LIC investment plans broadly fall into three categories: market-linked Unit-Linked Insurance Plans (ULIPs), guaranteed savings plans, and retirement-focused income plans. Investors seeking growth can consider LIC Nivesh Plus, which offers equity market exposure and higher return potential with market risk.

Those who prefer predictable outcomes may look at LIC Jeevan Labh or LIC Money Back Plans, which provide guaranteed benefits. For retirement planning and lifelong income, LIC Jeevan Umang is a popular option.

Most plans offer tax benefits and exemptions, subject to prevailing tax rules. The right choice depends on your investment horizon, liquidity needs, risk appetite, and income goals. However, at Ditto, we recommend keeping life coverage and investments separate so that both work efficiently. This guide suits those who wish to explore LIC's investment plans.

As per LIC's press release dated May 21, 2026, the insurer's Assets Under Management (AUM) crossed a staggering ₹57.29 lakh crore, reinforcing its position as India's largest life insurer. This massive corpus highlights LIC's unmatched scale, decades-long customer trust, and its significant role in managing the long-term savings and protection needs of millions of Indian households.

In the next few minutes, this guide will walk you through popular LIC investment plans, their core features, and help you understand whether they are the right investment choice for you.

Unsure if a LIC investment plan will align with your future goals? Book a free call or chat on WhatsApp with a Ditto advisor, and let us help you out.

Types of LIC Investment Plans

Category

Return Nature

Risk Level

Examples

Endowment / Savings Plans

Bonuses and/or guaranteed additions with maturity benefits

Low market risks, but inflation may reduce real returns

In addition to LIC's traditional insurance plans, investors can access LIC-linked investment opportunities through two separate non-insurance entities.

LIC Mutual Fund is the investment arm of the LIC group and offers SEBI-regulated mutual fund schemes across equity, debt, hybrid, and index categories. Here, investors are making a pure investment in funds like LIC Large Cap without any life insurance component.

LIC Housing Finance is a listed housing finance company promoted by LIC and offers fixed deposits, including the Sanchay Public Deposit Scheme, as well as other fixed-income products. These options are better suited for conservative investors seeking predictable returns and capital stability rather than market-linked growth.

CTA

Popular LIC Investment Plans

01

LIC Jeevan Umang (Plan 745)

A whole-life insurance plan that provides guaranteed annual survival benefits after the premium payment term ends and continues these payouts until age 100. It also offers a lump-sum maturity or death benefit, making it suitable for those seeking lifelong income and protection.

02

LIC Jeevan Utsav (Plan 771)

A limited-premium whole-life plan that pays a guaranteed annual income equal to 10% of the basic sum assured after the premium payment term. It is designed for individuals seeking a predictable lifelong income.

03

LIC Jeevan Labh (Plan 736)

A limited-premium endowment plan that combines insurance and savings. It provides a lump-sum maturity benefit comprising the sum assured and accrued bonuses, making it popular for long-term financial goals.

04

LIC New Jeevan Anand (Plan 715)

A traditional participating endowment plan that offers maturity benefits along with bonus additions. A unique feature is that the life cover continues even after the policy matures, providing extended financial protection.

05

LIC Index Plus (Plan 873)

A market-linked ULIP that combines life insurance with investments linked primarily to the NIFTY 50 and NIFTY 100 Index. It suits investors who want equity-market exposure and are comfortable with market fluctuations.

06

LIC Nivesh Plus (Plan 749)

A single-premium ULIP that allows investors to allocate a lump sum across multiple fund options. It offers fund switching and partial withdrawal facilities, making it suitable for long-term market-linked wealth creation.

07

LIC New Jeevan Shanti (Plan 758)

A single-premium deferred annuity plan that converts a lump-sum investment into a guaranteed future pension. It is primarily aimed at retirement planning and creating a predictable income stream in later years.

Realistic Returns and IRR Explained

When evaluating any investment or insurance-linked savings plan, the advertised maturity amount rarely tells the complete story. A more meaningful measure is the Internal Rate of Return (IRR), which converts all premiums paid and benefits received into an annualized return after accounting for charges.

This allows investors to compare LIC plans, ULIPs, fixed deposits, mutual funds, and other investments on a like-for-like basis and understand the true earning potential of their money.

Let’s take the example of LIC Nivesh Plus for a clearer understanding.

Sample Premiums

Aspect

Figures

Total Premium

₹1,25,000

Policy Term

20 years

Projected Value at 4% Gross Return

₹1,36,076

Projected Value at 8% Gross Return

₹4,41,480

Note: Projected values are illustrative and based on assumptions shown in the LIC Nivesh Plus brochure for a 30-year-old investing in Option 2. Actual fund value and maturity benefits will depend on market performance, policy charges, and the chosen investment tenure.

Key Insights:

A ₹1.25 lakh investment under LIC Nivesh Plus Option 2 provides a life cover of ₹12.5 lakh, which is inadequate for most families, which typically require ₹1 to ₹2 crore of protection. While selecting a term plan, people often get underinsured or overinsured. Use our term cover calculator to get an estimate of the life coverage you require.

To secure ₹1 crore coverage through this ULIP, you would need to invest approximately ₹10 lakh upfront, making it a relatively expensive way to buy insurance.

On the other hand, a pure term insurance plan can provide ₹1 crore coverage for roughly ₹10,000–₹15,000 per year for a young, healthy individual, offering substantially higher protection at a much lower cost.

Apart from the high premiums, ULIPs incur multiple charges that can reduce effective investment returns over time.

Even if the underlying fund earns 8% annually, the net return after fees may fall to around 6.8%, significantly reducing long-term wealth accumulation.

On a ₹1.25 lakh investment over 20 years, this return difference can reduce the final corpus by over ₹60,000, with the gap widening further over longer periods and larger investment amounts.

By combining a low-cost term plan with separate investments, you retain greater flexibility across low-cost index funds, Fixed Deposits (FDs), Public Provident Fund (PPF), National Pension System (NPS), and other investment options.

Charges, Lock-In, and Surrender Value

Plan Type

Charges

Lock-in / Liquidity

Surrender Value

Participating Endowment Plans

Charges are built into premiums. (Rider premiums, extra premiums, and taxes apply separately)

No formal lock-in. Surrender is usually allowed after one full policy year and payment of one full year's premium

Usually, the higher of guaranteed surrender value or special surrender value, subject to policy rules and premium history

Non-Par Guaranteed Savings Plans

Charges are embedded. Returns come through guaranteed additions and predefined benefits

Limited liquidity in early years. Surrender is generally allowed after one policy year and one full premium paid

Based on premiums paid and accrued guaranteed additions, subject to surrender factors and policy terms

Money-Back Plans

Charges are embedded within policy pricing. Periodic payouts may reduce long-term compounding

Survival benefits are paid periodically, but surrender eligibility follows standard policy conditions

Calculated using premiums paid, surrender factors, and adjusted for survival benefits already received.

ULIPs

Includes FMC, mortality, policy administration, switching, withdrawal, and discontinuance charges

Mandatory 5-year lock-in. No free access to funds during the lock-in period

Early exit moves the proceeds to the Discontinued Policy Fund. After 5 years, the fund value can generally be withdrawn

Pension ULIPs

Similar to ULIP charges with additional pension-related exit provisions

5-year lock-in and retirement-focused withdrawal rules

Discontinued funds move to a separate fund during lock-in and are governed by pension and annuity rules

Immediate Annuity Plans

Charges are built into annuity pricing. No separate investment management fee

Designed for long-term income. Liquidity is very limited

Surrender is available only under selected options and may result in a significant reduction in value

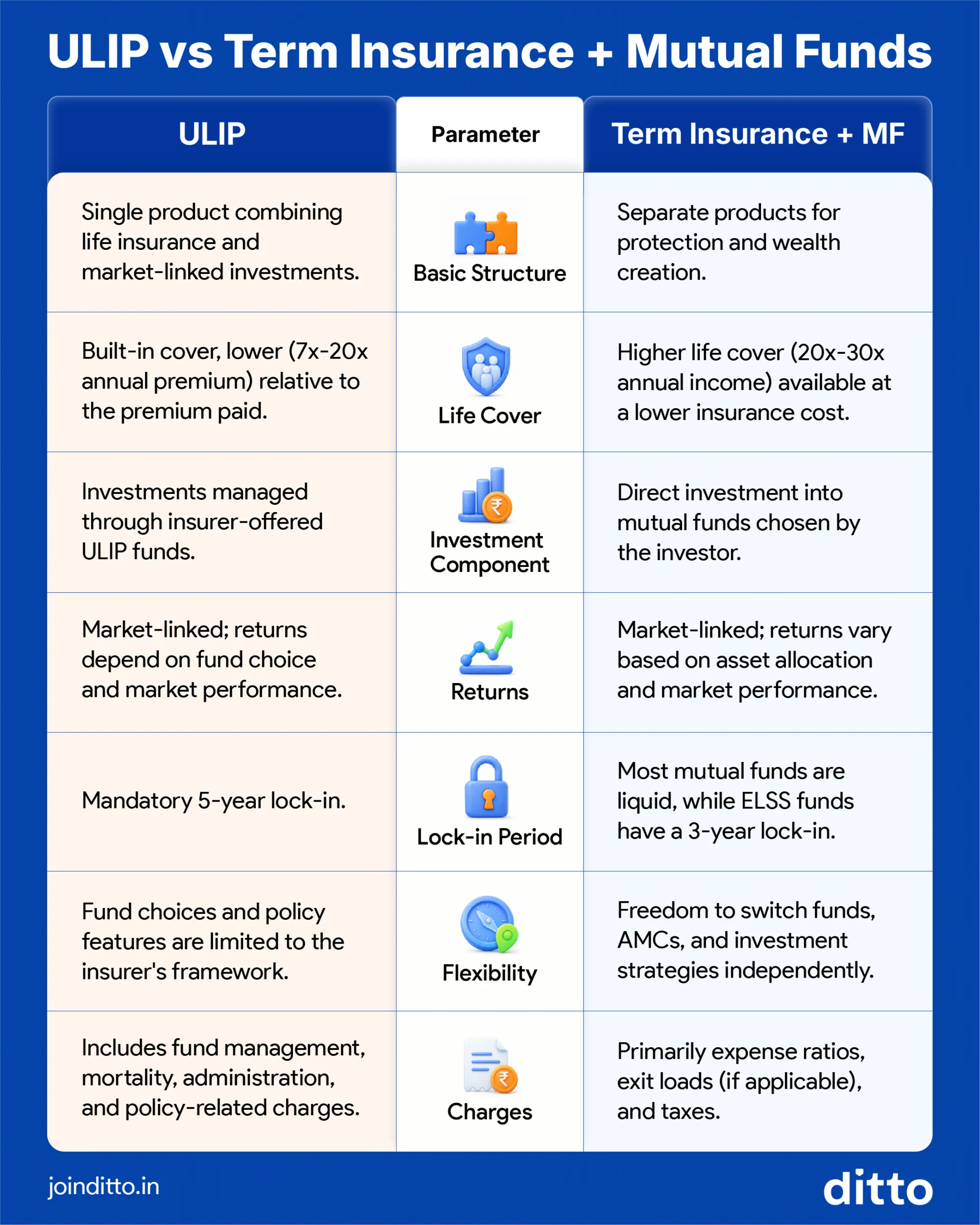

LIC Plans vs Term Plus Mutual Funds

Traditional LIC plans and ULIPs combine insurance and investing in a single product, offering convenience, disciplined savings, and, in some cases, guaranteed benefits. However, returns from traditional plans are moderate, while ULIPs come with lock-ins and multiple charges.

On the other hand, an affordable term insurance plan focuses purely on protection, while the premium savings compared to a ULIP can be invested separately in mutual funds. This separation gives investors greater flexibility, transparency, and liquidity.

See the infographic below to understand how ULIPs differ from the term insurance + mutual fund approach.

Who Should Consider LIC Investment Plans?

LIC investment plans are suitable for investors who prefer capital protection and are comfortable with moderate, long-term wealth accumulation rather than aggressive market-linked growth.

They are ideal for individuals seeking a combination of life insurance cover and disciplined savings in a single product, and for those seeking to take advantage of the Section 10D maturity payout tax exemption rules. Maturity proceeds are taxable if the aggregate annual premium exceeds ₹2.5 lakh for ULIPs issued on or after February 1, 2021, or ₹5 lakh for eligible traditional life insurance policies issued on or after April 1, 2023.

They also appeal to conservative investors who value guaranteed or bonus-linked benefits backed by a long-established insurer.

These plans are useful for parents planning for the future, such as a child's education, marriage, or family wealth transfer.

They are appropriate for retirees and pre-retirees seeking predictable income streams through pension and annuity-based LIC plans.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 24,000+ happy customers

LIC investment plans can play a role in long-term financial planning, but they should be selected based on your objective rather than brand familiarity. Traditional plans may suit investors seeking capital protection and predictable outcomes, while LIC ULIPs may appeal to those comfortable with market-linked growth and a longer investment horizon.

However, if you wish to maximize returns, a pure term plan, among the best term insurance plans, along with separate investments, will be fruitful. If you prefer LIC as your insurer, explore plans such as LIC Bima Kavach.

Note: Ditto is not a SEBI-registered investment advisor. Before investing, consult a professional, compare expected returns through IRR, assess liquidity needs, and review tax implications. Most importantly, ensure your financial foundation (health + term insurance) is strong.

Frequently Asked Questions

Are LIC plans for investment better than mutual funds?

LIC investment plans and mutual funds serve different purposes. LIC plans combine insurance and savings, while mutual funds focus purely on investments. Traditional LIC plans like endowment plans generally offer stability and predictable outcomes, but often generate lower long-term returns than equity mutual funds. Mutual funds provide greater flexibility, transparency, and liquidity. Investors seeking wealth creation often prefer separate investments through low-cost mutual funds, while those valuing bundled insurance and savings may prefer LIC products. The choice depends on whether your priority is protection, convenience, liquidity, growth potential, or a combination of these factors.

What are the different types of LIC investment plans?

LIC investment plans can broadly be divided into endowment plans, money-back plans, whole-life plans, ULIPs, pension plans, and micro-insurance products. Endowment plans focus on savings and protection. Money-back plans provide periodic payouts during the policy term. Whole-life plans offer lifelong coverage and income-oriented benefits. ULIPs invest premiums into market-linked funds and offer growth potential. Pension plans help generate retirement income, while micro-insurance plans provide basic protection and savings for lower-income households. Understanding the category is often more important than selecting an individual plan because each category addresses a different financial objective.

Should I choose a LIC ULIP or a term plan plus a mutual fund?

Both approaches can work, but they are structured differently. A LIC ULIP combines insurance and investment within a single policy and comes with a mandatory five-year lock-in period and associated ULIP charges. Returns depend on fund performance and policy-level charges. A term plan plus mutual fund approach separates protection and investment. This provides significantly higher life cover at a lower cost, while allowing greater investment flexibility and liquidity. Investors can choose mutual funds that match their risk profile and goals. The decision ultimately depends on whether you prefer a bundled solution or the flexibility of managing insurance and investments separately.

Are LIC maturity proceeds tax-free?

In many cases, yes. Maturity proceeds from traditional LIC plans, such as endowment, money-back, and whole-life policies, are generally exempt under Section 11 of the Income Tax Act, 2025 (earlier Section 10(10D)), provided the premium-to-sum-assured conditions are met. However, special rules apply to newer policies. For ULIPs issued on or after 1 February 2021, the exemption is available only if aggregate annual ULIP premiums do not exceed ₹2.5 lakh. For traditional non-ULIP policies issued on or after 1 April 2023, maturity proceeds become taxable if aggregate annual premiums exceed ₹5 lakh. Death benefits remain tax-exempt irrespective of these limits.

How does a LIC investment plan compare with PPF for long-term savings?

PPF and LIC investment plans cater to different needs. PPF is a government-backed savings scheme that currently offers a fixed interest rate of 7.1%, tax-efficient accumulation, and a 15-year tenure. Traditional LIC savings plans combine insurance with long-term savings but often generate lower effective returns (often under 6.5%) when measured through IRR. PPF generally provides greater transparency and straightforward compounding, while LIC plans add a life insurance component. Investors focused primarily on long-term wealth accumulation often compare the expected return, liquidity, tax treatment, and insurance value before deciding which option better aligns with their financial objectives.

Can I claim tax deductions on LIC policy premiums?

Yes, premiums paid towards most LIC traditional plans and ULIPs qualify for a tax deduction under Section 123 of the Income Tax Act, 2025 (earlier Section 80C), subject to a combined annual limit of ₹1.5 lakh. However, this benefit is available only under the old tax regime and cannot be claimed under the new default regime. To qualify, the annual premium should generally not exceed 10% of the sum assured. Premiums paid towards LIC pension and annuity plans are also eligible, but they share the same overall ₹1.5 lakh deduction limit.

What are the charges in LIC ULIP plans that reduce returns?

LIC ULIPs include several charges that can affect long-term returns. These ULIP charges include fund management charges, mortality charges for life cover, policy administration charges, switching charges, and, in certain situations, discontinuance charges. While fund performance figures are often shown after deducting fund management charges, policy-level charges can further reduce the investor’s outcome. This is why the fund return and policy return are not always the same. Investors should carefully review the benefit illustration, understand all applicable charges, and assess the effective return rather than relying solely on the fund’s historical performance.

What happens if I surrender a LIC investment plan early?

Early surrender can significantly affect the value received from a LIC policy. For traditional plans, surrender values are typically lower in the initial years. In ULIPs, surrendering within the five-year lock-in period results in the fund value being transferred to a Discontinued Policy Fund after applicable deductions. Life cover ceases once the policy is discontinued. You can also consider converting the policy to paid-up status if the surrender loss is too high. If you are evaluating LIC investment plans for 5 years, do not explore ULIPs due to the mandatory lock-in period.

Does LIC offer Fixed Deposits (FDs)?

LIC itself does not offer fixed deposits. However, its subsidiary, LIC Housing Finance Limited, provides corporate fixed deposits under the Sanchay Public Deposit scheme. These deposits typically offer fixed interest rates (6.70% to 6.90% p.a.), flexible tenures ranging from 1 to 5 years, and additional benefits such as loan facilities against the deposit. Senior citizens usually receive a higher interest rate than regular investors. The deposits carry strong credit ratings, reflecting a high level of repayment confidence. However, unlike bank FDs, these are corporate deposits and are not covered by DICGC deposit insurance, making them fundamentally different from deposits held with commercial banks.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.