partial payment, or be outright rejected.

- ICR: At levels above the recommended range of 50%-80%, IndusInd is paying out a large share of its premium collections as claims. That's not bad for you right now, but it does raise the possibility of premium increases down the line to keep the business sustainable.

- Complaint Volume: Customers rarely face service issues, and that's a big deal when you're navigating hospitals and paperwork during an already stressful time.

- Annual Business: Growth has been inconsistent, and the recent rebrand adds another layer of uncertainty. It's worth keeping an eye on how the company stabilizes over the next couple of years.

- Network Hospitals: With 10,000+ network hospitals spread across metros and smaller cities, you're more likely to find a hospital when you need one.

Top IndusInd Health Insurance Plans

Note: This is not an exhaustive list of plans. For complete details, visit the official website.

Key Features of IndusInd Health Insurance Plans

Health Gain

- Large Family Floater: Cover up to 12 family members under a single policy. Combined with a sum insured of up to ₹5 crore and up to 40% family discount, it's well-suited for those planning long-term coverage for a large household.

- No Room Rent Capping: No restrictions on room type, so you won't find your entire hospital bill inflated just because you chose a private room.

- Restoration: The sum insured is restored once exhausted for both related and unrelated illnesses. The default restoration is limited; unlimited restoration requires an add-on.

- Pre- and Post-Hospitalization: Covers 60 days pre- and 90 days post-hospitalization by default. An add-on upgrades this to 90/180 days, comparable to the more generous plans in the market.

- Add-On Flexibility: You can layer on OPD cover, consumables, air ambulance, home care, PED waiting period reduction (from 3 years to 1 year), guaranteed cumulative bonus, and more. This makes the plan highly customizable, but each add-on increases the premium, so the base plan is fairly lean on built-in benefits.

Health Infinity

- No Restrictions Plan: Coverage up to ₹5 crore, with no room rent cap and disease-wise sub-limits.

- Bonus: The optional Super Charger add-on boosts your sum insured by 20% or 33.33% at each renewal, up to a maximum 100% increase.

- Pre- and Post-Hospitalization: Covers 90 days pre- and 180 days post-hospitalization, which is among the more generous in its category.

- Maternity Cover: Available via the Mother & Child Care add-on, with a waiting period that can be reduced to 1 year.

- Add-On Flexibility: Similar to Health Gain, a wide range of add-ons is available. However, buyers looking for a plan with comprehensive built-in benefits, unlimited restoration, cumulative bonus, and the like, may find that other plans in this segment offer more out of the box.

Health Global

- Overseas Treatment: Covers up to $1 million for both planned and emergency treatment abroad, including the US and Canada. This is among the more comprehensive global health offerings available from Indian insurers.

- India + Global Option: The India + Global variant gives you a separate India sum insured alongside your global cover under the same policy, so you're not drawing from the same pool for domestic and international claims.

- Travel Add-On: A Multi-trip rider adds coverage for trip cancellations, baggage loss, and passport loss, making it a reasonable all-in-one option for frequent international travelers.

Now that we have seen the key features of the plans, let’s have a look at the premiums for the Health Gain Power and Health Infinity plans.

Premium Comparison

Note: A stands for adults, and C stands for child. The premiums are calculated for healthy individuals living in Delhi (pincode: 110010) for a ₹15 lakh cover. These are illustrative premiums, and the final premium can vary based on channel discounts, opted add-ons, and insurer underwriting.

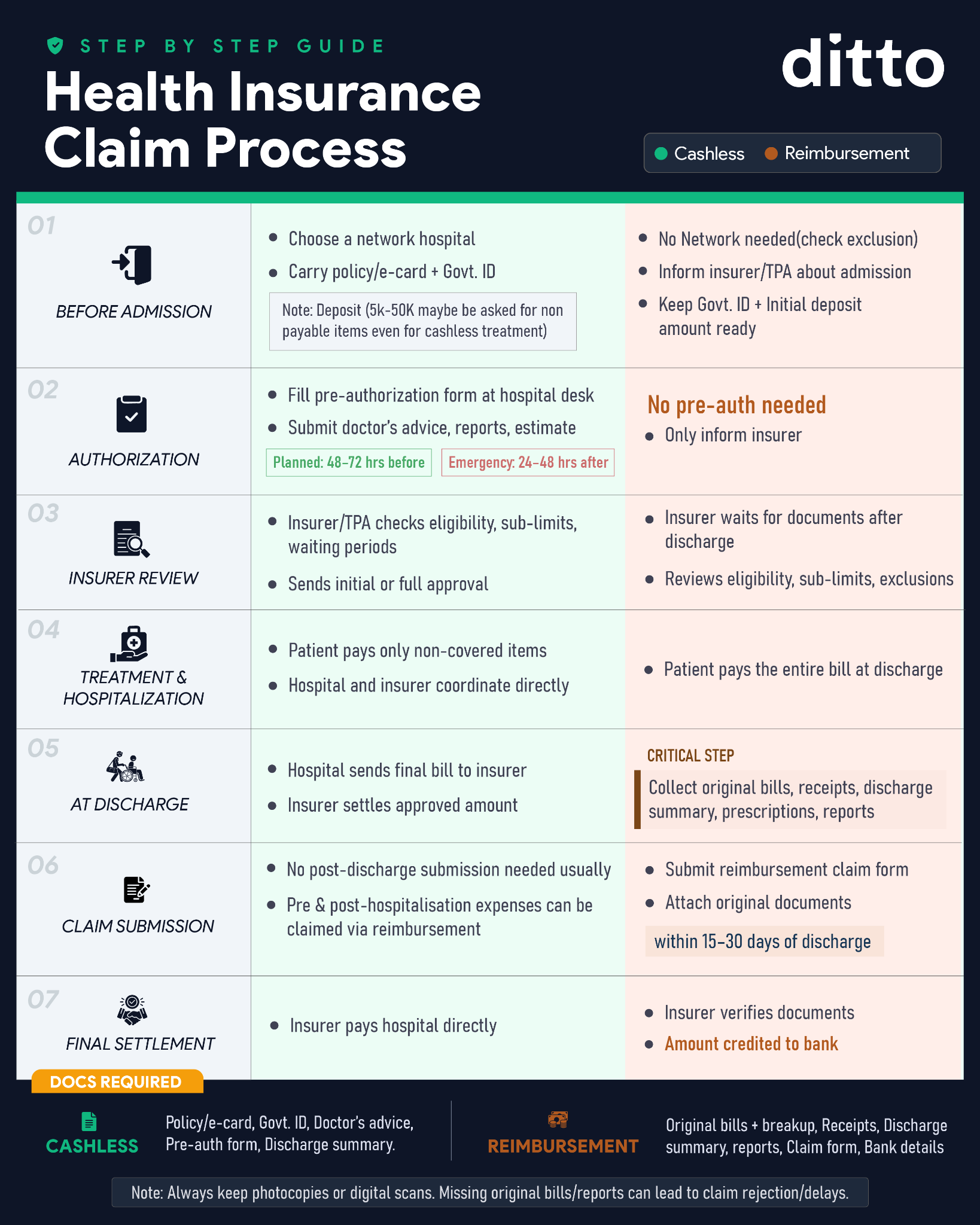

IndusInd Claim Process

The claim process for IndusInd is the same as that of other health insurers. To understand the cashless as well as reimbursement claim processing, refer to the infographic below:

IndusInd Contact Details and Address

- Helpline Number: +91 22 48903009

- Senior-Citizen Helpline Number: 022-65934185

- Email: services@indusindinsurance.com

- WhatsApp Number: 7400422200

- Website: https://www.indusindinsurance.com/

- Address: IndusInd General Insurance (formerly known as Reliance General Insurance), Correspondence Unit, 2nd & 3rd Floor, Winway Building, 11/12, Block No-4, Old No-67, South Tukoganj, Near Madhumilan Square, Indore, Madhya Pradesh, India - 452001

Ditto’s Pick for the Top 10 Health Insurance Companies in India

IndusInd is not on our list of the top 10 health insurance companies in India owing to the recent brand restructuring and plan features. We evaluate insurers across multiple parameters, including CSR, incurred claim ratio (ICR), business volume, number of complaints per 10,000 policies, hospital network size, product quality, and financial stability.

Note: If you'd like to explore the detailed figures reported by insurers and the IRDAI in their annual disclosures and public reports, visit Ditto Data Labs, our proprietary repository of health insurance data, meticulously compiled, verified, and maintained by the Ditto team over the years.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 22,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Ditto’s Verdict on IndusInd Health Insurance

IndusInd General Insurance is a financially stable insurer with decent competitive features. But their claim-settlement track record is where they fall short of earning what we'd consider a confident recommendation. For a product you're buying for peace of mind during a medical crisis, that matters a lot.

We do not actively recommend IndusInd as a first choice for most buyers. Their plans offer a high degree of customization through add-ons, but building a well-rounded policy this way can push premiums up considerably. If you're looking for comprehensive coverage with strong built-in benefits like unlimited restoration and cumulative bonuses, insurers like HDFC ERGO and Care Health deliver these by default, with stronger claim-settlement records and better overall value. For more alternatives, refer to our guide to the best health insurance companies in India.

Frequently Asked Questions

Last updated on: