Quick Overview

Having more than one health insurance policy can feel redundant. However, if you know how to make them work together, they can add an extra cushion of protection. Coordination of Benefits in health insurance explains exactly that: how multiple policies share costs so you get the most coverage without overlap. Let’s explore how COB works and why it matters for your health coverage strategy

What is Coordination of Benefits in Health Insurance?

Coordination of benefits in health insurance (COB) describes the rules and steps used when a person has more than one health policy and needs to use them together for a single hospitalization or treatment.

In India, IRDAI permits multiple health policies and gives policyholders the right to choose which policy to file a claim under. COB exists to make sure you are indemnified for actual healthcare expenses (you cannot profit from indemnity policies) while enabling you to use additional policies to cover gaps, co-payments, or amounts disallowed by the first insurer.

Key points:

- There is no legal limit on the number of policies you can own.

- Defined-benefit plans (hospital cash, critical illness, personal accident plans) pay fixed amounts and can stack on top of indemnity payouts.

- Indemnity policies reimburse actual medical costs; total combined indemnity payouts cannot exceed the real hospital bill.'

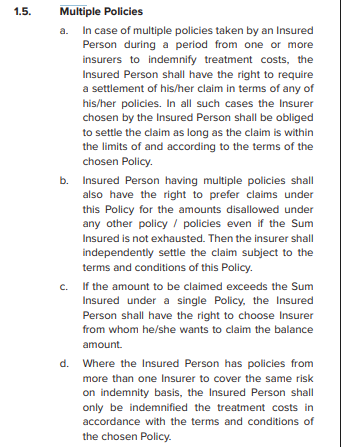

Note: The above screenshot illustrates how the guidelines on multiple policies appear in policy wordings.

How Does COB in Health Insurance Work?

Here’s an operational view of how coordination of benefits in health insurance works in practice, cashless and reimbursement routes, your rights, and the paperwork you need:

- You can choose which policy to file your claim under; this becomes your primary insurer for that claim. The chosen insurer is obligated to settle the admissible amount in accordance with the policy terms, as per the IRDAI Master Circular on Health Insurance Business (2024).

- Suppose the first insurer disallows certain items or limits, or has cost-sharing mechanisms such as co-payments in place. In that case, you can claim those disallowed amounts from another policy, provided it covers the same expenses.

- If a single policy’s sum insured is insufficient, you can claim the balance amount from other policies you hold.

- For indemnity-based covers, the combined payouts cannot exceed the actual hospitalization cost, ensuring fair reimbursement.These rights are reinforced under the IRDAI (Protection of Policyholders’ Interests and Allied Matters) Regulations, 2024, which emphasize transparency, consent, and fair treatment when holding or splitting multiple insurance policies.

Cashless Claims With Multiple Policies: A Step-by-Step Guide

- Inform a primary insurer and get cashless approval (if the hospital is in their network).

- The primary insurer settles up to its limit (cashless). Obtain the claim settlement summary or invoice copy.

- Submit the settlement summary + original hospital bills + other documents to your secondary insurer for reimbursement of the balance.

Example: Suppose your hospital bill is ₹6,00,000. Your corporate health policy settles ₹3,50,000 through cashless approval. You can submit the settlement summary and remaining bills to your personal (retail) insurer to claim the balance ₹2,50,000, subject to that policy’s terms and conditions.

Reimbursement Claims With Multiple Policies: A Step-by-Step Guide

- Notify all insurers within their specified timelines that you’ve been hospitalized.

- Pay the bill if cashless is not available.

- File for reimbursement with the insurer you choose first (submit original bills, discharge summary, reports).

- After the first insurer issues a settlement statement, submit that statement and the remaining documents to the next insurer to claim the balance.

Did You Know?

Important operational tips for coordinating multiple policies

- Always disclose other active policies if asked on the proposal form or during claim initiation. Non-disclosure can be considered a material misrepresentation and may lead to claim denial.

- Link follow-up (pre/post) claims to the same policy that paid for the hospitalization (otherwise, those post-hospitalization claims can be rejected).

- Prefer the same insurer for base and super top-up (for smoother cashless settlement). If they’re with different insurers, expect more complex reimbursement processes and additional documentation.

- Keep digital and physical copies of settlement summaries, hospital bills, and receipts.

Benefits of Coordination of Benefits in Health Insurance

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Conclusion

Coordination of benefits in health insurance is a powerful tool when used wisely. It helps you expand your effective coverage, fill gaps left by a single policy, and stack defined-benefit payouts for added security. However, it also introduces some process complexity, such as documentation, disclosure, and careful claim alignment, which are key.

The golden rules:

- Keep it purposeful; limit yourself to 2–3 policies unless you truly need more.

- Always disclose all existing covers when buying & when diagnosed with a new one, disclose it to your insurer immediately to avoid future claim hassles.

- Link hospitalization and follow-up claims to the same policy/claim ID for smoother processing.

- Prefer the same insurer for base + super top-up plans to simplify cashless coordination.

Follow these steps, and the coordination of benefits in health insurance becomes a strong pillar of safety, rather than a paperwork burden.

Frequently Asked Questions

Last updated on: