Overview

India's medical inflation hit 13%-14% in 2025, nearly triple the general Consumer Price Index (CPI) rate. That number compounds every year. A treatment that costs ₹5 lakh today will cost roughly ₹8 lakh in 4 years. So what does that mean for your health cover?

Take government schemes as a starting point. Government health schemes like PM-JAY cap cover at ₹5 lakh per family per year. That's a meaningful safety net for low-income households. But for a middle-class family dealing with a serious illness at a top private hospital, it may run out fast.

This guide covers every major government health insurance scheme in India, what each one covers, who qualifies, and most importantly, whether you should rely on it alone.

Key Central Government Health Schemes

1) Ayushman Bharat PM-JAY

Ayushman Bharat PM-JAY is the world's largest government-funded national health insurance scheme. Launched in 2018, it provides ₹5 lakh per family per year for cashless secondary and tertiary hospitalization. It covers 1,900+ procedures as per set packages with empaneled public or private hospitals, along with associated expenses. Notably, there are no waiting periods under the plan.

The Ayushman Bharat health insurance scheme covers surgeries, ICU stays, diagnostics, and pre- and post-hospitalization expenses for listed procedures. The insured members can also link the PM-JAY benefit to their ABHA Card to store digital medical records and access services quickly.

The scheme is funded by a combination of central and state government funds.

Did You Know?

2) Central Government Health Scheme (CGHS)

CGHS covers serving and retired central government employees, Members of Parliament (MPs), and their dependents. It is more comprehensive than PM-JAY because it includes Outpatient Department (OPD) consultations, routine diagnostics, and medicines. Treatment is available at government dispensaries and empaneled private hospitals.

CGHS has an annual budget of ₹2,370 crore for 2025-26. So, if you are a central government employee, pensioner, or dependent, CGHS is one of the most comprehensive government schemes available.

3) Employees' State Insurance Scheme (ESIC)

ESIC covers organized-sector employees earning up to ₹21,000 per month (₹25,000 for persons with disabilities). Both employer and employee contribute to the scheme. It covers hospitalization, maternity, disability, and dependents' care in the event of a work-related death. The scheme now covers 668 districts across India.

Key Insight

4) Niramaya Health Insurance Scheme

Niramaya covers persons with Autism, Cerebral Palsy, Mental Retardation, or Multiple Disabilities. It provides up to ₹1 lakh per year on a reimbursement basis. Anyone holding a valid disability certificate and a Unique Disability ID (UDID) card is eligible, with no age limit and no pre-enrollment medical test.

Coverage includes hospitalization, OPD, physiotherapy, speech therapy, dental care, and transport costs. You can get treated at any hospital. The annual premium is ₹250 for Below Poverty Line (BPL) beneficiaries and ₹500 for others, and it does not increase with age. You can enroll through the National Trust or a registered disability organization.

5) Pradhan Mantri Surakshit Matritva Abhiyan (PMSMA)

PMSMA guarantees free antenatal care to all pregnant women in India. On the 9th of every month, any woman in her second or third trimester can visit a designated government health facility for a full checkup, including blood tests, an ultrasound, blood pressure monitoring, and nutritional counseling. The scheme is free of cost, and there is no income-based eligibility.

The simple goal is to catch high-risk pregnancies early and reduce maternal mortality.

One thing to keep in mind: PMSMA is not a health insurance scheme. It does not cover hospitalization costs. For actual maternity cover, you can consider your employer-provided policy or rely on savings.

Key State-Level Government Health Schemes

Most states run their own government-funded health insurance schemes, either in addition to or integrated with PM-JAY.

Note: For a detailed state-wise breakdown, including how to apply, see our full guide on state government health insurance schemes.

Is Government Health Insurance Enough for You?

For a family with no other coverage and limited income, government health insurance can be the difference between getting treated and not being treated. That matters, and it should not be dismissed.

But if you are a middle-class family with a salaried income, aging parents, or anyone in the household with a chronic condition, relying on a government scheme as your only health cover is a financial risk.

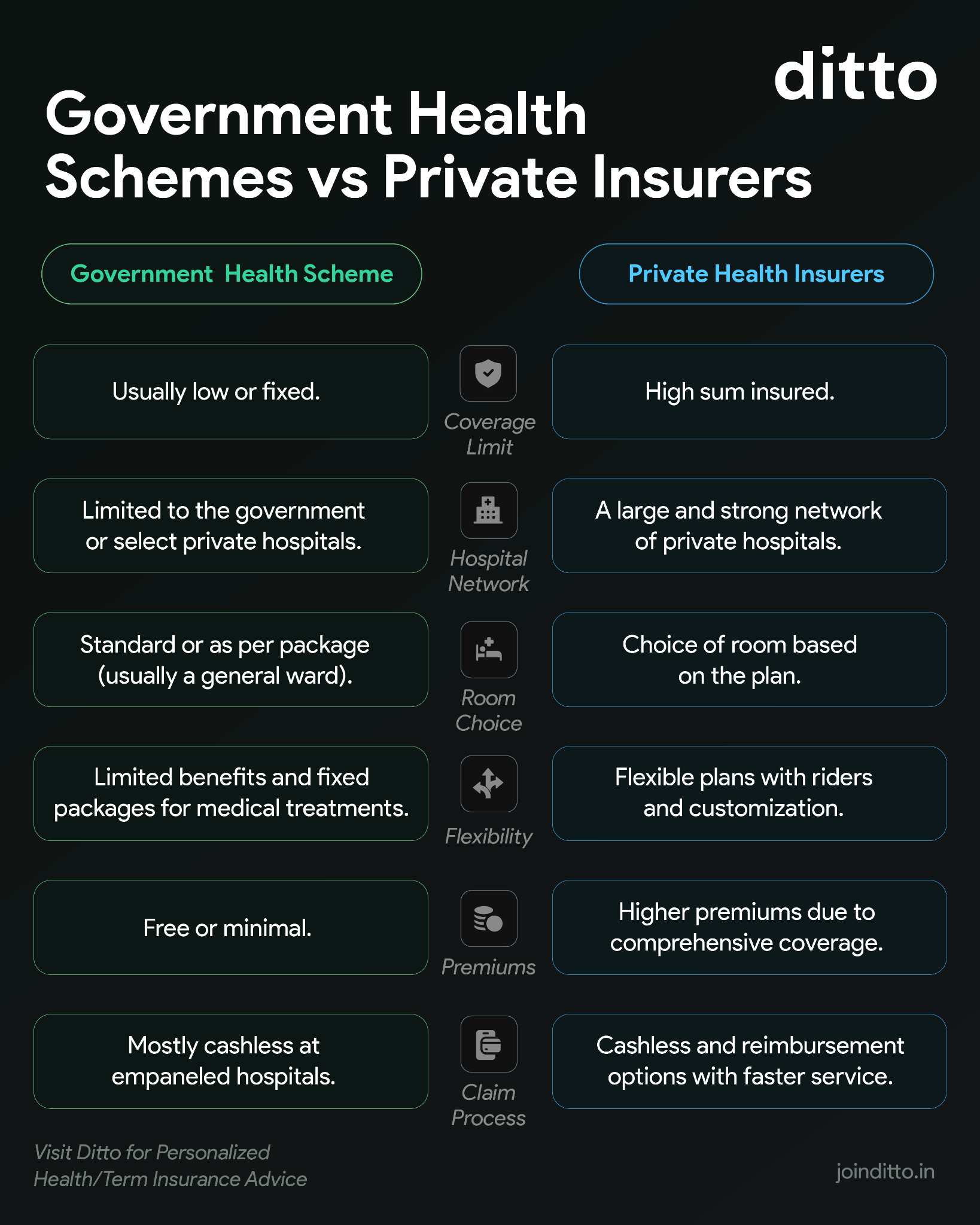

The ₹5 Lakh Cap Is Not Enough

Medical inflation in India has been rising sharply. What costs a few lakh today will cost significantly more in just a few years, and serious conditions like cancer, heart disease, or a prolonged ICU stay can push expenses well beyond what most government schemes cover in an entire year. Once the cover runs out, there are no top-ups, riders, or restoration.

Hospital Access May Be Limited

The majority of hospitals under government schemes are smaller facilities. Top-tier hospitals like Apollo, Fortis, and Manipal are largely outside the network. Even empaneled hospitals sometimes stop accepting government cards when reimbursement payments are delayed. If you want treatment at the hospital and doctor of your choice, a government scheme cannot reliably deliver that.

Consultations, Diagnostics, and Medicines Are All Out-of-Pocket

PM-JAY and most state schemes cover hospitalization only. Routine doctor visits, lab tests, and medicines outside a hospital stay are not covered. This matters because a large part of healthcare spending in India happens at the OPD level, not through admissions. CGHS covers OPD for central government employees, but only a limited portion of the population. For everyone else, outpatient costs remain fully out-of-pocket.

Government Schemes Can Change

Government health programs depend on annual budget allocations, state-level implementation, and political continuity. PM-JAY's hospital network, package rates, and eligibility criteria have changed multiple times since 2018. A scheme that covers a procedure today may not cover it next year.

On the other hand, a private health insurance policy is a legal contract with a licensed insurer regulated by IRDAI. The terms you buy are the terms you get, and the insurer cannot change them arbitrarily at renewal.

Have a look at the infographic below to compare government health insurance schemes and private insurers to get a better understanding:

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Conclusion

Government health insurance schemes in India cover a large segment of the population. PM-JAY reaches 55 crore beneficiaries. CGHS protects the central government and its employees. ESIC covers the organized-sector workforce. State schemes such as Swasthya Sathi, Aarogyasri, and HIMCARE add another layer of coverage for eligible residents.

That is real coverage. But it is not complete coverage. Low sum insured, restricted hospital networks, no OPD benefit, and dependence on political changes will mean these schemes work best as a baseline, not a final answer.

Ditto's Take: Government health insurance is a safety net, not a replacement for a primary health plan. If you are in the eligible segment, claim it because there is no reason not to. But do not let it substitute for a personal, lifelong, and customizable private policy. The two serve completely different purposes, and ideally, you should have both. If you’re exploring retail policies, have a look at our detailed guide on the best health insurance plans in India.

Frequently Asked Questions

Last updated on: