ICICI Pru Platinum is a Unit Linked Insurance Plan (ULIP) from ICICI Prudential Life Insurance that combines market-linked investing with life insurance protection. The plan requires a minimum premium of ₹60,000 and comes with a mandatory 5-year lock-in period. ICICI Pru Platinum plan offers access to 31 investment funds and 4 portfolio strategies.

Policyholders also get unlimited free fund switches and withdrawal flexibility after the lock-in period. Two life cover variants are available: Growth Plus for wealth creation and Protect Plus.

However, at Ditto, we do not recommend plans that mix investments and life coverage, and they tend to be less efficient than buying a term plan and investing separately. This guide is for those who wish to explore whether ICICI Pru Platinum is the correct choice.

Want to build long-term wealth without giving up life insurance protection? ICICI Pru Platinum combines market-linked investment opportunities with life cover in a single plan. In the next few minutes, this ICICI Pru Platinum plan review will break down the policy features, benefits and drawbacks.

Designed for wealth creation, this option pays the higher of the sum assured or fund value on death. Since the protection component is lower, mortality charges stay relatively low, allowing a large portion of the premium to remain invested.

02

Protect Plus Variant

Designed for stronger financial protection, this option pays both the sum assured and the accumulated fund value on death. Since the insurance cover is higher, mortality charges are also high, which reduces the portion of the premium available for investment. However, both variants pay only the fund value at maturity.

03

No Premium Allocation Charge

ICICI Pru Platinum does not deduct any premium allocation charge from your investment amount. Your premium goes directly into the chosen funds from day one.

04

Systematic Withdrawal Facility

After completing five policy years, you can start regular withdrawals from the fund value through the Systematic Withdrawal Plan. You can choose either a fixed amount or a fixed percentage based on your future income needs.

05

Top-Up Investment Option

The plan allows you to invest additional money through top-up during the policy term with a minimum premium of ₹500. However, top-ups are not allowed during the final five years before maturity and are not available for single pay policies.

06

Partial Withdrawal Benefit

Partial withdrawals are allowed only after the five-year lock-in period and after payment of five full years’ premiums. In one policy year, total withdrawals cannot exceed 20% of the available fund value. The minimum amount for each withdrawal is ₹2000.

07

Flexible Maturity Payouts

At maturity, you can either take the entire fund value as a lump sum or choose staggered payouts over up to five years. This helps create a more structured withdrawal strategy.

08

No Loan Facility

The policy does not offer a loan facility against the accumulated fund value.

Note: ICICI Pru Platinum does not offer death benefit payout choices like monthly income or lump sum plus income. The death claim payout is a lump sum.

Eligibility Criteria

Feature

Details

Entry Age

0 years to 60 years

Maturity Age

18 years to 75 years

Policy Term

60 years to 75 years minus age at entry

Premium Payment Term

Limeted pay (5 years to 30 years) and single pay

Premium Payment Frequency

Annual, half-yearly, and monthly

Minimum Premium (Yearly PremiumPayment Mode)

₹60,000

Minimum Premium for Single Pay(Yearly PremiumPayment Mode)

₹2.50 lakhs

Minimum Premium(Half-Yearly and Monthly Premium Payment Mode)

₹72,000

Note: The above eligibility criteria vary with the variant and policy term you choose. Additionally, the life insurance component is relatively limited. The sum assured on death ranges from 1.1x to 10x the annual premium, depending on age, premium type, and variant. Even at the maximum end, the protection still falls short for families needing substantial long-term income replacement.

Benefits of the ICICI Pru Platinum Plan

Market-Linked Wealth Creation: The plan allows investment in equity and debt funds to pursue long-term growth potential. It may work well for retirement, child education, or long-term corpus-creation goals over 15 years.

Portfolio Flexibility: The plan offers multiple fund options, portfolio strategies, and unlimited free fund switches (under the fixed portfolio strategy). This helps investors rebalance their investments without an immediate tax impact within the policy.

Systematic Withdrawal Facility: After five years, policyholders can withdraw fixed amounts regularly for planned expenses like retirement income or education funding. However, excessive withdrawals can reduce the overall corpus over time.

Tax Benefits: Premiums paid qualify for tax deductions under Section 80C under the old tax regime, up to ₹1.5 lakhs. Maturity benefits may also qualify for tax exemption under Section 10(10D). ULIP tax benefits are subject to prevailing tax rules and policy conditions.

What Are the Portfolio Strategies Under This Plan?

1. Fixed Portfolio Strategy: Lets you choose and manage your own fund allocation with unlimited free switches. Best suited for investors comfortable with regularly reviewing and adjusting equity, debt, and balanced fund exposures.

2. Target Asset Allocation Strategy: Maintains a chosen equity-debt mix through automatic quarterly rebalancing. Suitable for passive investors who want disciplined allocation without manual tracking.

3. Trigger Portfolio Strategy 2: Rebalances investments in response to predefined market triggers. Useful during volatile markets, though it follows fixed rules rather than market forecasting.

4.Lifecycle Based Portfolio Strategy 2: Automatically shifts allocation from equity toward safer debt-oriented funds as age increases, helping reduce risk gradually over time.

To know more about the fund options and portfolio strategies, refer to pages 7 to 10 of the ICICI Pru Platinum brochure.

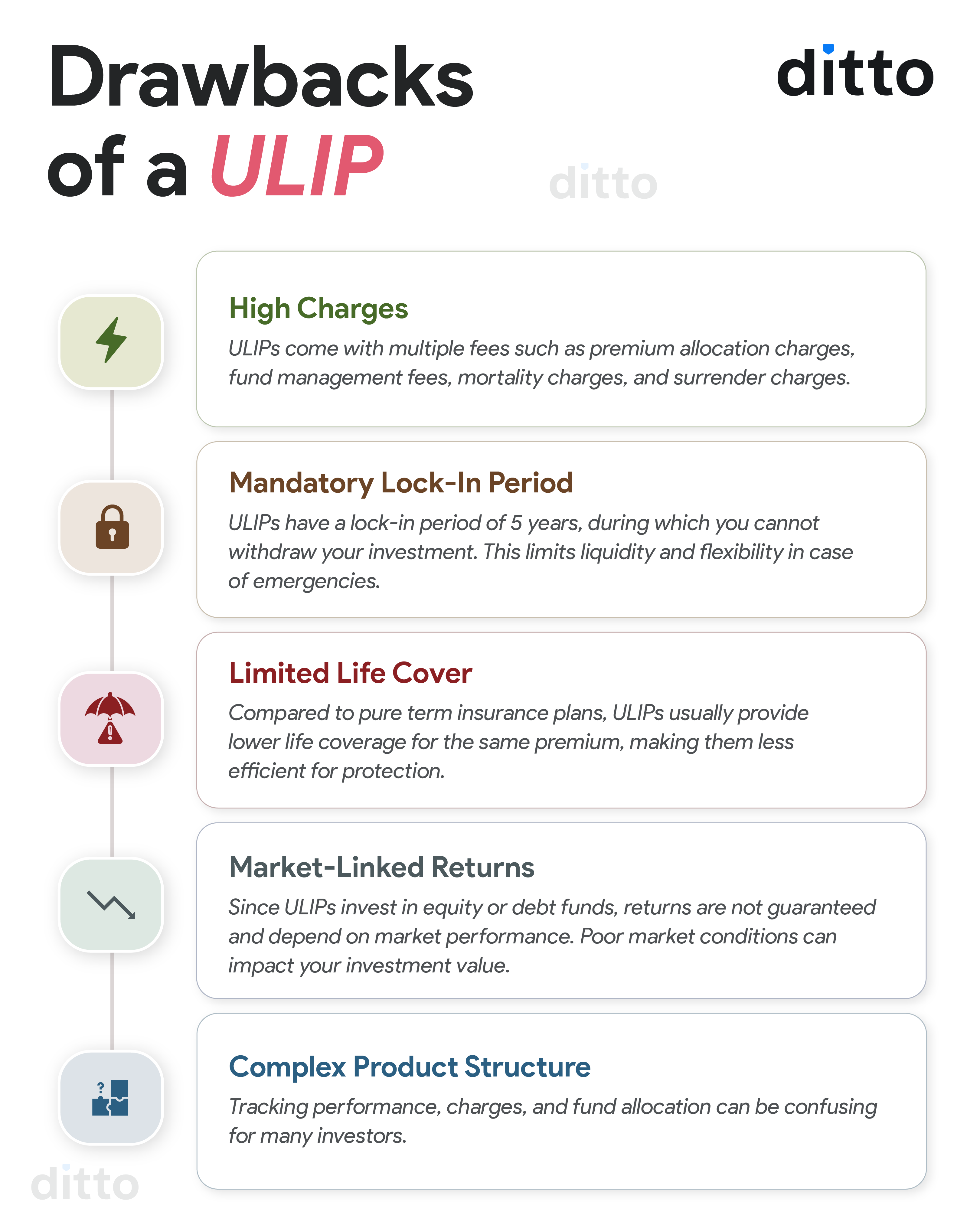

Drawbacks of the ICICI Pru Platinum Plan

While ICICI Pru Platinum does not deduct premium allocation charges, it does deduct other basic ULIP charges, such as fund management and mortality charges. Take a look at the infographic below to have an idea about the flaws of a standard ULIP.

Sample Premiums

Aspect

Figures

Total Premium

₹18 lakhs (₹15,000 per month for 10 years)

Premium Payment Term

10 years

Policy Term

40 years

Sum Assured

₹18 lakhs (10x annual premium)

Projected Value at 4% Gross Return

₹40.93 lakhs

Projected Value at 8% Gross Return

₹1.63 crore

Note: Projected values are illustrative for a 35-year-old with investments in the Growth Plus variant. The figures are based on assumptions from the ICICI Pru Platinum brochure, and actual returns are based on market performance.

As per IRDAI guidelines, insurers must show ULIP return illustrations at 4% and 8%. However, policy charges in the initial years reduce the amount actually invested. As a result, even if the underlying fund earns around 8%, the investor’s effective long-term return may be closer to around 6.4% after costs.

ULIP vs Term Insurance: Which Is Better?

From a pure financial protection standpoint, term insurance is usually the stronger and more cost-efficient option. A ULIP with an annual premium of ₹1.8 lakhs may provide life cover of only around ₹18 lakhs, which is inadequate for long-term family security.

In comparison, a standalone term insurance plan offers ₹2 crore or more in coverage at a much lower premium. For example,ICICI Prudential Life Insurance term plans like iProtect Smart Plus may offer this level of cover for roughly ₹74,088 annually (10-year premium payment term) for a healthy 35-year-old male. This is roughly 10x the coverage offered by a ULIP at 40% of the ULIP premium.

Here’s the difference between the two.

Aspect

ULIP

Term Insurance

Nature

Insurance and investment are bundled into one product.

Pure life insurance with no investment component.

Purpose

Wealth creation with a life cover attached.

Financial protection for dependents in the event of the policyholder's death.

Life Cover

Low relative to the premium paid (7 to 20 times the annual premiums).

Coverage is high (20 to 30 times annual income).

Premium Utilization

Split between mortality charges, fund management fees, and other charges.

The entire premium goes toward securing the life cover. Rest can be invested in better, low-cost instruments.

Returns

Market-linked and depend on the funds chosen (equity, debt, or hybrid).

High due to multiple built-in charges, which reduces the effective corpus.

One of the most cost-efficient insurance products.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 22,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

ICICI Pru Platinum may suit long-term investors who are comfortable with market-linked ULIPs and want investment plus insurance within a single structure. It may also work for individuals who already have adequate term insurance and are looking for a disciplined, long-term investment approach with portfolio flexibility.

However, at Ditto, we do not recommend ULIPs because their layered charges and complex structure often reduce overall return efficiency. For most investors, a separate term insurance plan for protection combined with investments like low-cost mutual funds, Public Provident Fund (PPF), or fixed deposits is usually a simpler, more transparent, and cost-effective strategy.

ICICI Pru Platinum is a Unit Linked Insurance Plan from ICICI Prudential Life Insurance that combines market-linked investing with life insurance. The plan provides access to 31 investment funds across equity, debt, and balanced categories, as well as 4 portfolio strategies. It also offers unlimited free fund switches for portfolio flexibility. The plan comes with a mandatory 5-year lock-in period and minimum annual premiums starting from ₹60,000. Buyers can choose between Growth Plus and Protect Plus variants based on whether their focus is wealth creation, higher protection, or a mix of both goals.

What are the two variants of the ICICI Pru Platinum plan?

ICICI Pru Platinum offers two variants called Growth Plus and Protect Plus. Growth Plus suits investors who already have adequate term insurance and want a cleaner wealth-creation structure through market-linked investments. Under this option, the death benefit is generally the higher of the sum assured or fund value. Protect Plus is designed for buyers who want additional financial protection for nominees along with investment growth. It offers both life cover and fund value. This ensures the family gets immediate financial protection through life cover while also retaining the wealth accumulated through market-linked investments, providing a stronger overall financial safety net.

What are the charges in the ICICI Pru Platinum plan?

ICICI Pru Platinum does not charge any premium allocation fee, which means your premium goes directly into investment funds. However, other standard ULIP charges still apply. These include policy administration charges, mortality charges for life cover, and fund management charges, depending on the fund selected. For example, the fund management charges for the money market fund is 0.75% per annum, while for the rest of the other available funds, it is 1.35% per annum. If you wish to know the exact charges, refer to the ICICI Pru Platinum brochure.

How many fund options does the ICICI Pru Platinum plan offer?

ICICI Pru Platinum offers access to 31 investment funds across equity, debt, and balanced categories. The plan by ICICI Prudential Life Insurance also includes 4 portfolio strategies designed for different risk profiles and investment horizons. Investors can switch between available funds without a switching fee, with unlimited free fund switches. This gives policyholders flexibility to rebalance their investments as market conditions change. One advantage of switching within a ULIP is that it does not trigger immediate taxation within the policy.

What is the lock-in period for the ICICI Pru Platinum plan?

Like all ULIPs regulated by IRDAI, ICICI Pru Platinum comes with a mandatory 5-year lock-in period. During this period, withdrawals are not allowed. Partial withdrawals become available only after completion of five policy years and payment of five full annual premiums. In a single policy year, total withdrawals cannot exceed 20% of the available fund value. The minimum withdrawal amount is ₹2,000 per transaction. The plan also restricts top-up investments during the final five years before maturity. This structure makes the plan more suitable for disciplined long-term investing rather than short-term liquidity or emergency financial needs.

Can I do a systematic withdrawal from the ICICI Pru Platinum plan?

Yes, ICICI Pru Platinum offers a Systematic Withdrawal Plan facility after completion of the mandatory 5-year lock-in period. Through this feature, policyholders can withdraw either a fixed amount or a fixed percentage from the available fund value at regular intervals. This may help create planned cash flows for retirement income, child education expenses, or other long-term financial goals. However, investors should understand that these withdrawals come directly from their accumulated fund value and are not separate income generated by the policy. Excessive withdrawals, especially during weak market phases, can significantly reduce the long-term corpus available at maturity.

What are the projected returns of the ICICI Pru Platinum plan?

ICICI Pru Platinum provides return illustrations based on IRDAI guidelines at assumed gross returns of 4% and 8%. For example, an illustration in the brochure shows that a 35-year-old investing ₹1.8 lakhs annually for 10 years under a 40-year policy term may accumulate around ₹40.9 lakhs at 4% returns and approximately ₹1.63 crore at 8% returns. These figures are only projections and not guaranteed outcomes. Actual returns depend on market performance, chosen funds, and policy charges. Since ULIP charges reduce long-term compounding, the investor’s effective return is usually lower than the gross fund performance shown in illustrations.

What are the tax benefits of the ICICI Pru Platinum plan?

Premiums paid towards ICICI Pru Platinum qualify for tax deductions under Section 80C of the Income Tax Act under the old tax regime, subject to the annual limit of ₹1.5 lakhs and applicable conditions. Maturity proceeds also qualify for tax exemption under Section 10(10D), depending on prevailing tax laws and policy eligibility conditions. However, ULIPs issued after February 1, 2021, with annual premiums exceeding ₹2.5 lakhs are subject to tax on maturity proceeds. Since ULIP taxation rules can be complex depending on the premium amount and holding structure, consulting a qualified tax advisor before investing is always advisable.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.