Overview

India’s life insurance market is growing, and the latest numbers are proof. According to the IRDAI Report 2024-25, the average premium per person, or insurance density, rose to USD 97 in FY 2025 from USD 95 in FY 2024. Life insurance density also increased, reaching USD 72, up from USD 70 the previous year.

Amid this expanding market, term insurance stands out as a simple, cost-effective way to ensure your family’s financial security. It is the simplest form of life insurance: you pay a fixed premium for a fixed period, and if you pass away during the policy term, your nominee receives the sum assured. Let’s discuss the features of term insurance, its types, premium comparison, and other details.

Best Term Insurance Plans in India (2026)

For more details on the comprehensive features, refer to our guide on the best term insurance plan in India.

Talk to an expert

today and

find

the right

insurance for you.

What is Term Insurance?

Term insurance provides financial protection to your family if you pass away during the policy term. It ensures that your dependents can maintain their lifestyle, pay off debts, cover living expenses, and meet future goals such as education or retirement without being financially burdened.

How Term Life Insurance Works?

- You pick your sum assured (SA), policy term, and premium payment option.

- The insurer evaluates your overall profile based on its underwriting guidelines and then decides whether to issue the policy or not.

- Once your term policy is issued, you keep paying premiums to maintain the policy.

- If you pass away during the term, your nominee receives the death benefit.

- If you survive the term, the policy ends without any payout unless you opted for a return of premium version.

Types of Term Insurance

The infographic below can help you understand the different types of term insurance in detail.

Key Insights:

- We recommend level term insurance as the default option because it provides a fixed, life cover at an affordable premium throughout the policy term.

- Increasing cover, zero cost exit, and housewife term plans can be considered only when they fit a specific need or profile.

- We don’t recommend return of premium, decreasing term insurance, or whole life term insurance because they either cost much more, reduce coverage over time, or extend coverage beyond the years when your family actually depends on your income.

- Group term and joint term insurance should not be your primary protection plan because employer- or bank-linked covers can end at any time, and joint covers may have payout and rider limitations. Separate individual term plans usually offer cleaner and more reliable protection.

Eligibility Criteria and Key Parameters

Note: Features and eligibility may vary from plan to plan.

Term Insurance Riders: Adding Extra Cover to Your Policy

Riders are optional add-ons that enhance your base term plan. You pay an additional premium for each rider you add. Not all riders are equally useful, so choose only what your situation actually calls for.

Take a look at the below infographic to understand the popular term insurance riders you can opt for or avoid based on your needs:

For more details, refer to our guide on what are riders or add-ons in term insurance.

How Much Term Insurance Cover Do You Actually Need?

At Ditto, we recommend an expense and liability based approach. Your cover should be enough to help your family maintain their lifestyle, repay outstanding loans, and fund major future goals like children’s education, even if you are not around.

The easiest way to estimate this is through our term insurance calculator. Enter your age, the number of years your family needs protection, monthly expenses, outstanding loans, and any existing life insurance cover. The calculator will give you a more practical estimate based on your actual responsibilities, not just your income.

Note: If you opt for higher coverage, insurers conduct stricter financial and medical underwriting. At Ditto, we recommend not skipping any test. Even if your policy application is declined, early clarity helps you plan and avoid future claim complications.

If you already have an existing life insurance cover, you should deduct the death sum assured from the recommended coverage. You should also declare it while purchasing a new term plan. This helps ensure you’re adequately insured without over-insuring or paying unnecessary excess premiums.

For more information, read our guide on how much term insurance do I need.

How to Decide the Right Term Insurance Plan for You?

Choosing term life insurance involves selecting a financially reliable insurer and a policy that aligns with your income, dependents, loans, and long-term family goals.

At Ditto, we rate plans using publicly disclosed metrics like Claim Settlement Ratio (CSR), Amount Settlement Ratio (ASR), solvency ratio, complaint volume, and premium affordability. Based on these checks, Axis Max Life is a strong pick, with a 99.62% average Claim Settlement Ratio (CSR) and 96.37% Amount Settlement Ratio (ASR) across FY 2022-25.

For more details, read how to choose term insurance.

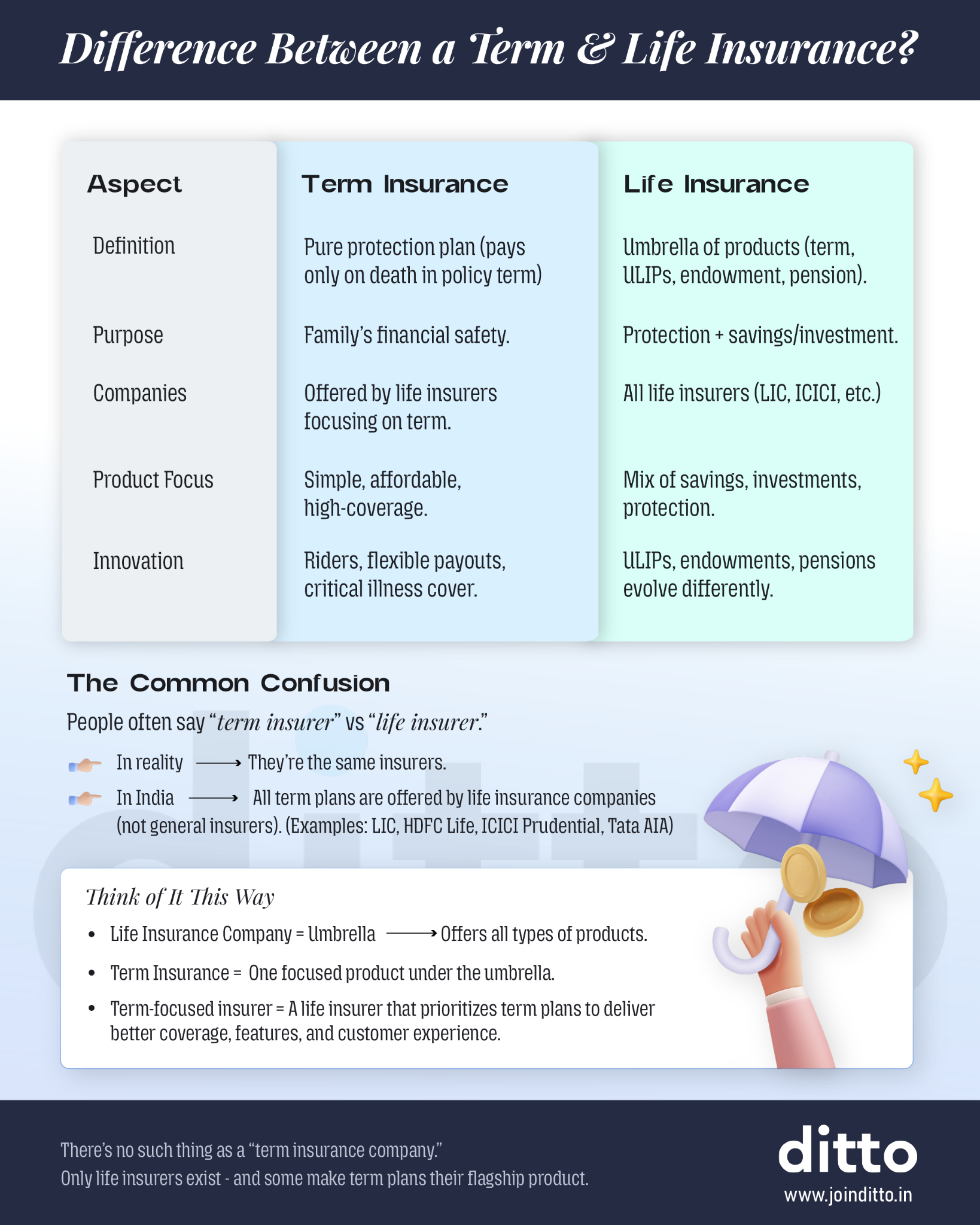

Term Insurance vs. Life Insurance: What's the Difference?

Term life insurance is a type of pure-protection life insurance that provides a death benefit if the policyholder passes away during the policy term. Conversely, life insurance is a broader category that includes policies that combine savings or market-linked investment with insurance and can provide a payout at maturity if you survive.

Refer to the infographic below to learn more about the differences between term insurance and life insurance.

How Much Does Term Insurance Cost?

Term insurance premiums depend primarily on your age, gender, smoking status, health profile, coverage amount, and policy term. The earlier you buy, the lower your premium, and that rate stays locked for the full policy term.

Here is an indicative premium comparison for non-smoking individual profiles (pin code: 110001) seeking ₹2 crore cover until age 65:

Note: These premiums are estimated without first-year discounts.

How to Buy Term Insurance Through Ditto: Step-by-Step

Understand Your Policy

Share Basic Details

Choose Cover and Payment

Apply and Get Issued

Note: When you buy term insurance through Ditto, you pay no extra charges, and the premium remains the same as what you would pay on the insurer’s website.

Did You Know?

Tax Benefits of Term Insurance

There are three major term insurance tax benefits in India:

- Tax deductions up to ₹1.5 lakh on premiums paid under Section 80C (old tax regime).

- Tax-free payouts to nominees under Section 10(10D), regardless of regimes.

- Tax deductions on premiums paid under certain riders, like critical illness, within the Section 80D limits (old regime).

For more details, refer to our guide on term insurance tax benefits in India.

Quick Update

How to File a Term Insurance Claim?

- The nominee should first inform the insurer as soon as possible through the insurer’s website, branch, email, or helpline.

- They must submit the claim form along with key documents, including the death certificate, policy documents, the nominee’s KYC, bank details, and medical or police records, if applicable.

- The insurer will verify the documents and may request additional information in the event of an accidental, premature, or suspicious death.

- Once the claim is approved, the insurer pays the death benefit to the nominee’s registered bank account.

For more details, refer to our term insurance claim guide.

How Long Does a Term Insurance Claim Take to Settle?

According to IRDAI’s 2024 policyholder protection framework, life insurers must settle or reject a death claim within 15 days of receiving all required claim documents and clarifications, if no investigation is needed. If an investigation is required, it must be completed within 45 days of claim submission. Any delay beyond these timelines attracts interest at the bank rate plus 2%, payable along with the claim amount.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Verdict on Term Insurance

At Ditto, we recommend pure term insurance to protect your family. It offers a high life cover at a relatively low premium. Much like motor, home, or fire insurance, term insurance is an expense you hope never needs to be used, but one that brings immense peace of mind. It ensures your loved ones remain financially secure even if life takes an unexpected turn.

If you are looking for a term plan from insurers with established track records and affordable riders, we recommend checking the best term insurance companies, which align with your long-term goals.

Frequently Asked Questions

Customer Reviews

Last updated on: