Overview

Launched on 26 February 2008 and benchmarked against the NSE Nifty Midcap 100 Index, the Axis Max Life High Growth Fund is built for investors willing to embrace volatility in pursuit of long-term wealth creation.

In the next few minutes, you'll discover how the Axis Max Life High Growth Fund works, where it invests, how it has performed across market cycles, and the risks and charges involved.

What Is the Axis Max Life High Growth Fund?

The Axis Max Life High Growth Fund is not a standalone mutual fund you can purchase. Instead, it is a ULIP segregated fund available within select Axis Max Life ULIPs. This means your money is invested through a ULIP structure, where the fund's performance is linked to its daily Net Asset Value (NAV).

As with any market-linked investment, the fund value can rise or fall, depending on market conditions, and the investment risk is borne entirely by the policyholder. In simple terms, your returns depend on how the underlying fund performs, not on any guaranteed payout from the insurer.

Note: Not all ULIPs offered by Axis Max will offer this fund choice. The fund is currently available with plans like Max Life Fast Track Super. For more information, refer to the plan’s Fund Portfolio.

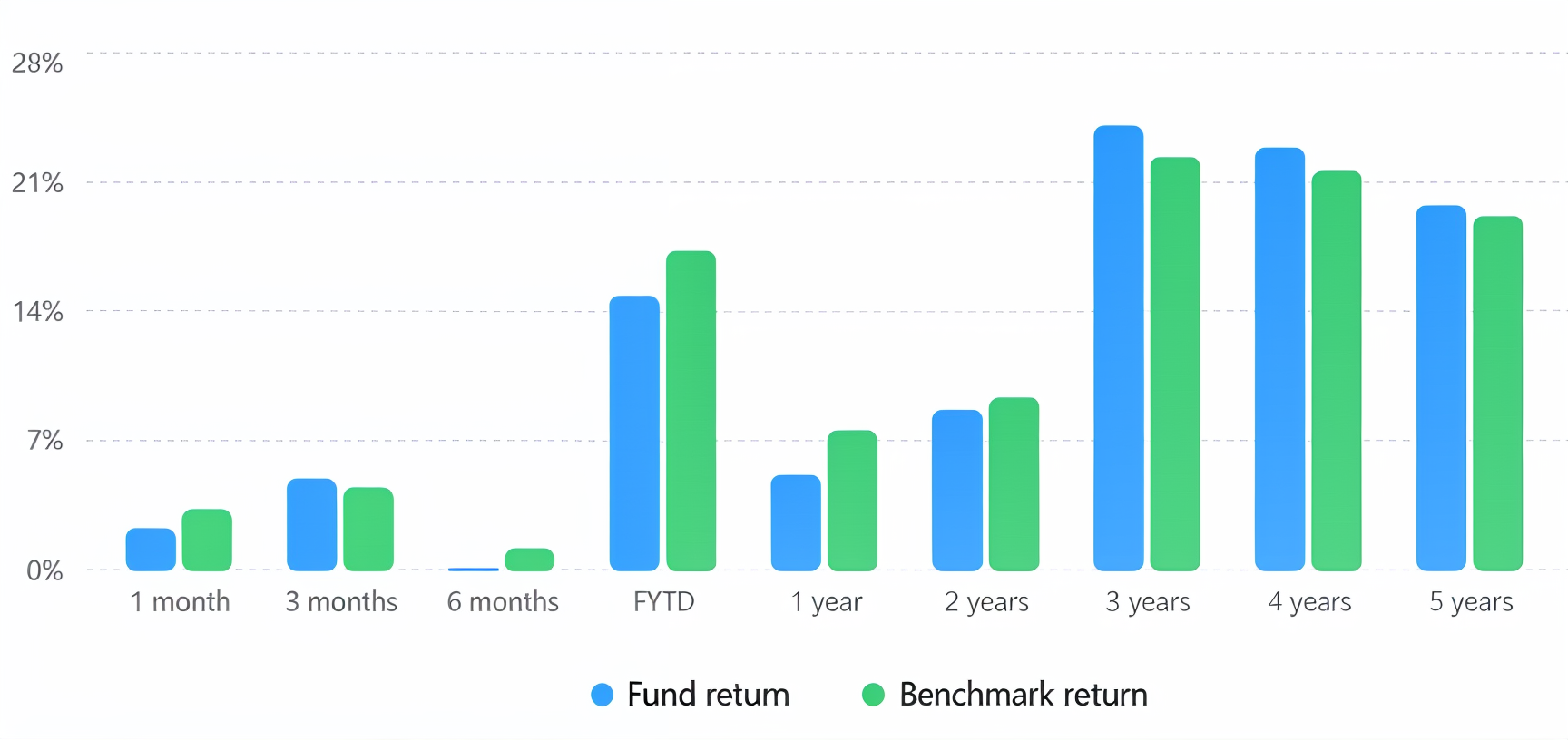

Latest NAV and Historical Performance

- Latest NAV: The Axis Max Life High Growth Fund NAV stood at ₹119.64 as of 29 May 2026. This reflects the price of a single unit of the fund under the plan.

- Strong Long-Term Track Record: Since its inception in February 2008, the fund has delivered a 14.55% CAGR, comfortably outperforming its benchmark's 10.14% CAGR.

- Consistent Medium-Term Outperformance: The fund has beaten its benchmark over the 3-year (24.01% vs 22.30%), 4-year (22.83% vs 21.55%), and 5-year (19.69% vs 19.09%) periods.

- Recent Performance Has Been Mixed: Over shorter horizons, the fund has lagged the benchmark, returning 5.10% over 1 year compared to the benchmark's 7.50%, highlighting the volatility typical of mid-cap investing.

- Growing Investor Participation: Assets Under Management (AUM) increased from ₹10,580 crore in August 2025 to ₹14,192 crore in May 2026, indicating rising investor interest.

The above data are derived from the monthly ULIP factsheet. Here’s a graphical representation of the funds' return over the last 5 years.

Note: The fund's strength lies in long-term wealth creation rather than short-term consistency. Investors should evaluate performance across full market cycles rather than focusing solely on recent returns.

Did You Know?

Portfolio, Allocation, and Risk Level

The Axis Max Life High Growth Fund is an aggressively managed equity-oriented ULIP fund that focuses on high-growth and mid-cap opportunities. As of 29 May 2026, the portfolio held 97.19% in equities and 2.81% in money-market instruments, reflecting an almost fully equity-driven strategy aimed at long-term capital appreciation.

The fund's mandate requires a minimum allocation of 70% to equities, with the balance permitted in government securities, corporate bonds, and money-market instruments.

However, the latest portfolio shows negligible debt exposure, highlighting the fund manager's strong conviction in equities and a clear preference for growth over capital preservation.

Top 5 Holdings

Key Insights

- The fund is actively managed rather than index-tracking, allowing the fund manager to make stock-specific bets across sectors such as financial-market infrastructure, healthcare, telecom, electricals, fintech, and automobiles.

- Portfolio diversification remains healthy, with the largest individual holding accounting for only about 4.19% of assets. This helps reduce the risk of excessive stock concentration while maintaining exposure to multiple growth opportunities.

- The fund can be high-risk due to its mid-cap orientation and near-total equity exposure. While this approach can deliver strong long-term returns, it also comes with higher volatility and sharper drawdowns.

Charges, Lock-In, and Surrender Rules

Using the High Growth Fund Calculator

- Use the Official Axis Max Life ULIP Calculator: The official Axis Max Life ULIP Calculator is the most relevant tool for prospective policyholders. It estimates potential maturity values based on your premium, policy term, and investment horizon, providing a more realistic picture of how a ULIP may perform within the insurance product structure.

- Use NAV Calculators for Fund Analysis Only: Third-party calculators like Moneycontrol returns calculator can be used as Axis Max Life High Growth Fund calculator, which are useful for tracking historical NAV growth and fund performance. However, they do not account for policy-level factors like mortality charges, premium payment terms, lock-ins, or ULIP-specific benefits, making them less suitable for estimating actual maturity proceeds.

Is Axis Max Life High Growth Fund ULIP Right for You?

- Suitable for investors with a high risk appetite who are comfortable with equity-market volatility and temporary declines in fund value.

- Can be a good fit if you want market-linked wealth creation within a life insurance wrapper rather than a standalone mutual fund.

However, it is not ideal for short-term goals, emergency funds, or money you may need access to within the next five years. Additionally, returns are not guaranteed and depend on market performance, fund management decisions, and the overall ULIP structure. For better returns and more efficiency, a term plan with separate investments in mutual funds can be considered.

Note: If your total annual ULIP premium remains within ₹2.5 lakh, the maturity proceeds can qualify for tax exemption under Section 10(10D), subject to prevailing tax rules. Once you receive the maturity corpus, you can move your investment from the aggressive High Growth Fund to a debt or liquid ULIP fund without triggering capital gains tax, allowing portfolio reallocation within the policy while maintaining tax efficiency.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Arun below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Conclusion

The Axis Max Life High Growth Fund can be a compelling option for investors seeking aggressive, equity-driven wealth creation within a ULIP and comfortable staying invested for the long term. Its strong historical performance, high equity allocation, and mid-cap growth orientation make it suitable for those seeking higher return potential and who can tolerate market volatility.

That said, a ULIP combines investments, insurance, charges, lock-ins, and policy rules into a single product. Investors who prefer simplicity, greater liquidity, and a clearer separation between protection and wealth creation may explore other options. A term insurance plan for life cover, plus mutual funds or fixed deposits for investing, is a more transparent and flexible approach.

If you prefer Axis Max, explore comprehensive options like Smart Term Plan Plus. The policy is one of the best term insurance plans in India, offering advanced features and affordable pricing.

Frequently Asked Questions

Last updated on: