Overview

Portability in insurance means you can switch your policy from one insurer to another without losing the benefits you’ve already built up. This is mainly available in health insurance (not term insurance), and it protects things like waiting and moratorium period credits, so there is no break in cover.

Now, let’s understand more about the nuances of term insurance portability and other IRDAI regulations that protect the interests of policyholders.

Can You Port a Term Insurance Policy in India?

No, term insurance portability in India is not possible. Term insurance also works differently from health insurance. There are no waiting periods to carry forward, no accumulated bonuses, and no continuity benefits of that nature.

Premiums are locked from a younger age, and moving to a new insurer would mean buying a fresh policy based on your current age, health, income, and underwriting profile. There is no shortcut around this.

Why Term Insurance Cannot Be Ported Like Health Insurance?

- No Regulatory Framework for Term Portability: IRDAI has clear guidelines for health insurance portability, but there is no framework for term insurance.

- Term Plans Have Fixed Premiums: You usually buy a term plan when you are young and healthy, and the insurer fixes a level premium for the entire policy term after analyzing the risks. There are no meaningful waiting periods or bonuses to carry forward if you “port” the plan.

- Pricing Issues: If you move to a new insurer later, especially at a higher age, the insurer would have to reassess your risk from scratch. This can significantly affect the premium you pay based on your age, health, and lifestyle habits.

What to Do If You Are Unhappy With Your Term Insurer?

Step 1: See Where You Are in the Policy Timeline

1) Within Free Look Period (30 Days)

- If the plan feels mis-sold or you simply don’t want it, cancel within the free look period.

- You’ll get your premium back after deducting stamp duty, risk premium for days covered, and medical costs (if any).

- If you catch the issue this early, exiting and choosing a better plan is usually the smartest move.

2) Within the First 1–2 Years

- Pure Term: If you stop paying, the policy lapses, and you don’t get anything back.

- Term Insurance With Return of Premium (TROP)/ Limited Pay: There may be a small surrender value after a minimum period, but in the early years, it’s usually not much. So your main loss is the premiums already paid.

Before switching, make sure to check if your health has changed since you bought the plan. This also involves considering if you will qualify for a new plan at a similar or reasonable premium. If health is good, switching is easier. If it has worsened, giving up your existing cover can be risky.

3) After 3+ Years

- You’ve already locked in a premium at a younger age.

- You’ve spent a few years inside the policy and fully covered the Section 45 provision, which makes the policy harder to question later.

At this stage, for many people, continuing the plan often makes more sense than trying to replace it.

Step 2: Know Your Practical Options

1) Buy a New Policy First, Then Tweak the Old One

- Apply for a new term plan that actually fits your needs today.

- Complete medicals and underwriting, and wait till the new policy is issued and active.

- Once that’s done, you can consider reducing the old cover or letting the old policy expire.

This way, you’re never left without cover if the new insurer rejects you, increases the premium sharply, or adds restrictions around cover amount, tenure, or riders.

2) Use Reduced Paid-Up (RPU) in Some TROP Plans

In some TROP policies, you can stop paying premiums and convert to a reduced paid-up. The policy continues with a lower sum assured, in proportion to the premiums already paid. Here’s an illustrative example:

- The sum assured is ₹2 crore, with ₹8 lakh paid over 20 years as the total premium.

- You’ve paid ₹4 lakh (50%).

- New sum assured = ₹1 crore (about 50%).

3) Surrender the Policy

Some products, like limited pay, TROP, or zero-cost term plans, allow you to surrender during specific ages or years. You can get back the base premiums minus the rider costs, depending on the product rules.

The exact surrender value is shown in your benefit illustration. Always check this before deciding.

Risks of Canceling Your Current Term Policy

Your Health May Have Changed

A new insurer will assess your health as it is today. If you have developed diabetes, hypertension, heart issues, or any other medical condition since then, they may charge a higher premium, add restrictions, or even reject your application.

Your New Premium Will Be Higher

Term insurance premiums increase with age. Even if a new plan looks cheaper at first glance, the final premium may be higher because you are now older than when you bought your existing policy.

You May Lose the Protection of Section 45

If your current policy has completed 3 years, the insurer has limited grounds to question or reject a claim under Section 45 of the Insurance Act. But when you buy a new policy, this 3-year protection period starts all over again.

You May End Up With No Cover

If you cancel your existing term plan before the new one is issued, you risk being uninsured. If the new insurer delays, charges extra, or rejects your application, your family may be left without protection.

How to Safely Buy a New Term Policy While Keeping the Old One

- Do Not Leave a Coverage Gap: Cancel, reduce, or stop paying for the old plan only after the new policy is in force.

- You Can Hold Multiple Term Plans: You can keep multiple term plans, as long as your total cover is justified by your income, liabilities, and financial responsibilities.

- Disclose Existing Policies Honestly: Always mention your existing policies and share income proof to avoid issues during underwriting or at the time of claim.

Common Mistakes to Avoid When Switching Term Insurers

- Do Not Switch Only for a Lower Premium: Compare the insurer’s claim record, policy features, exclusions, riders, flexibility, and overall value before switching.

- Do Not Ignore Policy Features: A new policy should offer better benefits, higher suitability, or clearer terms, not just a lower premium.

- Do Not Switch Without Understanding the Real Problem: Speak to your insurer or a Ditto advisor first to see if the concern regarding a feature, premium, or claim can be resolved without disturbing your coverage.

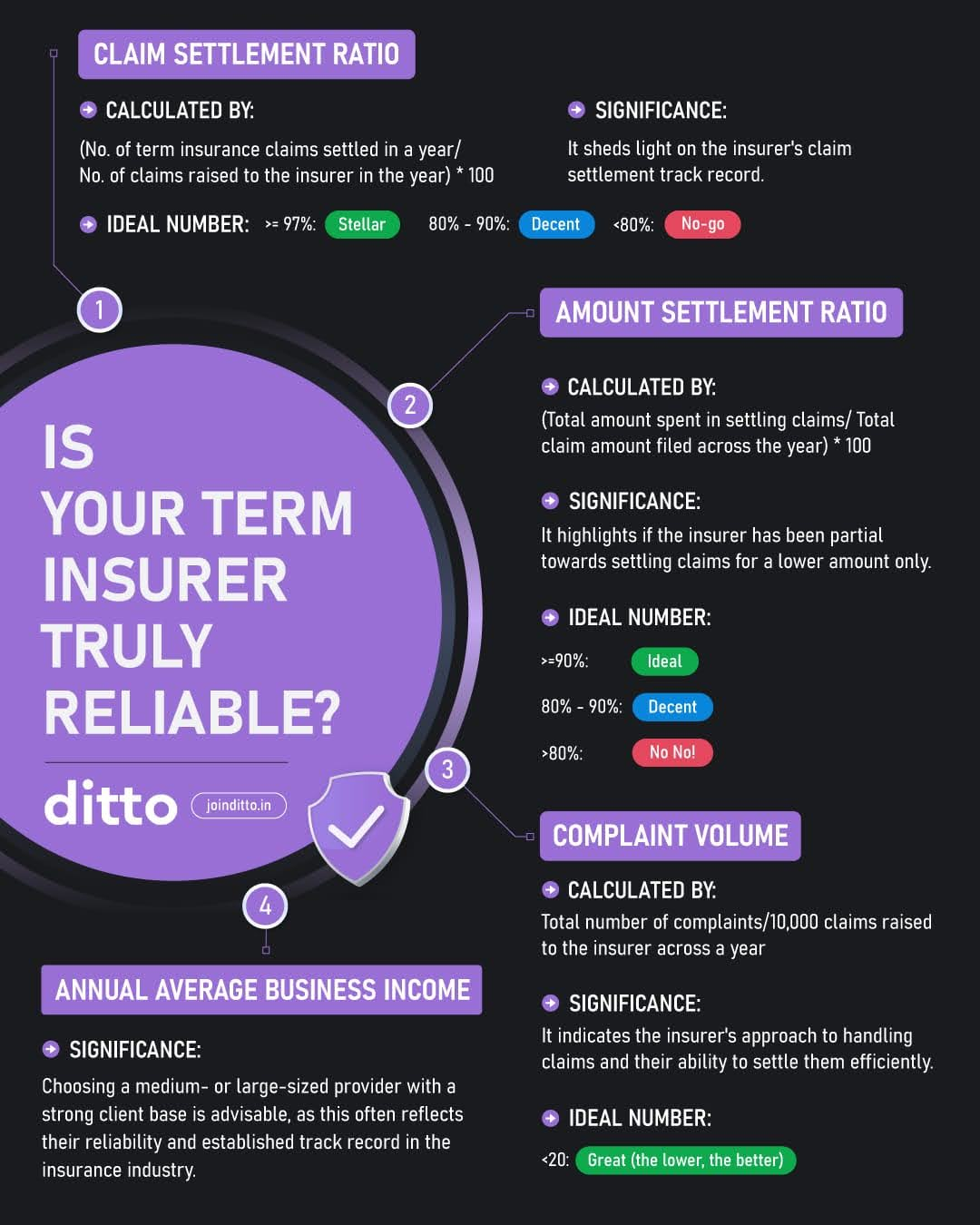

- Do Not Rely on Brand Size Alone: Look at the metrics like Claim Settlement Ratio (CSR), Amount Settlement Ratio (ASR), complaint volume, and overall service experience before making a decision.

Take a look at the infographic below to learn more about the performance metrics that help you understand if a term insurer is reliable enough.

Did You Know?

Why Choose Ditto for Term Insurance?

At Ditto, we have assisted over 8,00,000 customers with choosing the right insurance policy. Here is why customers like Vijay love us:

- No-Spam and No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Not sure whether to keep, supplement, or replace your existing term plan? Book a free call or chat on WhatsApp with Ditto’s advisors. Slots fill up fast!

Conclusion

Our simple view is that most people are better off keeping their existing term plan and adding more cover if needed.

You can always check how much life cover you really need using our term cover calculator. Then, apply for any new plan and wait for it to be issued and get active.

Later, you can easily think about reducing or canceling the old policy. Remember, once you lose a well-priced old plan, you may not get the same benefits again, especially if your health has changed.

If you are still unsure what to do with your current policy, speak to a Ditto advisor for free and get a simple keep, add, or change recommendation tailored to your income, loans, and family responsibilities.

Frequently Asked Questions

Last updated on: