Quick Overview

Worried your health cover may fall short when medical costs rise? NCB solves this by increasing your sum insured(SI) for every claim-free year, giving you higher protection without increasing your premium.

However, with evolving health insurance products, the traditional NCB is becoming less relevant. Many modern plans now increase your coverage even if you make a claim, ensuring consistent protection without relying on claim-free years.

This guide explains no claim bonus in health insurance, how it works, its benefits, and what to check before choosing a plan that fits your needs.

What is No Claim Bonus in Health Insurance?

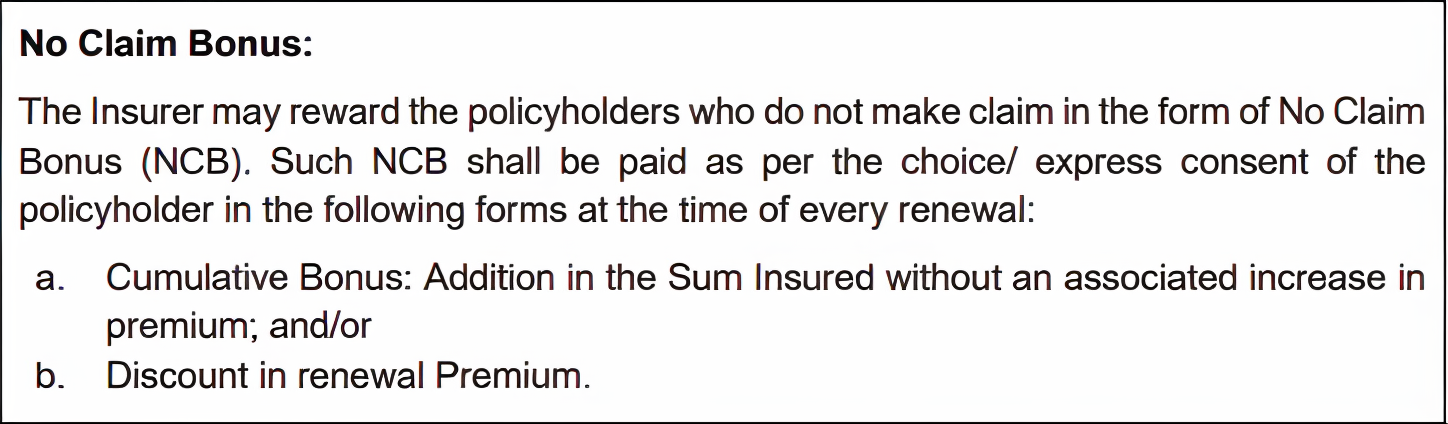

In case you do not make any claims in a policy year, insurers reward you with an increase in your sum insured or a discount in your renewal premium. If you opt to increase your SI, the bonus accumulates each year until it reaches a set limit, such as 100% or more of your base cover.

Here’s a snippet of how IRDAI classifies NCB:

How No Claim Bonus Works in Health Insurance Plans?

- If you don’t make a claim in the first year, you get a reward like a premium discount or a higher sum insured. Few plans, like United India Family Medicare, offer either a premium discount or an increase in your SI. You can opt for a 5% discount for the first five years and 2.5% thereafter, up to 50%. But if you select an increase in your SI, your coverage can grow by 20% initially and 10% later, up to 200% of the base sum insured.

- If you stay claim-free in the following years, this benefit continues and can keep increasing with each claim-free year.

Health Insurance Plans That Offer No Claim Bonus

Note: Policies that offer NCB follow a clawback rule where your bonus is reduced if you make a claim. The reduction is calculated on the base SI. For example, if your bonus grows by 20% each year, a claim can reduce it by 20% at renewal. However, any reduction applies only to the bonus component and will not impact your base sum insured.

Numerical Example

Note: The illustration assumes a base sum insured of ₹10 lakh with a 20% NCB (₹2 lakh) added each claim-free year. If a claim is made in Year 5, the accumulated bonus reduces by ₹5 lakh (50% of base SI), while the base cover remains unchanged.

Benefits of Choosing Health Insurance Plans With No Claim Bonus

- Stronger Financial Buffer: NCB increases your SI over time, building a larger safety net for rising healthcare costs and future medical needs.

- Boosts Cover at No Extra Cost: NCB increases your total sum insured without charging for the added cover.

- Portability and Migration Benefits: Your NCB can be transferred when switching insurers or plans. When you port your policy, this bonus can help reduce the waiting period on the additional cover in the new plan.

- Protection with Add-ons: NCB protection riders help retain your bonus even after a claim. Care Classic’s Care Shield add-on enhances coverage by adjusting the sum insured for inflation, covering consumables, and protecting your NCB even after claims. However, Care Shield protects your NCB only for low-value claims, specifically when the total claim paid stays below 25% of the base SI.

Real Example of How NCB Helped During a Claim

Things to Check Before Choosing a Health Plan With No Claim Bonus

Type of NCB

Maximum Bonus Limit

Reduction or Reset Rules

Loyalty Bonus vs NCB

Why Talk to Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- 100% Free Consultation

- Dedicated Claim Support Team

- Backed by Zerodha

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- No-Spam & No Salesmen

You can book a FREE consultation here. Slots are filling up quickly, so be sure to book a call now or chat on WhatsApp with us.

Conclusion

Choosing a health insurance plan with No Claim Bonus is a smart move and is especially helpful in family floater plans, where large medical bills can quickly deplete coverage. However, it should not replace a strong base cover. Start with at least ₹15 to ₹25 lakh to balance affordability and adequate protection.

An NCB is useful because it rewards you for staying claim-free. However, a benefit that grows your cover regardless of claims can be more reliable, as it ensures your protection continues to increase even when you need to use the policy.

If you’re comparing options from established insurers that offer a bonus irrespective of claims filed, start with our list of the best health insurance plans based on your medical needs.

Frequently Asked Questions

Last updated on: