Overview

Most term insurance plans focus only on providing basic life cover. However, some buyers also prefer features such as return of premium benefits, whole life coverage, or optional critical illness protection instead of choosing a pure protection-only policy. And that’s where traditional protection plans with savings-oriented features continue to attract attention despite the growing popularity of low-cost pure term insurance plans.

Bajaj Life Smart Protection Goal is one such plan. It combines basic life insurance protection with optional Return of Premium, optional Critical Illness Benefit, and whole life tenure. The plan also supports limited and regular premium payment options.

In this guide, we explain the plan’s features, premium illustrations, discounts, optional riders, insurer metrics, and whether it is still worth considering in 2026.

Key Features Of Bajaj Life Smart Protection Goal

1) Flexible Premium Payment Options: The Bajaj Life Smart Protection Goal supports Limited Premium (LP) and Regular Premium (RP) payment options. Policyholders can choose to pay premiums monthly, quarterly, half-yearly, or yearly. The premium payment frequency can also be changed on policy anniversaries, subject to the insurer’s applicable conditions.

2) Whole Life Coverage Up To 99 Years: Policyholders can opt for whole life coverage up to age 99. This option is available only with the Limited Premium payment structure. It is not available with regular premium payment. Also, if Whole Life is chosen, the Return of Premium option cannot be selected.

3) Return of Premium (ROP) Option: The plan offers an optional Return of Premium feature. If the policyholder survives till maturity and no death claim has been made, the policyholder receives the total premiums paid as a one-time lump sum at maturity. If the policyholder has also opted for the Critical Illness Benefit, the return of premium can also apply to the premiums paid toward the Critical Illness Benefit, subject to policy conditions.

4) Life Cover: The core benefit of Bajaj Life Smart Protection Goal is life cover. If the life assured dies during the policy term, the nominee receives the sum assured chosen at inception, and the policy terminates. If Return of Premium is not chosen, there is no maturity benefit on survival.

5) Optional Riders: The Bajaj Life Smart Protection Goal offers an optional Critical Illness Benefit (CIB) rider covering 55 illnesses, including 19 minor and 36 major conditions. Minor critical illnesses generally pay 25% of the CIB Sum Assured, while major illnesses pay the remaining balance up to 100% of the total CIB cover. The rider allows up to four minor critical illness claims during the policy term. It also comes with a 180-day waiting period and a 14-day survival period.

6) Rebates: The Bajaj Life Smart Protection Goal offers multiple discounts and premium rebates depending on the buyer profile and purchase mode.

7) In-built Health Management Services: The Bajaj Life Smart Protection Goal also includes built-in Health Management Services through registered service providers. These services include medical second opinions, medical consultations, and medical case management support. The objective is to help policyholders receive accurate diagnosis guidance and access appropriate treatment and illness care when dealing with serious medical conditions.

8) Tax Benefits: Premiums paid toward the base policy may qualify for deductions under Section 80C of the Income Tax Act. Premiums paid toward the Critical Illness Benefit rider may qualify under Section 80D under the old tax regime. Death benefits, surrender values, and return of premium payouts may qualify for tax exemptions under Section 10(10D), subject to prevailing tax laws.

Eligibility Conditions (Life Cover Eligibility)

Sample Premiums Of Bajaj Life Smart Protection Goal

Note: The above premium illustrations are taken from the official Bajaj Life Smart Protection Goal brochure.

Bajaj Life Insurance: Performance Metrics

Note: The above metrics are sourced from Bajaj Life’s public disclosures and IRDAI annual reports and are for the insurer as a whole.

Key Insights:

- The insurer shows strong claim settlement performance, fairly ahead of the industry, which reflects reliability in honoring claims.

- ASR is slightly below the industry average, but comfortably above the recommended 90%+ benchmark. This suggests Bajaj Life handles both high-value and low-value claims in a broadly fair and balanced manner.

- Complaint levels are significantly lower than the industry average, indicating a better customer experience and smoother service.

- Very strong solvency position and above-average business scale, which highlights financial stability and long-term strength as an insurer.

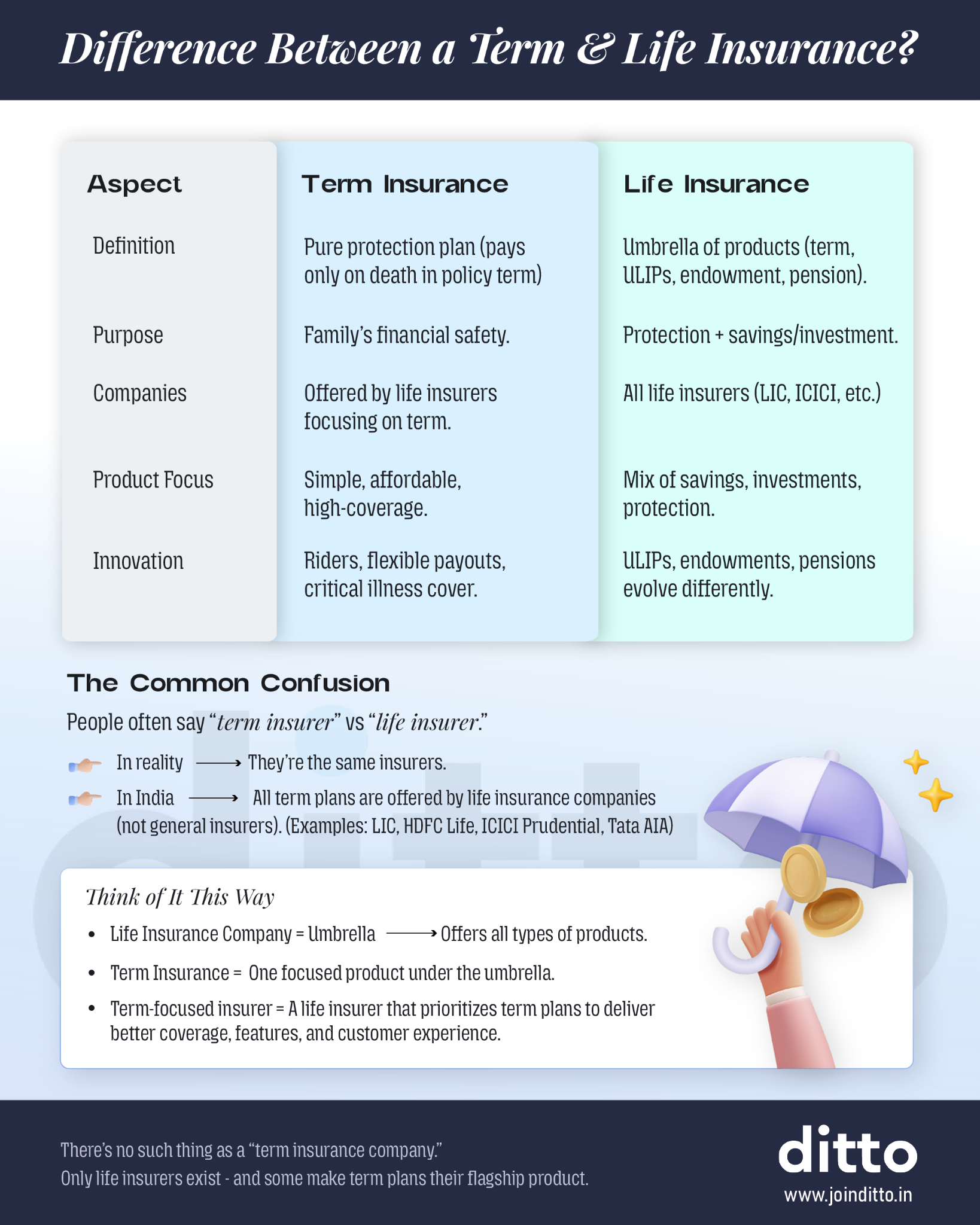

Term Insurance vs. Life Insurance: Which Is Better?

Check the infographic below to see why many people prefer buying term insurance and investing separately.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Ditto’s Take

The Bajaj Life Smart Protection Goal is suitable for buyers looking for a traditional term insurance plan with optional Return of Premium (ROP), Critical Illness Benefit (CIB), health management services, and whole life coverage up to age 99. Compared to the older Bajaj Life Smart Protect Goal structure, the current version is simpler and focuses mainly on core protection.

Its strengths include whole life coverage, critical illness protection, policy loan availability under eligible ROP variants, and multiple premium discounts. However, it misses several modern features now available in newer term plans like Bajaj Life eTouch II, including the Zero Cost Option, Terminal Illness Benefit, Top-Up Option, Waiver of Premium, inflation-linked cover increase, Insta Payout Benefit, and Cover Continuance Benefit.

The ROP option also significantly increases premiums compared to standard term insurance. For buyers seeking maximum coverage and modern protection features at a lower cost, plans like Bajaj Life eTouch II may be more efficient. If you are looking for reliable long-term coverage, explore our recommendations for the best term insurance companies in 2026.

Frequently Asked Questions

Last updated on: