Online term insurance plans are generally more cost-effective because they exclude agent commissions and paperwork charges, which can make premiums up to 5% to 10% lower than offline plans, usually for the first year. When you compare term insurance online vs offline, online plans are often more affordable and easier to manage, while offline plans may offer in-person assistance through agents or advisors.

Offline plans, however, may suit those who prefer personal guidance, paperwork support, and in-person assistance during claims. If you wish to purchase a term plan, Smart Term Plan Plus is Ditto’s top pick, backed by Axis Max, with a 99.62% claim settlement ratio (average FY 2022-25). This guide helps you understand the key differences of buying a term plan online vs offline.

Despite rapid digital adoption, insurers’ online direct sales contributed just 0.87% of individual life insurance new business premiums in FY 2025, up from 0.65% in FY 2024. This clearly shows that most Indians still prefer buying term insurance offline through agents or advisors. So, when comparing term insurance plans, the real question is not just about price. It is about guidance, disclosures, trust, and how comfortable you are managing the process yourself.

In the next few minutes, we will walk you through the advantages of online buying, why some people prefer offline purchasing, and which mode is right for you.

Note: Term plans and most core features offered by the insurer remain the same regardless of how you buy them. There is no separate category called “online term insurance” or “offline term insurance.”

Usually more affordable because there are lower distribution costs and no agent commissions.

Often expensive due to agent commissions, branch costs, or bundled recommendations.

Transparency

Easier to compare premiums, riders, exclusions, claim ratios, and policy features across insurers in one place.

Depends largely on the advisor’s knowledge and willingness to explain details clearly.

Ease of Comparison

Quick comparison across multiple insurers through insurer websites and comparison platforms.

Comparisons are usually limited to the insurers the advisor represents.

Control Over Proposal Form

You fill the form yourself, which reduces the risk of incorrect income, smoking, or medical disclosures.

There is a risk of incomplete or incorrect disclosures if the advisor fills out the form casually.

Advice and Guidance

Best suited for buyers who already understand cover amount, riders, payout options, and policy terms.

Helpful for people who want step-by-step guidance, paperwork support, and policy explanations.

Mis-selling Risk

Lower when buying directly from the insurer after reading the policy documents carefully.

Can be higher if commission-driven products or unnecessary riders are pushed aggressively.

Limitation

Buyers may choose inadequate cover or miss important riders without expert guidance.

Buyers may end up with expensive or unsuitable plans if advice is biased or incomplete.

Key Insights:

Insurers do not differentiate between online and offline customers when it comes to claim settlement, policy servicing, or customer support. Once the policy is issued, the service standards remain the same across both purchase modes.

Many people choose offline term insurance, assuming the agent will assist with claims years later. In reality, agents may switch careers, retire, or may not remain available throughout the policy tenure. Your nominee should always know how to contact the insurer directly.

Buying offline does not improve approval chances or guarantee lower premiums. The insurer’s underwriting team follows the same medical, income, and risk assessment standards regardless of the purchase channel.

Advantages of Buying Term Insurance Online

Easy Comparison Across Multiple Insurers: Buying term insurance online gives you the freedom to compare plans without pressure from insurance agents or sales teams. You can easily check the sum assured, policy term, premium payment options, and overall pricing across insurers. This helps you focus on the quality of protection instead of choosing a plan based on sales influence or personal relationships.

Full Control Over Your Proposal Form: One major advantage of buying term insurance online is that you fill out the proposal form yourself. This reduces the risk of incorrect disclosures or missing information. Details related to smoking, alcohol use, medical history, occupation, income, and existing policies play a major role in claim approval. Honest disclosure is extremely important. Even small omissions can create problems during claim settlement later.

Easier Access to Policy Documents: Online term insurance gives you direct access to important policy documents immediately after issuance. You can review the policy schedule, nominee details, rider information, and proposal form copy at your convenience. This makes it easier to spot mistakes early.

Faster, Simpler, and More Convenient: For most straightforward cases, online buying saves time and reduces paperwork. You can compare term plans, upload documents, complete payments, and track your application without visiting branches or following up repeatedly with agents.

Why Some People Prefer Buying Term Insurance Offline?

01

Personal Guidance Helps Buyers Make Better Decisions

Many people are unsure about how much life cover they actually need, which payout option works best for their family, or whether riders are worth adding. Offline buying feels easier because an advisor can explain these details step by step. A good advisor helps buyers understand the policy clearly instead of simply pushing a sale.

