A general rule of thumb for term insurance is to have coverage equal to 10 to 15 times your annual income. At Ditto, we recommend it as a starting base, adjusted for outstanding loans, future goals, and existing personal insurance cover. We evaluate coverage needs using a needs-based calculation because households' financial obligations differ.

For context, a 30-year-old in Delhi earning ₹10 lakh pays ₹12,296 per year for a ₹1 crore term cover under Axis Max Life Smart Term Plan Plus. Meanwhile, a 30-year-old earning ₹15 lakh a year in the same location may need closer to ₹2 crore if they have a home loan, young children, or dependent parents.

This guide is for anyone who’s wondering, “How much term insurance do I need based on my needs?”

Most Indians end up under-insuring themselves, either by picking a random number like ₹1 crore or by depending on outdated rules of thumb. When inflation pushes monthly expenses from ₹40,000 to nearly ₹1 lakh over 15 to 20 years, even a “big” cover can fall short.

At Ditto, our advisors speak to numerous customers every month about choosing the right term plan, and a recurring problem we see is people miscalculating the ideal sum assured.

In this guide, we will help you understand the actual term coverage you need using proven, industry-accepted methods.

Why Choosing the Right Term Insurance Cover Matters

01

Protects Your Family’s Lifestyle

The right term cover ensures your family can continue meeting everyday expenses even if you are no longer around. This includes rent, groceries, school fees, EMIs, and healthcare costs.

02

Helps Clear Loans and Liabilities

If you have a home loan, car loan, or personal loan, the cover should be large enough to repay these debts. This prevents your family from carrying the burden of EMIs later.

03

Accounts for Future Goals

Your term cover should include future expenses such as children’s education, marriage, or care for dependent parents. These goals can be expensive, so they should not be ignored while calculating cover.

04

Protects Against Inflation

Inflation reduces the value of money over time. A well-calculated cover ensures your family’s future expenses are accounted for, not just today’s costs.

05

Gives Peace of Mind

When the cover amount is right, you know your family has a strong financial safety net. This makes term insurance more useful than simply buying a random cover amount like ₹50 lakh or ₹1 crore.

CTA

Methods to Calculate How Much Term Insurance You Need

Income-Based Method (HLV + Income Replacement)

This method combines the logic of Human Life Value (HLV) and Income Replacement to calculate term insurance coverage.

Formula: Annual income × number of working years left

Example: If you earn ₹10 lakh annually and plan to work for the next 30 years,

₹10 lakh × 30 = ₹3 crore term insurance coverage

Benefit: If you’re the sole or primary earner in the family, calculating coverage through this method ensures your family continues to live comfortably, even in your absence.

Drawback: This method doesn’t account for increments, job changes, or even starting your own business. Moreover, insurers may limit it to 25x your annual income due to underwriting rules.

Expense and Liabilities Replacement Method

This method adds up all future financial needs, such as monthly expenses, children’s education, marriage, your spouse’s retirement (adjusted for inflation), and other outstanding liabilities, such as home, education, or personal loans.

Formula: Total future expenses + Outstanding liabilities = Cover required

Benefit: This method ensures you're neither under- nor over-insured since it's based on your actual life goals.

At Ditto, we use the expense and liabilities replacement method to estimate the term cover you require. To get a better understanding, use our term insurance calculator or talk to our certified experts to precisely know the ideal cover for you.

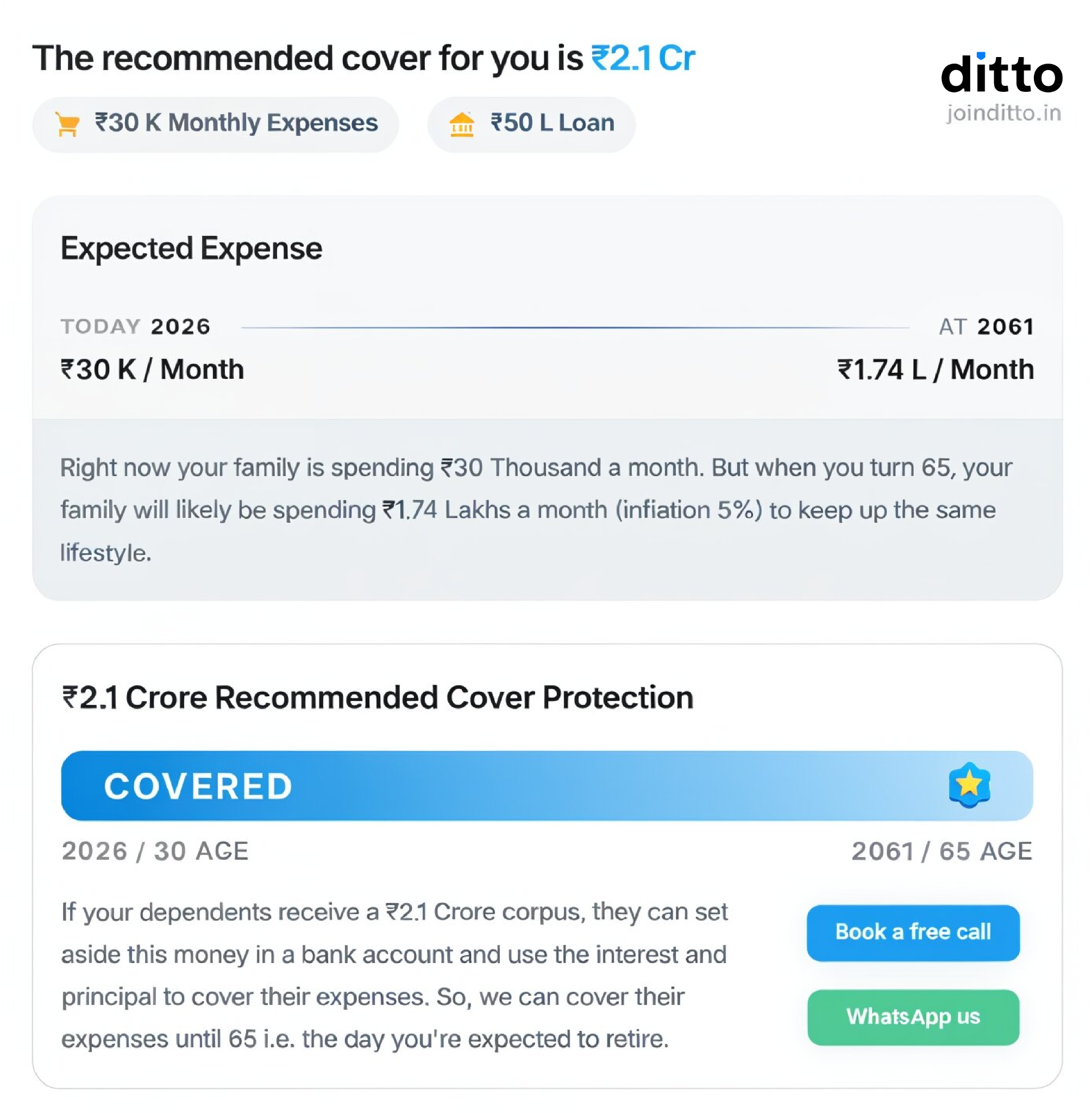

The following snippet includes the term insurance coverage calculation for a 30-year-old individual with ₹30,000 monthly expenses and a ₹50 lakh home loan, seeking coverage up to 65 years.

Underwriter’s Rule

It’s a general thumb rule based on insurers’ internal underwriting and risk management policies. It usually suggests a maximum cover of around 10 to 25 times your annual income.

Example:

If you earn ₹10 lakh a year, the term cover should be somewhere between ₹1 crore and ₹2.5 crore.

If you’re younger and have more financial goals ahead, aim for the higher end (20x to 25x).

If you are older and already have wealth or fewer responsibilities, the lower end may suffice (10x to 20x).

Benefit: While it’s not foolproof, the underwriter’s rule gives you a quick estimate when you're short on time or just starting your planning journey. In most cases, it is prudent to take the maximum coverage the insurer offers based on this rule and lock in the premium early. However, make sure you declare all existing personal life insurance policies and exclude their sum assured while calculating the additional cover you need.

There may also be cases where the cover you actually need is higher than what your current income allows you to buy. In such situations, opt for the maximum cover you are eligible for today and reassess your coverage as your income increases.

Key Factors That Affect Your Term Insurance Coverage Amount

Number of Dependents: A single earner supporting a spouse, two children, and aging parents needs significantly more coverage than someone with no dependents. Each dependent adds to both the income-replacement and the expenses component of your calculation.

Outstanding Loans: Every rupee of outstanding unsecured debt is a liability your family inherits. Your home loan balance in particular should be added directly to your coverage requirement, since a lapsed EMI can put the burden over your family at risk.

Existing Life Cover: If your employer provides group term insurance, it counts, but do not rely on it entirely. Group cover lapses when you change jobs and typically offers 2 to 5 times your salary, well below what most families need.

Inflation: Your term cover should be reviewed regularly as your income, liabilities, and family responsibilities change. Buying term insurance once is not enough. Major life events may require increasing your cover to keep your family adequately protected.

Age, Education, and Health: Insurers have underwriting limits on coverage multiples based on your age, education, and income. Younger, healthier applicants and graduates typically get access to higher multiples, which is another reason to buy early and buy enough the first time.

Did You Know?

A higher term insurance cover does not always lead to proportionally higher premiums. For instance, increasing your coverage from ₹1 crore to ₹2 crore may result in only an 80% proportional increase in the premium due to bulk pricing discounts.

Common Mistakes to Avoid When Deciding Your Term Cover

Choosing Too Little Coverage

Many people assume ₹50 lakh to ₹1 crore is enough, but this amount may run out quickly once you factor in monthly expenses, loans, education, healthcare, and inflation. A better approach is to calculate coverage based on your family’s actual needs rather than a random number.

Relying Only on Thumb Rules

The 10 to 15 times annual income rule can be a useful starting point, but it may not work for everyone. Your ideal cover should also include liabilities, dependents, future goals, and existing savings.

Counting Group Insurance as the Primary Cover

Group cover is a bonus, not a plan. If you switch jobs or get laid off, that cover disappears. Your personal term plan is the only guaranteed safety net.

Choosing a Short Policy Term

Your policy should run until your youngest dependent is financially independent and your longest loan is repaid, or until age 65 to 70 at a minimum. A 20-year policy bought at 30 expires at 50, when you may still have a home loan and children in college.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Before you lock in your term insurance cover, there are a few personal factors that deserve a closer look.

If you’re in your 20s or early 30s, you can choose a longer tenure and get higher coverage at a lower premium.

Your coverage should increase with the total number of people relying on your income, such as your spouse, young children, or aging parents.

Consider whether your income is stable or likely to grow, and choose slightly higher coverage now to stay future-ready.

If you are planning to borrow soon (e.g., via loans and liabilities), make a provision for it in your term cover early.

Health conditions, smoking, or family illness history can raise premiums or affect eligibility, so getting a policy early and maintaining a healthy lifestyle helps you lock in better rates.

Various methods suggest an ideal cover range of ₹1 crore to ₹2.5 crore, balancing affordability with long-term financial protection. While this may sound sufficient, many families could still fall short over time. Instead of relying on guesswork, use methods like HLV, the Underwriter’s Rule, or the Expense Replacement Method to estimate the right cover, ideally with guidance from a trusted advisor.

Frequently Asked Questions

What is Term Insurance?

Term insurance provides financial protection to your family if you pass away during the policy term. It ensures that your dependents can maintain their lifestyle, pay off debts, cover living expenses, and meet future goals like education or retirement, without being burdened financially.Additional riders such as critical illness, accidental total and permanent disability, and waiver of premium also provide enhanced protection beyond the base death cover. In short, term insurance acts as an income replacement tool, making sure your family has a financial safety net even in your absence.

How much term insurance do I need?

There’s no one-size-fits-all number. The term insurance coverage that you need depends on your income, expenses, goals, and other financial obligations. Usually, you can determine the sum assured using three proven methods: the income-based method (human life value + income replacement), the expense and liabilities replacement method, and the underwriter's rule. At Ditto, we follow the expense and liabilities replacement method to help you decide your term cover. Alternatively, you can also use our term cover calculator and check for the premium estimates.

What are the factors to keep in mind when calculating a term insurance cover?

Account for monthly expenses and inflation so your cover reflects rising living costs and dependent needs. Add existing loans and consider future liabilities to avoid leaving unpaid debt behind. Include future goals like children’s education, weddings, and spouse’s retirement by estimating their inflated cost. Set aside part of your cover to ensure your spouse has long-term financial stability even after the children are independent. Subtract only existing life insurance covers from your maximum eligible amount and declare them when applying for a new policy.

Does a higher term insurance cover always mean a proportionately higher premium?

No, a higher term insurance cover doesn’t always lead to proportionately higher premiums for policyholders. Insurers do not increase premiums linearly just because you seek higher coverage. For example, if you opt for a ₹1 crore cover with the Axis Max Life Smart Term Plan Plus as a 30-year-old (up to 65 years), it will cost you ₹12,296 annually. Conversely, a ₹2 crore cover will cost you only ₹20,656. Put simply, double the cover does not mean double the premium.

How does term insurance coverage work?

Term insurance coverage is always based on the sum assured you choose, but the maximum limit depends on factors like your age, education, occupation type, and income. For instance, if your highest education is below graduation or you are above 35, the eligible coverage multiplier is reduced. For self-employed individuals or those without traditional income proof, insurers like ICICI Prudential iProtect Super and the Bajaj Life iSecure II use surrogate indicators such as credit scores, credit card limits, or investment proofs.

How to enhance my basic term insurance cover?

Riders can play a significant role in turning the best term insurance plan into a complete protection shield. The top 3 riders worth considering are critical illness cover, Accidental total and permanent disability (ATPD), and waiver of premium. You can always use a term cover calculator to estimate your premiums and decide whether or not to add the riders based on your current needs. If you are still worried about miscalculations or confused about the correct sum assured, the best thing to do is to approach an IRDAI-certified advisor for further assistance.

Does age impact term insurance coverage?

When you are young, you can get higher coverage at lower premiums that stay fixed throughout the policy term. As you approach your 30s or 40s, major life events like marriage or having a child increase your financial responsibilities, so buying a higher cover early is always recommended. As you age, the chances of lifestyle diseases like diabetes, hypertension, obesity, or heart-related issues also increase. Hence, insurers charge a higher premium, add cover or rider restrictions, seek additional medical tests, or reject the proposal in some cases. That is why buying adequate cover early, while you are young and healthy, is the smarter move.

Is ₹1 crore term insurance enough?

Not always. A ₹1 crore term cover may look large today, but it may fall short if you have high monthly expenses, loans, children’s education goals, or long-term dependents. Instead of choosing a round number, calculate your cover based on your family’s actual expenses, liabilities, future goals, inflation, and existing life insurance cover. You must also analyze several factors when considering the insurer of your choice for the cover that you sought. For more information, refer to our guide on the best term plan for ₹1 crore.

Can I increase my term insurance cover later?

Yes, but it depends on the insurer and the plan features. Some term plans offer life stage benefits, where you can increase your cover after major milestones like marriage, childbirth, or taking a home loan. However, increasing cover later may involve fresh underwriting, higher premiums, or medical checks, so it is better to buy adequate cover early. You can also consider buying a second term plan later if your existing plan does not allow a cover increase. But remember, the new policy will be priced based on your age, health, income, and underwriting eligibility at that time.

Should I subtract my existing investments while calculating term insurance cover?

At Ditto, we do not recommend subtracting your current assets or investments from your required term insurance cover. Your investments are meant for wealth creation, and dipping into them prematurely breaks the power of compounding. Think of term insurance as your money of last resort, and it is there to provide absolute security to your loved ones in your absence. Consider your existing assets as a financial bonus, allowing you to maintain a safe, conservative approach to protecting your family's future.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.