Overview

Are you looking for a simple LIC-backed plan that combines savings with basic life cover? LIC’s Micro Bachat Plan offers financial support for your family in case of death and a lump sum payout at maturity. However, this plan is available only for standard, healthy individuals and does not require any medical examination. The policy is an insurance product under IRDAI’s micro insurance initiative.

In this guide we break down the LIC Micro Bachat Plan in simple terms so you can understand its features, benefits, and limitations before making a decision.

Did You Know?

LIC: Performance Metrics

Note: These performance metrics come from IRDAI annual reports and LIC’s public disclosures for the overall insurer. These metrics are for the overall insurer, not just micro insurance, but they still give a fair indication of performance in this segment.

Key Insights:

- A CSR above 97% reflects strong reliability, supported by LIC’s government backing and long track record.

- The ASR above 90% shows balanced payouts across both small and large claims.

- A premium volume well above Ditto’s recommended mark of ₹5,000 crore highlights scale and market reach. LIC is the largest life insurer in the industry and accounted for about 55% of India’s total life insurance premium income in FY 2024–25, as per IRDAI annual reports.

- Total death claims paid around 100 times the industry average indicates strong payout capacity.

- A complaint volume at nearly one-fourth of the industry average, despite the insurer’s large scale, points to a relatively better customer experience.

- A solvency ratio above the IRDAI requirement of 1.5x confirms solid financial stability and ability to meet future claims.

Eligibility Criteria of LIC Micro Bachat Plan

Key Features of LIC Micro Bachat Plan

Built for Small, Practical Needs

This plan suits people who want a simple LIC-backed policy with a small savings element. With a sum assured of ₹1 lakh to ₹2 lakh, it functions more as a basic micro insurance option than a comprehensive protection plan.

Maturity Benefit Adds Value

If you survive the policy term, you receive a lump sum. This includes the basic sum assured and any declared loyalty addition, which adds a savings component to the plan.

Chance of Extra Returns

As a participating plan, it may offer loyalty additions based on LIC’s performance. This benefit becomes relevant after you have completed at least five years of premium payments.

Easy to Get Started

The plan is available for standard healthy lives without medical tests. This makes the buying process simple and accessible for many first-time policyholders.

Support If You Miss Payments

If you have paid premiums for at least three years, the policy may continue for a limited period even if you miss payments. This gives some breathing space during financial stress.

Extra Protection Through Riders

You can add an accidental death & disability benefit rider or accident benefit rider for additional cover. These riders can be added anytime during the policy term if the base policy is active and has at least five years remaining. The rider premium is capped at 30% of the base policy premium.

Loan Option for Emergencies

You can take a policy loan after paying at least one full year’s premium. This provides access to funds when you need them.

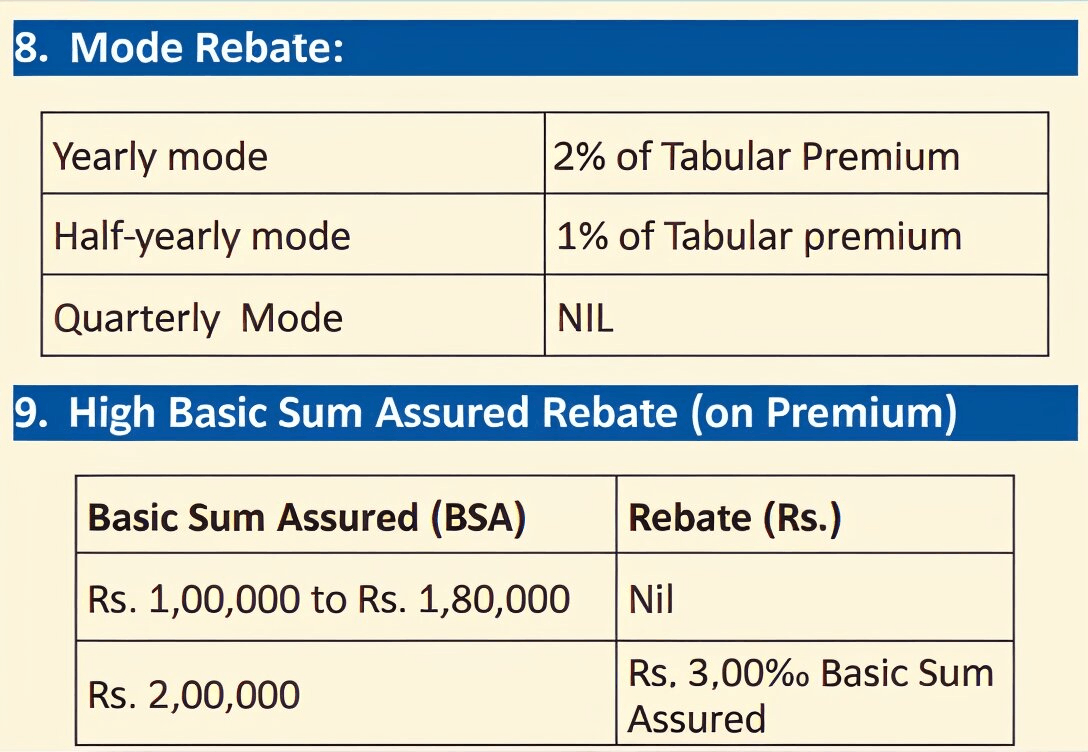

Here’s a snippet from the policy brochure about the rebates offered with the plan.

Note: The mode rebate in LIC Micro Bachat is a small discount on your premium based on how often you choose to pay. It is not a cashback or bonus. Similarly, a sum assured rebate lowers your premium slightly if you opt for a higher basic cover.

Is the Sum Assured Offered by the LIC Micro Bachat Plan Enough?

LIC Micro Bachat is not a bad plan. It is simply too small to solve what life insurance is meant to do. It offers basic support, not long-term financial security, given the rising inflation.

- Limited Cover, Limited Impact: The plan is designed to be affordable, so the cover stays low. It can help with immediate expenses, but the support does not last long and fades when bigger needs arise.

- No Real Income Replacement: Life insurance should replace the income of the earning member for years. This plan cannot support regular expenses, repay loans, or secure your family’s future goals.

- Short-Term Relief, Not Long-Term Security: It works like a short-term cushion during a crisis. It does not provide the strength needed to support dependents over the long run.

In simple terms, Micro Bachat can help for a while, but it cannot protect your family’s future.

Drawbacks of the LIC Micro Bachat Plan

- Low Life Cover: The maximum sum assured is ₹2 lakh. This amount may cover small expenses, but it cannot support income replacement, loan repayment, or long-term family needs. However, this low cover may not meet your family’s needs. Use our cover calculator to estimate the right term insurance amount for your situation.

- Not Pure Protection: This plan combines savings with insurance. As a result, the cover stays limited and does not match the protection a term plan can offer.

- Uncertain Loyalty Addition: The plan may offer a loyalty addition, but it depends on LIC’s performance. You should treat it as a bonus, not a guaranteed return.

- Full-Term Premiums: You pay premiums regularly for the entire policy term. This creates a long commitment and reduces flexibility for many buyers.

- Weak Early Exit Value: There is no surrender value in the first year. Even after two years, the payout remains low, which makes early exit unattractive.

- Reduced Paid-Up Benefits: If you stop paying premiums, the policy continues in a reduced form. Both death and maturity benefits drop in proportion, which lowers overall value.

Premium Comparison

Note: These sample premiums are illustrative and based on a ₹1 lakh sum assured. The figures are sourced from the LIC Micro Bachat policy brochure.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

LIC Micro Bachat is a micro insurance product available only for standard, healthy individuals. While it offers basic coverage, it is not built for meaningful financial protection or long-term flexibility.

- Limited benefits with no advanced features, such as instant claim payouts or health support services.

- You can opt for only one of the two riders available, and the policy lacks important rider options like waiver of premium.

If you are looking for stronger protection and flexibility, it makes sense to explore the best term insurance plans that better support your long-term financial goals.

Frequently Asked Questions

Last updated on: