A term insurance is possible with a ₹25,000 monthly salary, as long as you meet underwriting checks. There is no separate ₹25K salary term insurance category and insurers underwrite you for a standard term plan based on risk profile. A realistic cover range usually falls between ₹50 lakh and ₹75 lakh.

The smarter move is to take the highest cover you can while you are young, since premiums stay fixed. For example, a 25-year-old male may get ₹50 lakh cover for about ₹7,000 a year. Ditto’s top pick is Axis Max Life Smart Term Plan Plus, as it offers strong flexibility, and the insurer has a claim settlement ratio of 99.62% (average FY 2022-25). This guide walks you through affordable term plans with ₹25k per month salary.

India continues to remain significantly underinsured, with average annual life insurance spend at just $72 compared to the global average of $388, as per the IRDAI 2024–25 report. This gap highlights how many households still lack adequate financial protection, especially among lower-income earners with dependents.

For someone earning ₹25,000 per month, term insurance becomes a practical way to build a safety net against income loss. This guide focuses on whether protection is possible at this income level, what cover range is realistic, and how to choose affordable term insurance wisely.

Yes. If you earn ₹25,000 a month, you can get a term insurance plan. Insurers usually review your age, income, health, and the cover amount you request.

However, the sum assured offered by the insurer may come with limits. In many cases, insurers may cap the maximum available cover at around ₹50 to 75 lakh, which depends on your income and underwriting profile.

For more details on factors that affect term eligibility, please refer to our guide on Term Insurance Eligibility.

How Much Cover Is Right for You?

At a ₹25,000 monthly salary, it often makes sense to take the maximum term cover the insurer offers you and lock in lower premiums while you are younger. With many insurers, this may be around ₹50 lakh, while some may offer up to ₹75 lakh.

The premium difference between ₹40 lakh, ₹50 lakh, and ₹75 lakh is often modest. In some cases, a ₹25 lakh cover can even be priced higher than ₹50 lakh because of product pricing slabs.

At Ditto, we use the expense and liabilities replacement method to estimate suitable coverage. The common industry rule for the required term cover is 10-15x of your annual salary. However, for a personalized decision, use our cover calculator to find an ideal cover for you. In situations where you wish for a higher sum assured, like ₹1 crore, it is advised to take the maximum possible cover offered and increase it later.

Did You Know?

According to the State of Inequality in India (2022) report by the Institute for Competitiveness, a monthly income of around ₹25,000 places individuals among the top 10% of wage earners in India.

Best Affordable Term Plans for Low-Income Earners

If you earn around ₹25,000 a month, the right plan should offer low premiums, a reliable claim record, and cover you can comfortably maintain for years. Instead of paying for extra features, focus on simple protection from trusted insurers. Most of the best term insurance plans for this income group are regular pure-term policies with flexible cover choices.

Many insurers look for a minimum annual income of around ₹2.5 lakh to ₹3 lakh before offering term cover. In several cases, being a graduate can also improve eligibility, though actual approval depends on each insurer’s underwriting rules.

Premiums Across Ages and Plans

Age

HDFC Life Click2Protect Supreme Plus

Axis Life Max Smart Term Plan Plus

ICICI iProtect Smart Plus

25 (Male)

₹7,372

₹6,925

₹6,667

25 (Female)

₹6,266

₹5,887

₹5,667

30(Male)

₹9,714

₹8,477

₹8,221

30 (Female)

₹8,258

₹7,206

₹6,987

Note: The listed premiums are based on non-smoker profiles residing in Delhi, with a ₹50 lakh sum assured (coverage up to age 65, and no first-year discount). These figures are illustrative, and actual premiums depend on insurer underwriting.

If you have a tight budget, you can pay for your term plan on a monthly/quarterly basis, though it becomes about 2-4% more expensive than the annual payment mode. This is due to higher collection and servicing costs in monthly modes.

CTA

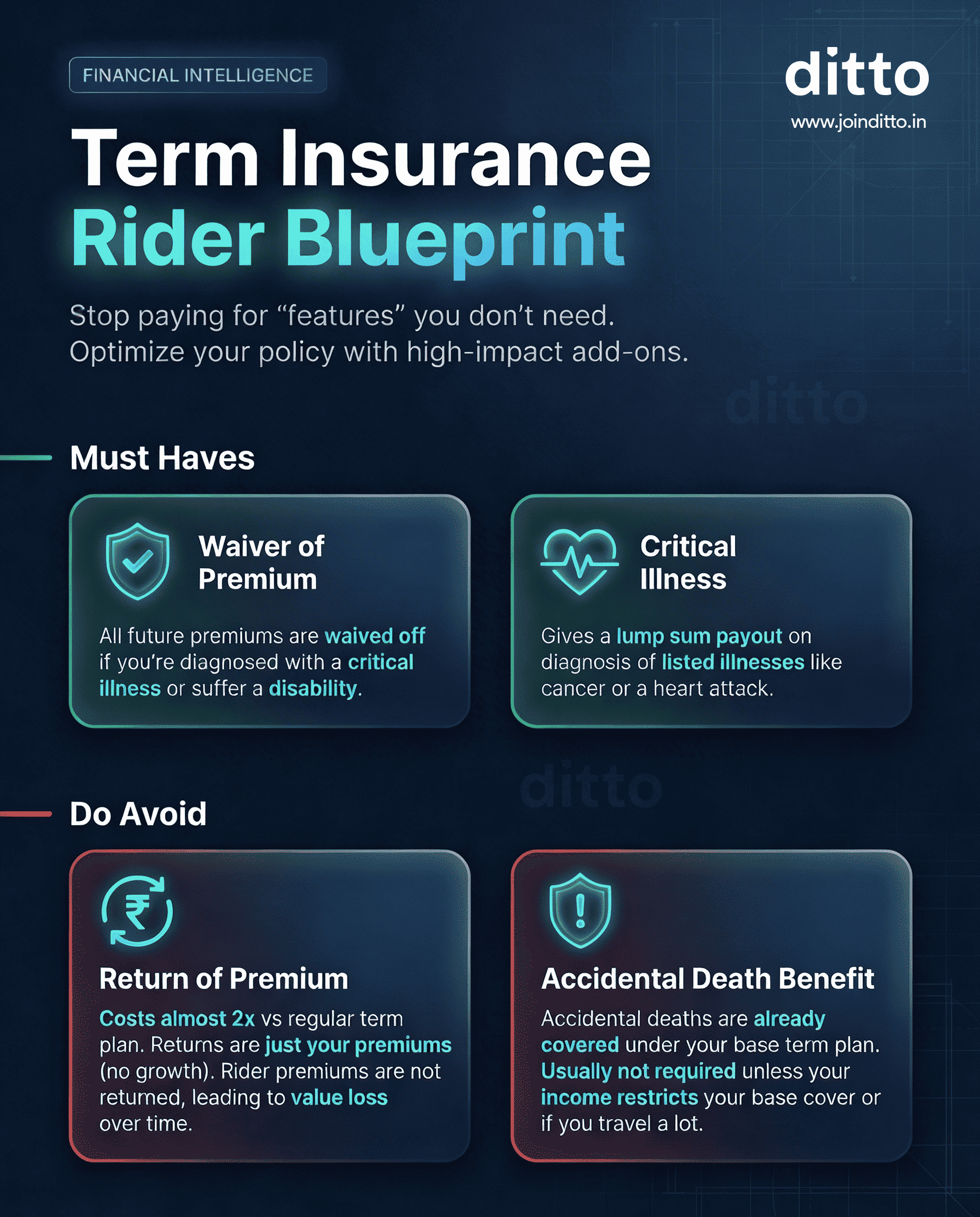

Tips to Maximize Coverage on a Tight Budget

01

Start with a Simple Term Plan

Begin with plain level-cover term insurance that focuses only on life cover. Avoid return of premium variants as they cost more and can put pressure on a limited budget.

02

Be Honest on Every Detail

Share accurate information about your income, health, smoking habits, and existing policies. Honest disclosures reduce future claim issues and help the insurer assess your application correctly.

03

Buy Now and Improve Later

A smaller policy today is usually better than waiting for the perfect cover amount. As your income grows, you can review your needs and increase protection later through an additional plan if needed.

04

Pick a Premium You Can Sustain

Do not choose cover only because the number sounds impressive. The better choice is a premium you can comfortably pay for many years without financial stress.

05

Protect the Essentials First

If money is tight, focus on giving your family solid life cover first. Instead of adding too many riders, it is often smarter to keep term insurance simple.

See the infographic for an understanding of which add-ons are useful and which to avoid.

Take Note: If you do not qualify for your desired insurer’s flagship term plans due to income or documentation issues, consider Saral Jeevan Bima. It may cost slightly more, but underwriting can be more flexible, and every insurer must offer it under IRDAI rules.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Term insurance on a ₹25,000 monthly salary can make sense if chosen wisely. Focus on a simple plan with affordable premiums. When you buy a term plan at a young age, you secure several long-term benefits. You lock in lower premiums that stay fixed for the entire policy term and improve your chances of approval since younger applicants usually have fewer health risks.

In addition, affordable coverage helps you manage your finances better by freeing up more money for savings and investments over time. The practical approach is to start with the cover you currently qualify for and secure protection early. As your income and responsibilities grow, you can increase coverage through the same plan, if allowed, or add another term policy later.

Frequently Asked Questions

Is 25000 per month term insurance good?

Yes, a ₹25,000 monthly income can still be enough for term insurance. What matters most is choosing a cover amount and premium you can comfortably maintain, while considering your family's needs, debts, and future responsibilities.

Many insurers consider annual incomes of around ₹2.5 lakh to ₹3 lakh for eligibility, so this salary range often qualifies. For younger buyers, a ₹50 lakh cover may cost roughly ₹6,000 to ₹7,000 a year, depending on age, health, and insurer.

How much salary is required for term insurance?

The minimum salary for term insurance plans is ₹2.5 to ₹3 lakh per annum, but specifics vary from one insurer to another. Insurers look at several factors, which include your income, age, job type, health, and the cover amount you request.

Even modest earners can purchase a term plan if the premium is affordable and the documents are complete. For younger applicants, a ₹50 lakh term plan may often cost under ₹1,000 a month, depending on the insurer you choose.

What is the monthly premium for a ₹50 lakh term plan if I earn ₹25,000 per month?

Premium costs vary by age, health, and insurer. For a 25-year-old, non-smoker male (residing in Delhi), the monthly premiums for a ₹50 lakh term insurance cover usually range around ₹550 to ₹800 for leading insurers like HDFC Life, ICICI Prudential, and Axis Max Life.

This means life cover can often cost less than many everyday monthly expenses. If you buy at a younger age, premiums are generally lower and remain fixed for the policy term, which makes early purchase a smart move.

Can someone earning ₹25,000 a month actually get term insurance in India?

Yes, you can get term insurance on a ₹25,000 monthly salary. There is no universal IRDAI rule that bars low-income earners from buying a term insurance plan. Most insurers will ask for salary slips or bank statements to verify your income level and determine how much term cover you qualify for.

As long as the documents you provide are in order and you meet the age and health requirements, you can apply for a standard term insurance plan.

How much term insurance cover do I need on a ₹25,000 salary?

A practical coverage range for someone earning ₹25,000 a month is ₹30 lakh to ₹75 lakh, depending on your age, dependents, and liabilities. A common method is the expense and liabilities replacement approach, which estimates what your family would need to cover living costs and outstanding loans in your absence.

If you are in your early 20s with limited financial responsibilities, even ₹25 lakh to ₹40 lakh can be a practical starting point. However, this is also the best stage to take the maximum cover you can comfortably qualify for, as premiums are lower at a younger age.

What documents do I need to buy term insurance on a low salary?

Insurers usually ask for proof of identity (Aadhaar, PAN), proof of address, and proof of income such as recent salary slips or bank statements. Some insurers also consider your educational qualification, and being a graduate improves term coverage eligibility.

For self-employed individuals, income tax returns are usually required instead of salary slips. The insurer uses these documents to confirm you can sustain premium payments for the policy you wish to purchase and to set an appropriate sum assured that avoids over-insurance.

Is there a minimum income required to get term insurance in India?

No. IRDAI does not have any mandated minimum income rule for term insurance. However, many private insurers informally require a minimum annual income of around ₹2.5 lakh to ₹3 lakh before approving standard term plans. This threshold exists to ensure you can maintain premium payments over the policy term and to prevent over-insurance.

This helps them assess whether you can comfortably continue premium payments through the policy term. It also helps prevent over-insurance, where the cover amount is far higher than your income profile.

What is Saral Jeevan Bima, and should I consider it on a ₹25,000 salary?

Saral Jeevan Bima is a standardized term insurance plan that IRDAI mandated all life insurers to offer from January 1, 2021. It provides cover between ₹5 lakh and ₹25 lakh (sometimes more) with no restrictions based on gender, occupation, education, or place of residence.

It is designed specifically for people who may not qualify for regular term plans due to income gaps or documentation challenges. The premiums are slightly higher than standard plans, but underwriting tends to be more flexible.

Should I buy a return premium term plan or a pure term plan on a tight budget?

On a ₹25,000 salary, a pure term plan is always the better choice. Return of premium (ROP) plans typically cost two to three times more than a comparable pure term policy for the same sum assured. That higher premium creates real budget pressure, especially when income is limited.

The smarter approach is to buy a pure term plan at a lower premium and direct the savings toward an investment like a mutual fund or PPF. A ₹50 lakh pure term plan for a 25-year-old can cost under ₹7,000 per year, money well spent on straightforward protection.

Which is the best term plan in India for someone earning ₹25,000 a month?

Ditto recommends Axis Max Life Smart Term Plan Plus as a top pick, partly because Axis Max Life posted a claim settlement ratio of 99.62% (Average of FY 2022-25). For low-income earners, the best term plan is one that balances affordable premiums, a strong claim settlement record, and reliable coverage.