Overview

According to the HDFC Annual Report 2025-26, the company manages an annual average Assets Under Management (AUM) of ₹8.9 lakh crore. Scale like this naturally attracts investors, but the real question is whether HDFC investment plans align with your financial goals, risk appetite, and return expectations.

In the next few minutes, this guide breaks down HDFC's investment options and helps you choose the right one.

Take Note: The HDFC investment options discussed here are offered by separate regulated entities: HDFC Life for insurance-linked plans, HDFC AMC for mutual fund schemes, and HDFC Bank for deposit products.

Types of HDFC Investment Plans

Note: If you want a safer and fixed-income type of investment, open Fixed Deposits (FDs) and Recurring Deposits (RDs) with HDFC Bank. They provide greater certainty, with interest rates currently reaching around 6.50% for regular investors and 7.00% for senior citizens, making them suitable for short- to medium-term goals where capital protection matters more than growth.

In guaranteed savings plans, the maturity payout may be predefined, but the true return is best assessed through the Internal Rate of Return (IRR). For ULIPs, strong fund performance does not automatically translate into equivalent policy returns, as charges such as mortality, policy administration, and fund management can impact the final outcome.

While comparing HDFC investment plans, it is worth looking beyond insurance-linked products as well. Long-term savers may also consider government-backed options like Public Provident Fund (PPF), National Pension System (NPS), and Sukanya Samriddhi Yojana. These options offer different combinations of tax benefits, risk levels, liquidity, and return potential.

HDFC Investment Plans by Tenure (1 to 12 Years)

1) 1–4 Years: Prioritize Liquidity Over Insurance

For short-term goals, HDFC Life investment plans are generally not the ideal fit. ULIPs come with a 5-year lock-in, while traditional savings plans often have poor surrender values in the early years. FDs, RDs, and liquid mutual funds offer better flexibility and easier access to money.

2) 5–7 Years: Proceed Selectively

A 5-year horizon makes ULIPs legally accessible, but that does not automatically make them suitable. Insurance-based investments can still restrict liquidity, and returns may not justify the lock-in. Consider them only if disciplined, long-term savings are the primary objective.

3) 8–9 Years: Compare Against Mutual Funds

This is a gray zone where HDFC investment plans become more viable, but flexibility remains important. In many cases, a combination of term insurance and mutual funds may provide better liquidity, protection, transparency, and control over your investments.

4) 10+ Years: HDFC Plans Become More Relevant

Longer horizons allow guaranteed savings plans and ULIPs to work as intended. Products such as HDFC guaranteed-income and maturity-benefit plans are designed for goals that are a decade or more away, where investors can comfortably commit to lower liquidity.

5) 12+ Years: Focus on Returns, Not Just Guarantees

For very long-term goals, compare the expected Internal Rate of Return (IRR) of HDFC savings plans against alternatives such as mutual funds, PPF, and other retirement-oriented investments. The best choice depends on whether you value guarantees, growth potential, or flexibility the most.

Note: For investment horizons of 5 years or longer, and if you are comfortable taking some market risk, equity and balanced funds can become viable options for long-term wealth creation. These can be accessed through direct mutual funds or via the investment component of a ULIP, depending on your preference for flexibility, insurance needs, liquidity, and overall financial goals.

Returns, Charges, and Lock-In Explained

Tax Treatment and Liquidity

- Section 80C Benefits: Premiums paid toward eligible HDFC Life plans qualify for tax deductions under Section 80C of the old regime, up to ₹1.5 lakh.

- Section 10(10D) Exemption: Maturity proceeds can be tax-free only if prescribed conditions are met. Death benefits remain tax-exempt irrespective of premium thresholds.

- ULIP Tax Rule: For ULIPs issued on or after 1 February 2021, the Section 10(10D) exemption may not apply if aggregate annual premiums exceed ₹2.5 lakh. These will be subject to capital gains tax, similar to mutual funds.

- Non-ULIP Tax Rule: For traditional life insurance policies issued on or after 1 April 2023, maturity proceeds may become taxable if annual premiums exceed ₹5 lakh.

Note: Mutual funds generally offer superior liquidity. ULIPs have a mandatory 5-year lock-in, while guaranteed savings plans often impose surrender penalties that can significantly reduce returns on early exit. ULIPs allow partial withdrawals only after the lock-in period. Guaranteed plans may offer policy loans or surrender options, but access depends on the policy acquiring a surrender value.

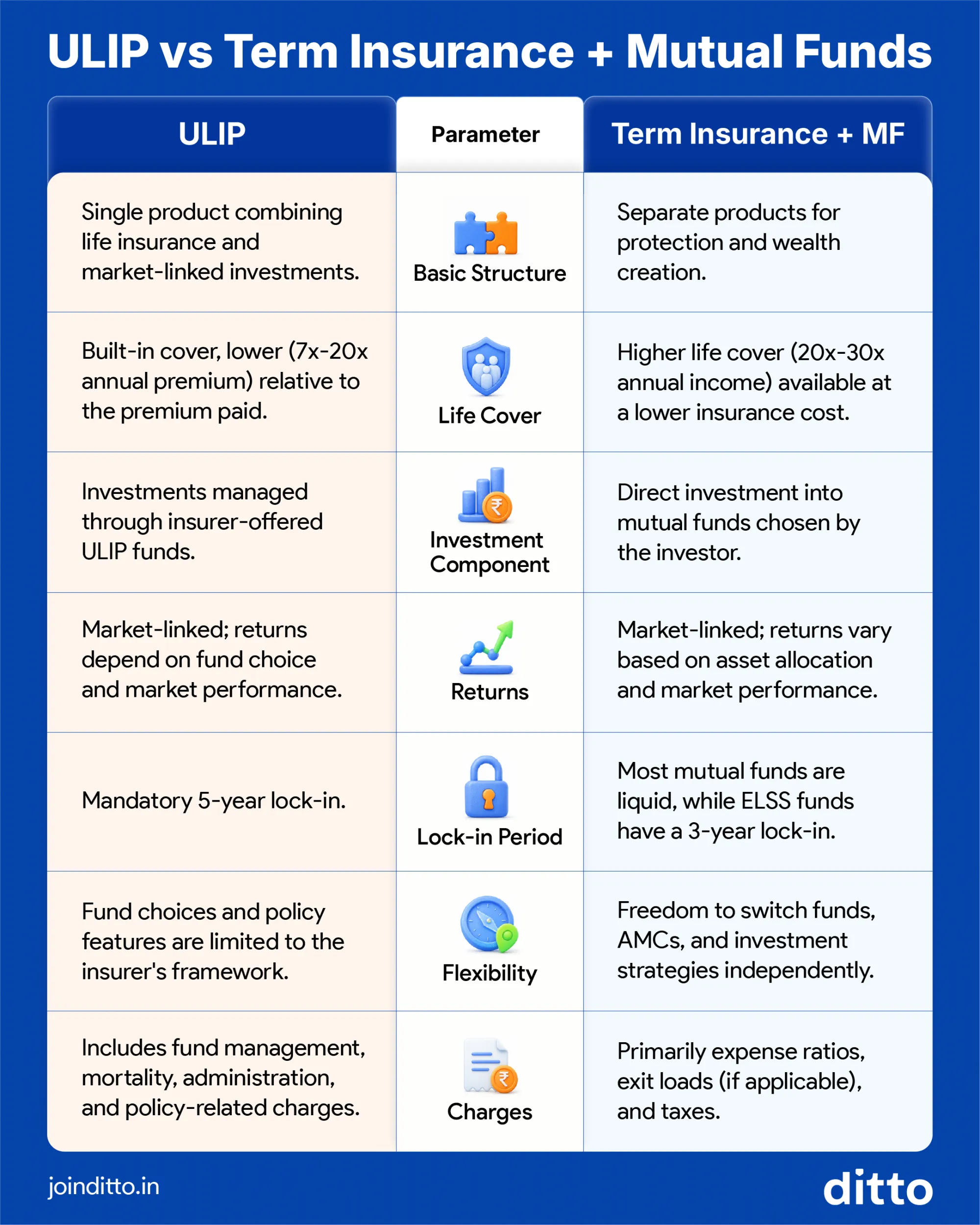

HDFC Investment Plans vs. Term Plus Mutual Funds

Investment plans, such as HDFC ULIPs, combine life insurance and investing into a single product. In contrast, the term insurance plus mutual fund approach separates protection and wealth creation into two specialized solutions.

While ULIPs offer the convenience of a bundled solution, a term plan paired with mutual funds often provides greater transparency and control. The infographic below highlights the key differences investors should evaluate before making a decision.

How to Choose the Right Plan for Your Goal

- Long-Term Wealth Creation: If your goal is wealth creation over 10+ years, consider ULIPs or mutual fund SIPs. Market-linked investments need time to benefit from compounding. You can use the HDFC SIP Calculator to estimate possible outcomes.

- Guaranteed Returns: If capital certainty matters more than return potential, guaranteed savings plans may be a better fit than market-linked options.

- Retirement Planning: For retirement-focused goals, look at pension and annuity plans that can provide a predictable income stream after your working years.

- Regular Income Needs: If you want steady cash flows rather than a lump sum, income-oriented plans can be more suitable than growth-focused investments.

- Short-Term Goals: For goals within 5 years, prioritize liquidity through FDs, RDs, savings accounts, or short-duration mutual funds rather than long-term insurance-based investment plans.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat on WhatsApp.

Conclusion

HDFC investment plans can serve different needs, but the right choice depends on your goal, time horizon, and liquidity requirements. For long-term investors seeking guarantees, savings plans may be worth exploring. For growth-oriented investors, market-linked options deserve consideration.

Always compare returns, costs, flexibility, and tax implications before investing. Most importantly, choose a plan that fits your financial objective rather than selecting a product solely because it carries the HDFC brand.

Health insurance and term insurance create the financial foundation that allows investments to do their intended job: build wealth. When you choose among the best term insurance plans, you can invest with greater confidence, stay invested through market cycles, and focus on long-term wealth creation rather than financial survival.

Note: Ditto is not a SEBI-registered investment advisor. Before making any investment decision, we strongly recommend consulting a qualified SEBI-registered investment advisor.

Frequently Asked Questions

Last updated on: