A specific illness waiting period in health insurance is the time during which certain listed conditions are not covered. As per the Insurance Regulatory and Development Authority of India (IRDAI), this period can extend up to 36 months from the start of the policy, depending on the insurer.

It applies to slow-growing, non-emergency conditions such as cataracts, hernias, sinusitis, kidney stones, joint replacement, etc. Unlike the pre-existing disease (PED) waiting period, this applies uniformly to all policyholders, regardless of their medical history. For example, if you buy a policy and develop a cataract within a year, the insurer won’t cover surgery as the waiting period for that condition hasn’t been completed.

Once the waiting period is completed, the specified treatments are covered if the policy is continuously renewed. However, if such conditions arise due to an accident, insurers waive the waiting period and provide immediate coverage. This guide is for anyone looking to understand how the waiting period works and how it impacts their health insurance coverage.

Industry reports suggest that a significant share of claim denials, about 31%, are rejected because the treatment was taken before the waiting period was completed.

This makes waiting periods one of the most overlooked reasons for claim rejection. Specific illness waiting periods are often more confusing because they apply even if the policyholder does not have the condition at the time of purchase.

In this article, we break down how specific illness waiting periods work, the conditions covered under them, and how you can plan around them.

If you’re unsure how the specific illness waiting period applies to your policy, book a free call or WhatsApp us for personalized guidance.

What is a Specific Illness Waiting Period in Health Insurance?

A specific illness waiting period is the time after buying a policy when certain listed conditions or surgeries are not covered.

Insurers impose this waiting period to prevent misuse of insurance and reduce adverse selection. In simple terms, it discourages people from buying a policy only when they expect to undergo a medical procedure.

Typically, the duration of this waiting period ranges from 1 to 3 years, depending on the insurer. Many companies, such as HDFC Ergo, clearly list these specific illnesses in their policy documents. It helps buyers understand which conditions are not covered during the waiting period. It’s also important to renew health insurance policies on time, as any break can reset the waiting periods and delay coverage.

Types of Waiting Periods in Health Insurance Plans

Health insurance plans include mandatory waiting periods before certain benefits are available.

The infographic below shows the different types and how each one applies to your policy.

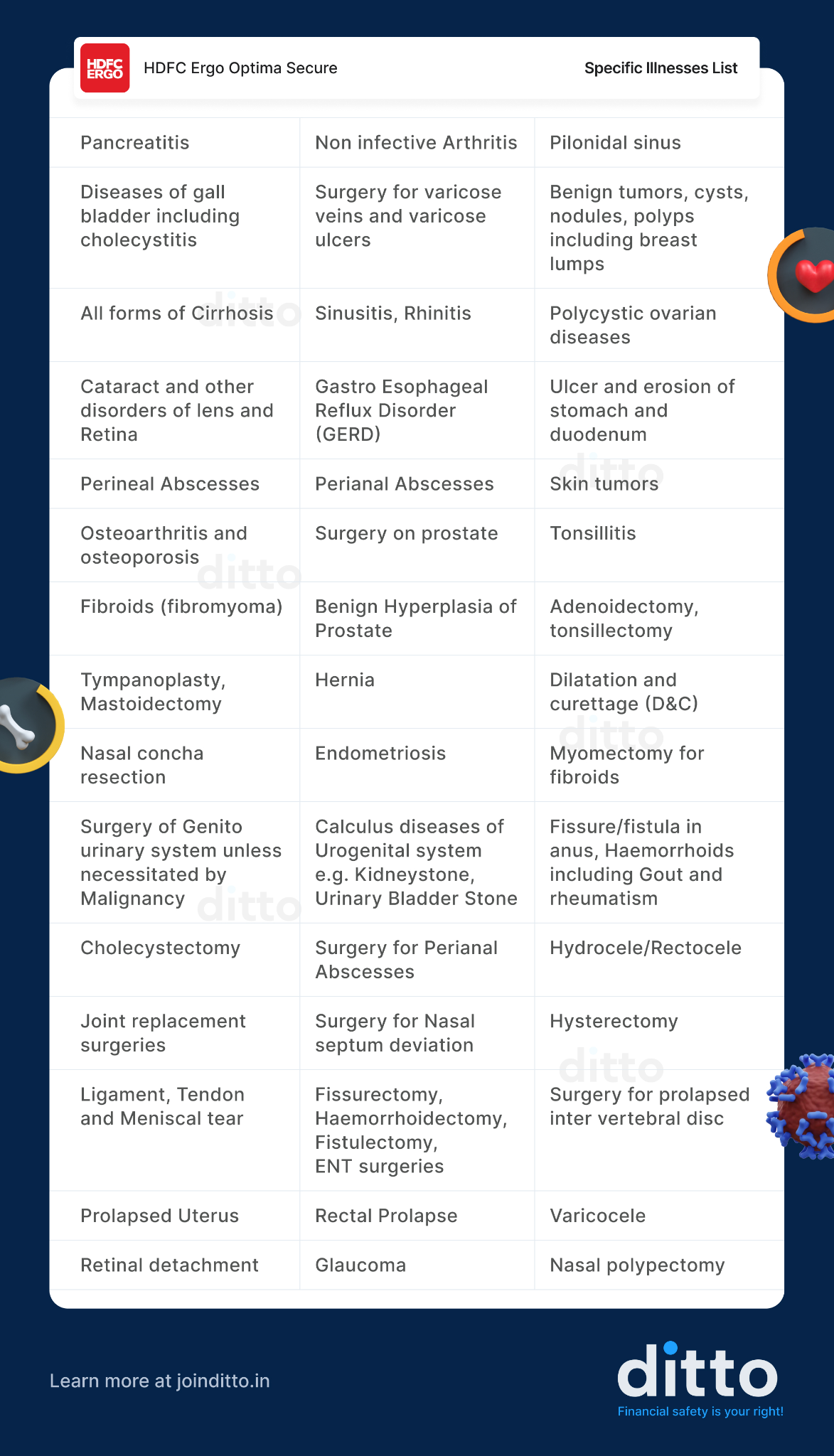

Common Illnesses with Specific Waiting Periods and Durations

Note: The exact list of conditions may vary across insurers and plan variants. It is best to carefully refer to the policy wording before purchasing. You can quickly locate these details by using a simple search (Ctrl + F) for “specific illnesses” or "specified diseases" in the policy wording.

How to Reduce or Avoid Waiting Periods in Health Insurance

Employer-Based Group Coverage: Group health insurance plans are one of the few ways to get coverage with little or no waiting time. Since the risk is spread across a large group, insurers often waive waiting periods for pre-existing diseases and, in some cases, the maternity waiting period in health insurance.

Waiting Period Reduction Add-ons: Many retail plans offer add-ons that reduce waiting periods for pre-existing conditions. These can shorten the duration significantly, sometimes to as little as 30 days for specified conditions. For example, HDFC Optima Secure (ABCD Chronic Care add-on) and Care Supreme (Instant Cover add-on) offer reduced waiting periods for conditions like diabetes, hypertension, asthma, and cholesterol. Some plans, like ICICI Lombard Elevate, offer add-ons that may reduce the waiting period for certain specific illnesses from two years to one year, subject to underwriting terms.

Early Enrollment Strategy: Buying health insurance early, while you are still healthy, ensures that all waiting periods are completed well in advance. This approach helps you stay prepared for future medical needs without facing delays in coverage when you need it most.

Cooling-Off Period vs Waiting Period in Health Insurance

A cooling-off period is often confused with a waiting period, but the two are quite different. Here’s how they differ:

Basis

Waiting Period

Cooling-Off Period

Definition

Time after policy purchase when certain claims are not covered

A gap required by insurers before issuing a new policy following a major illness or surgery.

Applicability

Applies after buying a policy

Applies before buying a policy

Official Term

Yes (defined in policy wording)

No (used informally by insurers/advisors)

Purpose

Prevent misuse and adverse selection

Assess health risk after recent illness/surgery

An Example of a Cooling-Off Period: If you recently had heart surgery, an insurer may ask you to wait 3–6 months before reviewing your application. This allows them to assess your recovery and ensure your health is stable before offering coverage. That’s why it’s important to disclose your recent medical history to understand if a cooling off period health insurance applies to your specific case.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

No-Spam and No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat with our advisors on WhatsApp.

Conclusion

A specific illness waiting period in health insurance protects insurers from short-term risks but requires patience from policyholders. Most retail plans impose a duration of one to three years for listed ailments, although employer-provided group health plans may offer immediate coverage for some of these treatments.

However, it is important not to rely solely on a group plan. Having a personal retail policy ensures more comprehensive and continuous coverage, especially if you change jobs or lose employer benefits. Buying insurance early while you are healthy also helps you complete waiting periods in advance. Review your policy documents carefully to understand which conditions are covered and when your benefits become fully available

Finally, continuous renewal is essential to ensure that waiting periods are completed and your coverage remains uninterrupted.

Frequently Asked Questions

What is the standard duration for specific illness waiting periods?