02

Extra Support With Health and Income Disclosures

Term insurance approval depends heavily on accurate disclosure of medical history, smoking habits, income, occupation, and existing insurance policies. Buyers with medical conditions often prefer offline assistance because they want help filling out the proposal form correctly and avoiding mistakes that could create claim issues later.

03

Helpful for Self-Employed Buyers

Self-employed applicants usually face stricter income verification during underwriting. Insurers may ask for Income Tax returns (ITRs), bank statements, balance sheets, profit and loss statements, or CA-certified documents. Offline support can make this process smoother by helping buyers organize paperwork properly and respond to insurer queries more efficiently.

04

Trust Still Plays a Big Role

Many customers still feel more comfortable discussing a large financial decision with a known person. In India, insurance often remains relationship-driven. Purchasing through someone familiar often feels more convenient and reassuring, especially for people who are less comfortable with a fully digital process.

05

Families Often Prefer Claim Assistance

A term insurance claim happens when the policyholder is no longer there to guide the family. Because of this, many families value having an advisor who can help with claim paperwork, document submission, and communication with the insurer during difficult situations. Reliable post-sales support remains one of the strongest reasons some people still prefer offline buying.

06

Easier Understanding of Policy Terms

Policy documents can feel confusing for first-time buyers. Terms related to exclusions, riders, benefit illustrations, and payout structures are not always easy to understand. Offline guidance can simplify these details and help buyers understand exactly what the policy covers and what it does not.

Online vs Offline Term Insurance: Which Should You Choose?

Purchase Mode

Best Suited For

Online Term Insurance

Salaried individuals, digitally comfortable buyers, and people with simple income and medical profiles.

Offline Term Insurance

Self-employed individuals, business owners, Non Resident Indians (NRIs), high-cover applicants, and buyers needing underwriting or documentation support.

If you wish to get expert advise on a term plan, connect with us.

CTA

At Ditto, being an IRDAI licensed corporate agent, we offer the best of both worlds (expert guidance over the phone, along with online convenience). Premiums remain the same as the insurer’s direct online prices because available discounts are passed on to customers.

Along with digital convenience, buyers also get support with plan selection, documentation, underwriting, and claims assistance at no additional cost. This gives customers the flexibility and pricing advantage of online buying without losing access to personalized support when needed.

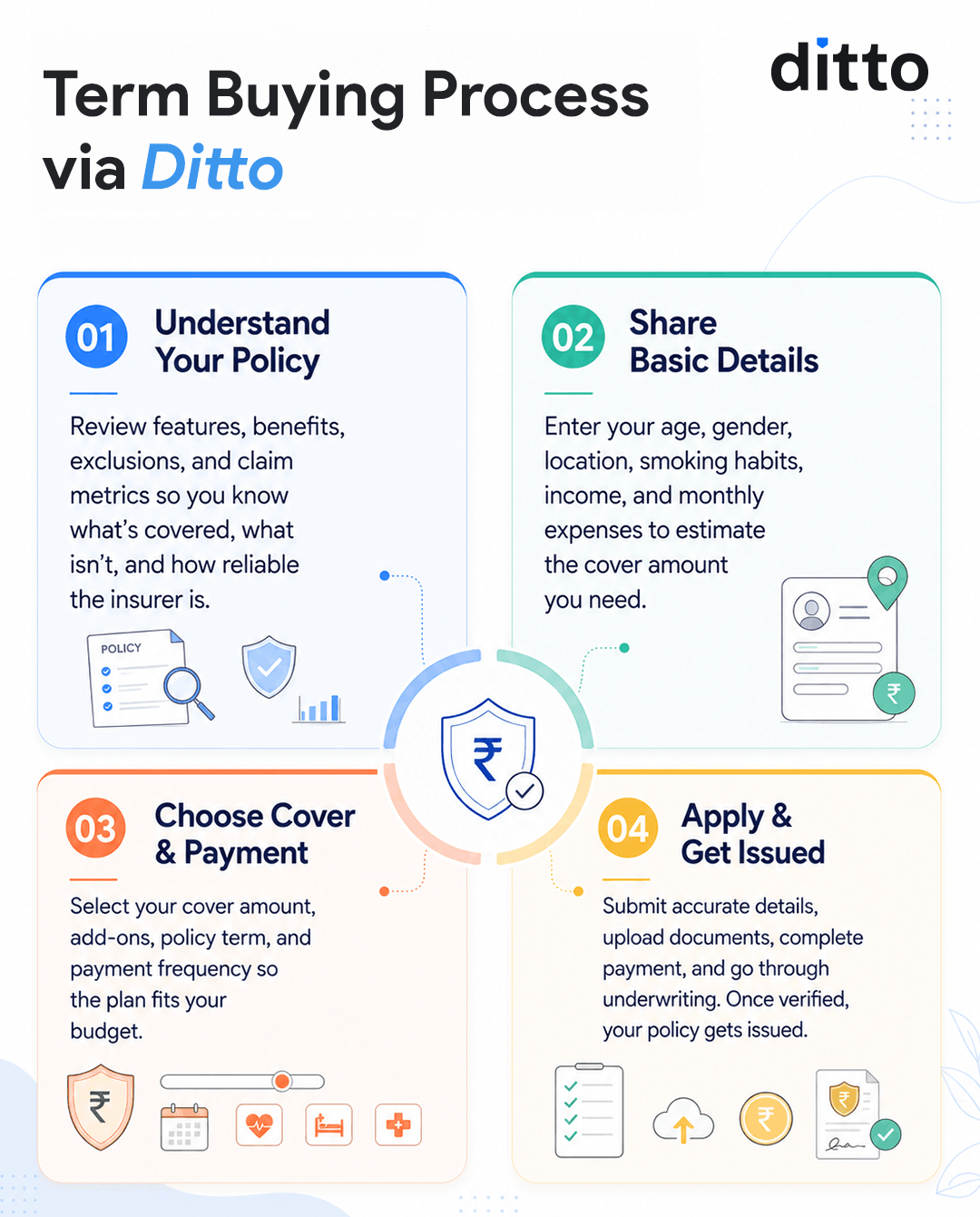

Take a look at the infographic below to have a clear picture of how the process works.

Did You Know?

Some offline Point of Sale (POS) term insurance versions may offer fewer features than regular online plans. For example, Axis Max Life Insurance Smart Secure Plus POS does not include optional benefits like premium break, voluntary top-up, or additional riders.

Point of Sales Person (POSP) products are designed for simpler and wider distribution across mass-market channels. Because of this, insurers may restrict certain riders or coverage features in POSP versions compared to regular online plans. Buyers should always compare the official brochure, Customer Information Sheet (CIS), Unique Identification Number (UIN), and benefit illustration carefully before assuming the POSP plan offers the same features as the insurer’s standard online product.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Insurers increasingly prefer online and digital channels because the process is faster and more efficient. Digital applications simplify policy issuance, document verification, updates, and future modifications. They also improve communication with customers through quicker alerts, easier tracking, and smoother servicing throughout the policy term.

For most buyers, online term insurance offers better value, lower premiums, and greater transparency. Online buying makes it easier to compare the best term insurance plans side by side without sales pressure or unnecessary add-ons. However, offline buying can still be useful for people with complex medical conditions, higher cover requirements, or income documentation issues who prefer personal guidance throughout the process.

Frequently Asked Questions

Is online term insurance cheaper than offline in India?

Yes, online term insurance is usually cheaper than offline plans because insurers save on agent commissions, branch expenses, and distribution costs. These savings are passed on through lower premiums. In many cases, the same insurer may offer noticeably lower premiums online for identical coverage and policy terms. Offline commissions on term plans can range between 5% and 10%, depending on the insurer and product structure. Online buying also makes premium comparison easier across insurers. At Ditto, we offer the same pricing available on insurer websites, pass on all online discounts, and provide advisory and claim support without any extra fee.

What is the difference between online and offline term insurance?

The main difference lies in the purchase process and who handles the proposal form. Online term insurance is purchased directly through an insurer's website or digital platform. Offline term insurance is purchased through an agent, advisor, or branch representative who assists with documentation and application formalities. According to IRDAI data, online direct sales contributed only 0.87% of individual life insurance new business premiums in FY25, though adoption continues to rise steadily. Once the policy is issued, insurers provide the same claim settlement process, servicing standards, and customer support regardless of whether the plan was purchased online or offline.

Does buying term insurance online or offline affect the claim settlement?

No. Insurers do not differentiate between online and offline customers during claim settlement. The documentation process, timelines, and claim assessment standards remain the same for both channels. What matters most is the accuracy and completeness of disclosures made while purchasing the policy. Important details such as smoking habits, alcohol consumption, medical history, occupation, income, and existing insurance policies must always be disclosed honestly. Incorrect or incomplete information can create serious claim rejections or complications later. At Ditto, we consistently emphasize that disclosure quality has a much bigger impact on claims than the purchase channel itself, whether online or offline.

What are the advantages of buying term insurance online?

Buying term insurance online gives buyers greater control, transparency, and convenience. You can compare term insurance plans, premiums, riders, payout options, and exclusions across multiple insurers without sales pressure. Since you fill out the proposal form yourself, the chances of incorrect disclosures reduce significantly. Online buying also allows instant access to policy documents, premium breakdowns, and benefit illustrations from home without branch visits. At Ditto, we combine online convenience with expert human guidance, so buyers receive both transparency and personalized support throughout the process.

Why do some people still prefer buying term insurance offline?

Many buyers still prefer offline term insurance because they value personal guidance during the purchase process. Advisors can help estimate the right cover amount and recommend suitable riders based on family needs. Buyers with medical conditions often feel more comfortable discussing disclosures with an expert to avoid mistakes that may affect future claims. Self-employed individuals and business owners may also need help arranging income proofs and underwriting documents. Offline support becomes especially useful for high-cover applications or complex financial profiles. At Ditto, we believe advisory support matters, which is why we combine expert guidance with a fully digital buying experience.

What happens if my term insurance proposal form has errors?

Errors in the proposal form can create serious problems during claim settlement, especially if they involve important disclosures like smoking status, medical history, occupation, income, or existing insurance policies. If mistakes are identified during the free-look period, insurers usually allow corrections. Even later, buyers can request amendments with supporting documents, though changes remain subject to underwriting approval. Under Section 45 of the Insurance Act, after 3 years from policy issuance, commencement of risk, revival, or rider date, whichever is later, insurers generally cannot question a life insurance policy except on grounds such as fraud.

Is it safe to buy term insurance online in India?

Yes, buying term insurance online in India is safe if you purchase through an insurer’s official website or a registered intermediary such as a licensed corporate agent. IRDAI regulates online insurance transactions and mandates strict compliance standards for customer protection and data security. Policy documents are issued digitally and remain accessible through insurer portals, which makes storage and nominee access easier. One major advantage of online buying is that buyers complete the proposal form themselves, reducing the risk of incorrect disclosures by intermediaries. At Ditto, we operate as a licensed corporate agent and follow all IRDAI regulations and compliance requirements.

What is mis-selling in term insurance, and how do I avoid it?

Mis-selling in term insurance happens when an agent provides incorrect or incomplete information about a plan's features, exclusions, or premium structure to close a sale. Common examples include promising returns in Return of Premium (ROP) plans, misrepresenting premium payment terms, and adding unnecessary riders. Buying online reduces this risk significantly because you research and compare plans yourself without sales pressure, and you fill in the proposal form in your own words. At Ditto, our advisors offer free, commission-blind advice, which removes the financial motive for mis-selling.

Is online term insurance better than offline term insurance?

Online term insurance is not automatically better, and offline term insurance is not automatically safer. The right choice depends on your comfort with disclosures, documentation, and policy understanding. Online plans usually cost less, offer easier comparison, and give you control over the proposal form. Offline buying can help self-employed individuals, NRIs, buyers with medical history, or those needing underwriting and documentation support. Claim settlement does not depend on the purchase channel. What matters most is accurate disclosure of income, health, smoking habits, and existing policies. A simple profile may work well online, while complex cases often benefit from advisor support.

Are offline term insurance policies still issued digitally?

Yes. Even offline term insurance policies are largely processed and issued digitally today. When you buy through an agent, corporate agent, or bank representative, the final policy document is still generated electronically, emailed to you, and often stored in an Electronic Insurance Account (eIA). Agents usually use digital portals or tablets to upload documents, submit proposal forms, and coordinate medical requirements. The underwriting, verification, and policy issuance process remains digital for both online and offline purchases. The real difference lies in the sales and advisory journey, not in how the insurer processes or issues the final policy.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.