Investment plans help individuals grow wealth and achieve financial goals such as retirement, children's education, or long-term wealth creation. The right investment choice depends on your risk appetite, investment horizon, and return expectations.

Low-risk options include Fixed Deposits (FDs), Public Provident Fund (PPF), and Sukanya Samriddhi Yojana (SSY), which offer stability and predictable returns. For higher growth potential, you can consider equity mutual funds, the National Pension System (NPS), and Unit Linked Insurance Plans (ULIPs), which provide market-linked returns. However, a ULIP performs poorly as it combines elements of both life coverage and investment.

In case you are looking for both life protection and good returns, we recommend purchasing a term plan and investing separately. This guide is for those who wish to explore investment options to build long-term wealth.

Where are Indian investors putting their money today? The answer may surprise you. Equity mutual funds attracted ₹38.44 crore in inflows as of April 2026, highlighting the growing appetite for wealth creation. But mutual funds are just one piece of the puzzle. From safe options like PPF and FDs to market-linked investments such as NPS and equity funds, the right investment plan can help turn your financial goals into reality.

In the next few minutes, this guide will walk you through the types of investments, risk, returns, and which one helps you achieve your financial goals.

Confused whether to start investing or get your insurance coverage? Book a free call or chat on WhatsApp with a Ditto advisor, and let us help you out.

What Are Investment Plans?

Investment plans are structured strategies that help you grow your money and achieve future financial goals. In India, investments primarily refer to mutual funds, FDs, PPF, gold, or insurance-linked products like ULIPs and traditional savings plans like endowment plans. Each class of investment is regulated by different bodies, such as:

Securities and Exchange Board of India (SEBI) is the primary market regulator, and regulates financial instruments like stocks and mutual funds.

Reserve Bank of India (RBI) regulates safer investments like Government Securities (G-Secs) & Treasury Bills.

Insurance Regulatory and Development Authority of India (IRDAI) regulates insurance products like ULIPs.

Pension Fund Regulatory and Development Authority (PFRDA) regulates NPS and APY.

Note: People often tend to confuse investments with Systematic Investment Plans (SIPs). An investment is the asset/financial instrument you purchase, while an SIP is simply a periodic payment plan used to purchase that asset over time.

Types of Investment Plans in India

Investment plans in India can be grouped into broad categories, with certain products overlapping across classifications. For example, PPF is both a government-backed scheme and a fixed-income product, while ULIPs are market-linked but also related to insurance.

ULIPs, endowment plans, guaranteed income plans, pension, and annuity plans

People who want insurance cover plus disciplined savings in one product.

Note: Investments can be both long-term and short-term. Long-term investments include SIPs, while short-term investment plans include liquid funds and overnight funds.

Returns vs Risk: How to Decide What's Right for You

01

Market-Linked Investments

Market-linked investments offer returns that depend on market performance. While returns are not guaranteed, these options have historically delivered strong long-term growth potential.

02

Fixed-Income and Guaranteed Return Investments

Fixed-income options provide predictable returns and greater stability. These investments are ideal for conservative investors, short-term goals, or those who prioritize capital preservation over aggressive growth.

03

Government and Social Security Schemes

Government-backed schemes offer a combination of safety, tax benefits, and steady growth.

04

Insurance-Linked Investment Products

Insurance-linked products combine financial protection with investment or savings benefits. Depending on the product structure, returns may be market-linked, guaranteed, bonus-based, or a mix of these.

The exact returns and risks of any investment plan need a thorough examination. Return should be measured by Compound Annual Growth Rate (CAGR) for lump sum investments or Extended Internal Rate of Return (XIRR) for periodic investments. Risk should be measured by volatility, credit risk, liquidity risk, and suitability to the goal horizon.

Take Note: India's Consumer Price Index (CPI) inflation has averaged around 5–6% in recent years, which significantly impacts the real returns from traditional savings products.

A PPF return of about 7.1% translates to a real return of only 1–2% after inflation.

An FD offering 7% interest generates a real return of roughly 1.5% when inflation is 5.5%. After accounting for taxes, the picture becomes less attractive.

For an investor in the 30% tax bracket, a 7% FD delivers a post-tax return of about 4.9%, which falls below inflation and can result in a loss of purchasing power over time.

CTA

Tax Benefits on Investment Plans in India

Type

Tax Benefits

Equity Mutual Funds and Stocks

Capital gains tax is applied, where short-term gains are taxed at 20%, while long-term gains above the applicable exemption threshold of ₹1.25L are taxed at 12.5%.

Pension and Annuity Plans

Investments in eligible pension plans qualify for deductions under Section 80CCC.

National Pension System

Contributions qualify for deductions under Section 80CCD.

PPF, SSY, and ELSS Mutual Funds

All schemes qualify for Section 80C benefits of the old regime.

Life Insurance

Premiums qualify under Section 80C (old regime), while death benefits proceeds are tax-free under Section 10(10D), and maturity proceeds are exempt, subject to conditions.

Did You Know?

The Income Tax Act, 2025, has replaced the Income Tax Act, 1961, and introduced a new section numbering system. For example, Section 80C is now Section 123, Section 80D is now Section 126, and Section 10(10D) has been moved to Section 11 (read with Schedule II). While the numbering has changed, many underlying tax concepts remain broadly similar.

Popular Investment Plans in India

Fixed Deposits (FDs) and Recurring Deposits (RDs): FDs and RDs are among the simplest investment options available. They offer predictable returns and low risk, making them suitable for emergency funds or near-term financial goals. In India, current FD interest rates range from 5.00% to 8.50% Per Annum (P.A.), while RD rates range from 4.50% to 8.50% p.a.

Public Provident Fund (PPF): PPF is a government-backed savings scheme that offers tax benefits and stable returns. It is ideal for conservative investors who prioritize capital protection. The current PPF interest rate is 7.1% per annum.

National Pension System (NPS): NPS combines equity and debt investments to help investors create long-term retirement wealth at a relatively low cost. As of March 2026, NPS had over 2.17 crore subscribers.

Mutual Funds: These provide access to professionally managed portfolios across equity, debt, and hybrid categories. India's mutual fund industry managed assets worth ₹81.92 lakh crore in April 2026, highlighting its growing popularity among investors.

Annuity Plans: Annuities convert a lump sum into a steady stream of income after retirement. They can provide peace of mind for retirees who want a predictable cash flow. The trade-off is lower growth potential and limited liquidity.

Besides the above, people also invest in the Sukanya Samriddhi Yojana (SSY) and Senior Citizens’ Savings Scheme (SCSS). SSY is a government-backed savings scheme focused on long-term wealth creation for a girl child, while SCSS is a government-backed, fixed-rate retirement program designed for individuals over 60.

Note: Indians are not yet large direct investors in corporate bonds. This market remains institution-heavy, though retail access is improving through lower ticket sizes, SEBI-regulated online bond platforms, and better disclosure infrastructure.

Are Indians Still Conservative With Their Investments?

Yes, at the household level. Deposits, provident and pension funds, and insurance still dominate household financial savings. However, digitally active retail investors are increasingly using Exchange Traded Funds (ETFs), index funds, gold ETFs, and arbitrage funds.

Silver ETFs attracted ₹10,755 crore in April 2026 as ETF inflows in April 2026, reflecting strong investor interest in precious metals as a portfolio diversification tool.

Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InvITs) are becoming popular among investors looking for listed exposure to real estate and infrastructure income. REITs and InvITs raised a combined ₹30,325.66 crore in FY 2025-26, where InvITs accounted for the larger share, mobilizing ₹21,025.66 crore during the year.

From an insurance perspective, Indian investors continue to favor safety over market-linked growth. IRDAI data shows that as of March 2025, traditional non-linked life insurance products accounted for 87.77% of total life insurer funds, with assets of ₹59.50 lakh crore, while ULIPs represented just 12.23%, with assets of ₹8.28 lakh crore.

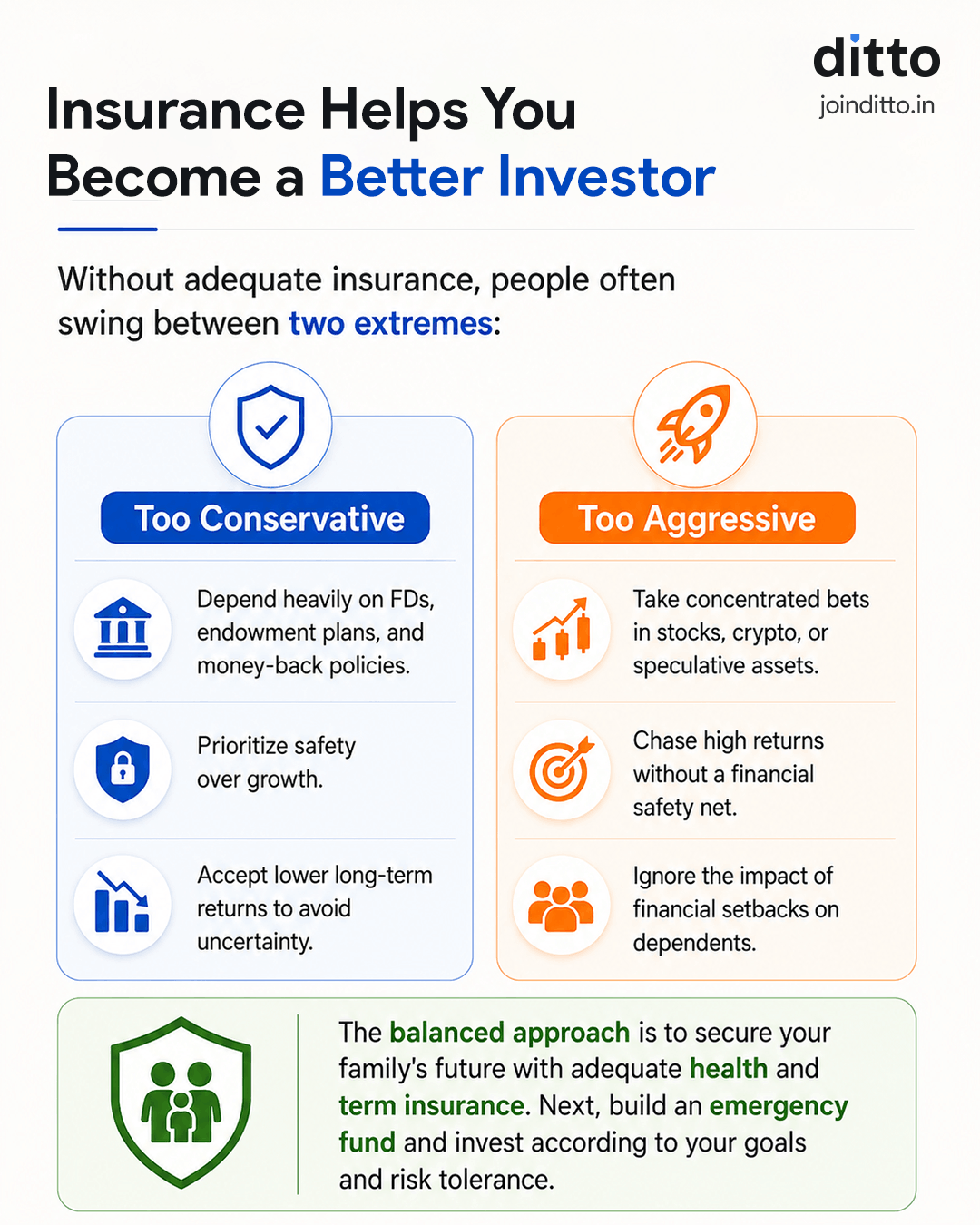

When Should You Not Buy an Investment-Linked Insurance Plan?

Investment-linked insurance plans such as ULIPs and traditional savings-cum-insurance policies are not suitable for everyone.

You may want to avoid them if your primary goal is either maximum life cover or maximum investment returns.

Products like ULIPs include mortality charges, among other ULIP charges. These offer limited liquidity with lower insurance coverage relative to the premium paid, and product structures that can be difficult to understand.

They also require periodic review of fund choices, performance, and policy features, which may not suit investors looking for a simple, hands-off approach.

At Ditto, we follow the separation principle: insurance is meant to protect your family's financial future if something happens to you, while investments are meant to build wealth over time. When a single product tries to achieve both objectives, it often involves compromises on cost, flexibility, coverage, or returns.

Having proper insurance creates better investors by removing fear and allowing for optimized, long-term risk-taking. When basic life, health, and property risks are covered, an investor no longer needs to treat their portfolio as an emergency fund.

Take a look at the infographic to understand how having proper protection in place creates better investors.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 24,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat on WhatsApp.

Conclusion

There is no single "best" investment plan in India. However, before investing, focus on understanding what the product is designed to do rather than chasing the highest advertised returns.

If You're a First-Time Earner: Start with the basics. Build an emergency fund, secure adequate health and term insurance, and then explore long-term options such as mutual funds or fixed deposits based on your goals and risk appetite.

If You're Comparing Different Investment Options: Look beyond headline returns. Compare liquidity, taxation, risk, lock-in periods, and historical performance.

If an Agent Recently Pitched a "Top Investment Plan": Take a step back and review the product carefully. Check the actual returns, charges, lock-in period, life cover, and flexibility.

Any investment decision should be made after consulting a qualified financial professional. Ditto focuses exclusively on helping customers understand and purchase health insurance and term life insurance policies and is not a SEBI-registered investment advisor.

Frequently Asked Questions

What are the main types of investment plans available in India?

Investment plans in India can broadly be grouped into four categories. Market-linked options include equity mutual funds, debt funds, hybrid funds, stocks, and ULIPs, where returns depend on market performance. Fixed-income products such as Fixed Deposits, Recurring Deposits, PPF, and NSC offer more predictable returns. Government-backed schemes like NPS, SSY, and SCSS focus on long-term savings with tax benefits. Insurance-linked products such as ULIPs and endowment plans combine protection with savings. The right choice depends on your financial goals, investment horizon, liquidity needs, and risk tolerance.

What is the difference between SIP and lump sum investment in mutual funds?

A SIP allows you to invest a fixed amount at regular intervals, usually every month, while a lump sum investment involves investing a larger amount in one go. SIPs help build investing discipline and reduce the impact of market volatility through rupee cost averaging. As of March 2026, SIP assets stood at ₹16.85 lakh crore and accounted for over 20% of total mutual fund assets, highlighting their popularity among Indian investors. The choice between a lump sum investment and SIP comes down to your cash flow, risk tolerance, and when the funds to invest become available.

What is PPF, and how much return does it offer?

The Public Provident Fund (PPF) is a government-backed long-term savings scheme designed for conservative investors. It currently offers an interest rate of 7.1% per annum and comes with a 15-year tenure. One of its biggest advantages is its Exempt-Exempt-Exempt (EEE) tax status. Contributions qualify for tax deductions under Section 80C (old regime), the interest earned is tax-free, and maturity proceeds are also exempt from tax. PPF is ideal for investors who prioritize capital safety, tax efficiency, and long-term wealth accumulation. It especially suits those who fall outside the EPF purview (self-employed or gig workers).

What is NPS, and what returns can investors expect?

The National Pension System (NPS) is a government-regulated retirement savings scheme that invests across equity, corporate debt, and government securities. Returns are market-linked and depend on asset allocation, but historically, many NPS equity funds have delivered returns in the 9% to 12% range over longer periods. As of March 2026, NPS had more than 2.17 crore subscribers. The scheme also offers attractive tax benefits. At retirement, up to 60% of the accumulated corpus can be withdrawn tax-free, while the remaining amount is generally used to purchase an annuity for regular retirement income.

Is PPF or NPS better for retirement planning?

PPF and NPS serve different investor needs. PPF offers government-backed returns, capital protection, and complete tax efficiency, making it suitable for conservative investors. NPS, on the other hand, provides market-linked growth potential and an additional tax deduction of ₹50,000 under Section 80CCD(1B), over and above the Section 80C (old regime) limit. Investors seeking higher long-term returns may prefer NPS, while those prioritizing stability may lean toward PPF. In practice, many investors use both products together to balance safety and growth while building a diversified retirement portfolio.

How Does Insurance Encourage Smarter Investment Decisions?

Adequate insurance creates a financial safety net that allows investors to take calculated risks rather than emotional ones. Without proper protection, people often fall into one of two extremes. Some become overly cautious and keep most of their money in low-return products like endowment plans simply because they feel safe. Others take excessive risks through speculative investments like cryptocurrencies without considering the financial impact on their family if things go wrong. Insurance helps create a foundation of security. Once major risks are covered, investors can make more rational decisions and build wealth through a balanced investment strategy aligned with their long-term goals.

What are the main tax benefits of investment plans in India?

Several investment products offer tax benefits under the Income Tax Act. Contributions to PPF, ELSS mutual funds, life insurance premiums, and certain other eligible investments qualify for deductions under Section 80C, subject to the prescribed limit. NPS offers an additional deduction of up to ₹50,000 under Section 80CCD(1B). Life insurance proceeds may qualify for tax exemption under Section 10(10D), subject to applicable conditions. Tax treatment also varies for mutual funds, stocks, and pension products. Investors should review current tax rules carefully and seek professional guidance when required.

What is an emergency fund, and how much should I save?

An emergency fund is money set aside for unexpected events such as job loss, medical expenses not covered by insurance, urgent home repairs, or other financial emergencies. Ideally, it should cover 6 to 12 months of essential expenses and be kept in easily accessible options such as a savings account, sweep account, or liquid mutual fund. As your income, lifestyle, and financial responsibilities grow, your emergency fund should grow as well. Having this buffer prevents you from breaking long-term investments or taking expensive loans during difficult situations, allowing your wealth-building plan to stay on track.

How much health and term insurance should I have before investing?

Before focusing on wealth creation, ensure your financial foundation is secure. While you choose among the best health insurance plans, look for at least ₹15 lakh health cover, which helps protect your savings from rising medical costs. If you have dependents, a term insurance cover of ₹1 crore to ₹2 crore strikes the correct balance between affordability and adequate life coverage. However, before choosing among the best term insurance plans, have an understanding of how much term cover is required. To get a better understanding, use our cover calculator to find the ideal cover for you.

How does term insurance affect your ability to take investment risk?

Many investors focus only on risk tolerance, which means how much market volatility they can emotionally handle. However, risk capacity is equally important. It reflects how much financial risk your situation can realistically support. Without adequate term insurance, your family may have to depend on your investments if something happens to you, which can force a more conservative investment approach. A well-sized term plan provides a financial safety net for your dependents. This can improve your risk capacity and allow your investment portfolio to be aligned more closely with your long-term goals, time horizon, and wealth-creation objectives.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.