Most insurance companies in India commonly apply a specific illness waiting period of around 2 years for planned treatments and surgeries. However, as per IRDAI, this period can go up to 3 years, depending on the policy terms. This duration applies to common ailments like cataracts, hernias, arthritis, and stones. You must complete the waiting period before the insurer pays for these treatments. Some plans might reduce this to one year (e.g., ICICI Elevate), but a 2-year wait remains the industry standard. Always check the policy wording to see the exact list of excluded diseases or treatments for this period. Early purchase helps you complete this phase while you are still healthy and active.

What is the difference between specific disease waiting periods and pre-existing disease (PED) waiting periods?

Specific disease waiting periods apply to illnesses listed in the policy, such as cataract, hernia, kidney stones, and joint replacement. These conditions usually have a waiting period of 1 to 2 years, during which related claims are not payable. Pre-existing disease waiting periods apply to any condition diagnosed or treated before policy inception, with a maximum cap of 3 years, as mandated by IRDAI’s 2024 health insurance regulations. PED periods are condition-specific to the individual’s medical history, while specific disease waiting periods apply uniformly to all policyholders regardless of prior diagnosis. If a condition falls under both categories, the longer waiting period applies, which is usually the PED waiting period in most cases.

Does every policy have a 2 year waiting period list for health insurance?

Almost every comprehensive health plan includes a 2 year waiting period list for health insurance for specific ailments. This list usually contains slow-growing medical conditions that do not qualify as emergencies. Common examples include piles, fistulas, and gout. Insurers use this list to prevent people from buying a policy only when they discover a need for a scheduled surgery. You should review your insurer’s specific list carefully, as the conditions included can vary widely across policies. Understanding what is covered under this category helps you plan treatments in advance and avoid unexpected out-of-pocket expenses.

How are specific illnesses covered if I don’t have them when buying the policy but develop one soon after?

Even if you don’t have a listed condition at the time of purchase, the specific illness waiting period still applies. This means that if you develop any of these conditions soon after buying the policy, the insurer will not cover related treatment until the waiting period is completed. These waiting periods are standard and apply to all policyholders, regardless of health status at purchase. Once the specified duration is over and the policy is continuously renewed, coverage for these illnesses becomes available.

Is it possible to find zero waiting period health insurance for surgery?

Finding zero waiting period health insurance for surgery is difficult for retail buyers because insurers view this as a high risk. Surgeries due to accidents are an exception and are covered from day 1. For planned procedures like knee replacement or hernia surgery, you must complete the applicable waiting period, usually under the specific illness category. Some insurers offer add-ons such as waiting period reduction or PED waiver riders, which can shorten these timelines. True zero waiting period health insurance for all surgeries is typically available only through employer-provided group health insurance, where coverage can begin from day 1.

What is a cooling off period in health insurance?

A cooling off period in health insurance is the time an insurer waits before issuing a policy to someone who has just recovered from a major illness. For example, if you had a major surgery last month, the company might wait for a few months before they accept your application. This is different from a specific illness waiting period in health insurance, which starts after the policy is issued. The cooling-off period protects the insurer from immediate high-risk claims. Always disclose your recent medical history clearly to avoid any issues during the claim process.

Why do insurers mandate a specific illness waiting period in health insurance?

Insurers mandate a specific illness waiting period in health insurance to maintain a balanced risk pool. Without these rules, people would only purchase insurance when they need surgery. This would lead to massive losses for the insurance company and higher premiums for everyone else. By enforcing a two-year wait for non-emergency conditions, the insurer ensures that policyholders contribute to the pool over time. It encourages long-term health planning rather than short-term gain. Understanding this logic helps you see the value of maintaining continuous coverage without any breaks.

Can I reduce the initial waiting period in health insurance for my family?

The initial waiting period in health insurance is a standard 30-day window that applies to all new policies. During this time, claims for illnesses are not covered, except for accidents. In most retail plans, this waiting period cannot be reduced or removed. The ACKO Platinum health insurance plan is a rare option that lets you skip the usual 30-day waiting period (subject to underwriting approval). Additionally, employer-provided group health insurance plans may offer immediate coverage without this restriction for families.

Which conditions are on the 2-year waiting period list for health insurance?

The 2-year waiting period list usually includes planned or non-emergency conditions such as cataracts, hernias, kidney or gallbladder stones, sinusitis, tonsillitis, piles, fissures, fistulas, varicose veins, hydrocele, endometriosis, and joint-related issues like knee replacement. You can find the specific illness waiting period in the “waiting periods” or “exclusions” section of your policy wording. These are often listed under terms like “specified diseases” or “specified procedures,” depending on the insurer. If you require treatment for these conditions within the first two years, you will have to pay for it out of pocket.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.