Top-rated family health insurance plans in India combine high sum insured options, restoration benefits, and wellness rewards to guard against medical inflation. Based on Ditto's transparent policy rating framework, best picks for 2026 include-

HDFC Ergo Optima Secure+: "Secure Benefit" doubles your cover from day one, with in-built unlimited restoration and a 97.61% 3-year average claim settlement ratio (FY 2024-26).

Care Supreme: Unlimited automatic restoration, up to an unlimited bonus with an add-on, and wellness discounts.

Aditya Birla Activ One MAX: unlimited restoration and "HealthReturns" fitness rewards up to 100%.

Niva Bupa ReAssure 2.0 Platinum+: age-lock on premiums until first claim, and "Booster+" carry-forward.

SBI Super Health Platinum Infinite: unlimited reinstatement and a 3x "Health Multiplier".

Choosing the right plan means weighing benefits, premiums, insurer reliability, and the required sum insured based on your family structure and members' ages.

Think about the last time someone in your family needed a hospital visit. The bill didn't care if your savings were low or if it was your worst month financially. In India, out-of-pocket health spending still accounts for a significant share of total health expenditure, meaning most families absorb these shocks entirely on their own.

A family health insurance plan changes that. It creates a financial cushion so that one bad health year doesn't wipe out everything you've worked for.

But not all family plans are built equally. Some look great on paper and create unpleasant surprises at claim time.

In this guide, we break down the top 5 health insurance plans for family in India and show you how to pick a plan based on some key metrics.

Top 5 Health Insurance Plans for Family in India: Detailed Comparison

01

HDFC Ergo Optima Secure+

HDFC Ergo Optima Secure+ is a flagship health insurance plan of the insurer that offers sum insured options from ₹10 lakh up to ₹2 crore.

HDFC Ergo

Optima Secure+

4.6

Overall Rating

Premium Rating

3.0/5

Insurer Rating

5.0/5

Feature Rating

4.6/5

Customer Service Rating

5.0/5

Key Features:

Policy tenure for 1, 2, 3, 4, and 5 years.

Pre- and post-hospitalization expenses for up to 60 days and 180 days, respectively.

2x cover from day one (Secure Benefit).

In-built unlimited restoration.

Covers consumables (gloves, masks, syringes, and others under Protect Benefit).

Add-ons for pre-existing disease (PED) waiting period reduction, outpatient department (OPD) coverage (Optima Wellbeing), hospital cash, maternity, and unlimited coverage once or twice during the policy's lifetime.

Infinity Benefit adds 100% of the base sum insured every year at renewal, with no cap.

Takeaway: While premiums are higher than peers, the biggest strength here is insurer reliability: strong claims support, a dependable claims record (FY 2024-26 average CSR of 97.61%), and the basics done right.

02

Care Supreme

Care Supreme is a comprehensive, value-for-money health insurance plan for families, offering sum insured options from ₹5 lakh to ₹1 crore.

Care

Supreme

4.5

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.2/5

Feature Rating

4.5/5

Customer Service Rating

3.0/5

Key Features:

Policy tenure for 1, 2, or 3 years.

Unlimited automatic recharge for related and unrelated illnesses.

Cumulative bonus up to 100% (option to extend by 500% or unlimited accumulation additionally through add-ons).

Reduced out-of-pocket expenses by covering 146 non-payable items during hospitalization (Claim Shield Plus add-on).

Wellness discounts, with up to 30% off renewals based on the number of steps.

Add-ons for PED waiting period reduction, OPD cover, gym sessions, unlimited coverage (once), and air ambulance.

Takeaway: A fairly affordable plan for those with PEDs who want shorter waiting periods, as well as individuals looking for more flexibility through multiple add-ons.

03

Aditya Birla Activ One MAX

Aditya Birla Activ One MAX is a comprehensive health insurance plan that offers sum insured options for families, ranging from ₹5 lakh to ₹2 crore.

Aditya Birla

Activ One MAX

4.4

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.5/5

Feature Rating

4.3/5

Customer Service Rating

5.0/5

Key Features:

Policy tenure for 1, 2, or 3 years.

Unlimited restoration (for related and unrelated illnesses) from the second claim of the policy's lifetime.

Cumulative bonus of 100% per annum up to 500% given regardless of claims made (up to ₹3 crore).

HealthReturns rewards fitness and healthy living with discounts on renewal premiums up to 100%.

Add-ons for pre-existing disease waiting period reduction and chronic care.

Takeaway: A good fit for families looking for a feature-rich plan with modern benefits, affordable premiums, and strong service credentials.

04

Niva Bupa ReAssure 2.0 Platinum+

Niva Bupa ReAssure 2.0 Platinum+ offers comprehensive coverage with sum insured options up to ₹1 crore for families.

Niva Bupa

ReAssure 2.0 Platinum+

4.3

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.2/5

Feature Rating

4.2/5

Customer Service Rating

3.0/5

Key Features:

Policy tenure for 1, 2, or 3 years.

ReAssure+ to restore your cover an unlimited number of times in a policy year, up to the sum insured for each claim.

Age-lock on premium until the first claim (premiums may still increase due to medical inflation).

Unused sum insured to be carried forward up to 5x for the recommended Platinum+ variant (Booster+ Benefit).

Add-ons like Safeguard and Safeguard+ for non-payables and inflation-linked sum insured hikes (no impact on Booster+ if the claim made in a policy year is up to ₹50,000-₹1,00,000).

Takeaway: A plan worth considering for families seeking a flexible policy with innovative and modern features.

05

SBI Super Health Platinum Infinite

The SBI Super Health Platinum Infinite plan offers comprehensive, premium health insurance coverage for families, with sum insured options ranging from ₹50 lakh to ₹2 crore.

SBI

Super Health Platinum Infinite

4.1

Overall Rating

Premium Rating

5.0/5

Insurer Rating

3.2/5

Feature Rating

4.2/5

Customer Service Rating

3.0/5

Key Features:

Unlimited reinstatement of up to 200% of the sum insured per claim (ReInsure Benefit).

Up to 3x cover for 37 listed serious illnesses (Health Multiplier).

Global cover for 16 conditions and an air ambulance worth ₹10 lakh.

Built-in OPD and consumables cover.

Shorter waiting periods (2 years for PEDs and 1 year for specific illnesses).

Health assistance (personal fitness coaching), dietitian and nutrition e-consultation, and unlimited gym membership.

Renewal discount based on the number of steps walked by the insured members, up to 30%.

Takeaway: The policy is ideal for families seeking high health coverage with strong financial protection against major medical expenses.

Talk to an expert today and find the right insurance for you.

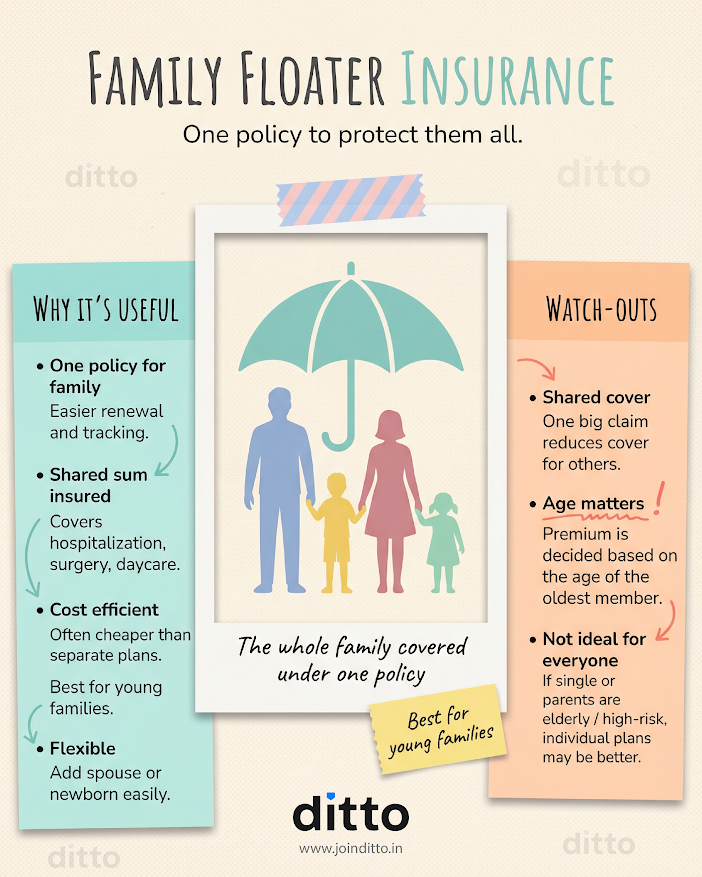

Family Floater vs Individual Health Insurance: Which is Better?

For most households, a family floater covering you, your spouse, and dependent children is the right starting point. Everyone shares one pool of coverage, and the premium is generally 40-50% lower than buying separate individual policies for each person. It's efficient, simple to manage, and easy to renew.

In short, a family floater makes sense if the age gap between you and your spouse is not significant and you are a fairly healthy family with medical needs that do not differ significantly.

Should Parents Be in the Same Floater?

Almost always, no. And here's why:

Floater premiums are calculated based on the age of the eldest person on the policy. If your parents are included, their age drives up the pricing for everyone, even if you and your spouse are in your 30s.

More importantly, parents tend to make more frequent claims, which can drain the shared pool and leave less coverage for your spouse and kids in the same policy year.

The cleaner approach: One floater for you, your spouse, and your children; a separate floater or individual policy for your parents. This keeps premiums predictable, covers separate, and claims from one group do not affect the other.

See the infographic below to learn how family floater insurance is beneficial in most cases, and other key considerations to keep in mind.

When an Individual Plan Makes More Sense

If one family member has a complicated medical history, underwriting for the entire group under a floater may become difficult.

If one person already has an existing policy and has accumulated several years of no-claim bonus on an individual plan, shifting them to a floater also means losing that benefit.

In some cases, certain members or relationships may not be eligible under a group floater structure at all, making individual policies the only practical option.

CSR: All five insurers have claim settlement ratios above 90%, indicating that most claims filed with them are successfully processed and settled.

Complaints: HDFC Ergo, Bajaj General, and Aditya Birla perform better on complaint figures, while Care and Niva Bupa are notably above the industry average, which may be a concern for some buyers. However, it is important to note that they are Standalone Health Insurers (SAHIs), which tend to receive more complaints than general insurers.

Network Hospitals: All five insurers cross Ditto’s 10,000+ network hospital benchmark, indicating a strong cashless hospital network.

Annual Business: Each of these leading health insurers reports a healthy annual business, indicating broader market presence and a larger policyholder base.

Note: Apart from these metrics, it is also worth looking at factors like network hospital size and incurred claim ratio (ICR) to get a more complete comparison of insurers. Refer to Ditto Data Labs to explore our proprietary repository of health insurance data, meticulously compiled, verified, and maintained by the Ditto team over the years.

Premium Comparison: Top 5 Health Insurance Plans for Family

Profile

HDFC Ergo Optima Secure+

Care Supreme

Aditya Birla Activ One MAX

Niva Bupa ReAssure 2.0 Platinum+

SBI Super Health Platinum Infinite

(Family Floater, 2A): Ages (31, 32)

₹₹21,128

₹21,528

₹16,299

₹19,176

₹61,568

(Family Floater, 2A 1C): Ages (35, 34, 5)

₹26,017

₹27,161

₹21,478

₹25,026

₹62,758

(Family Floater, 2A): Ages (62, 63)

Not available for senior citizens

₹78,923

₹66,505

₹68,239

₹1,13,250

Here, A stands for adult and C denotes children.

Note:

These are indicative premiums for a Delhi resident (pin code - 110010) with a ₹15 lakh sum insured, including mandatory and recommended add-ons. Your premiums can change based on city, age, medical history, plan variant, and chosen add-ons.

Premiums for SBI Super Health Platinum Infinite have been calculated by considering a sum insured of ₹50 lakhs.

For senior citizens, HDFC ERGO Optima Secure is a better option, as Optima Secure+ is currently not available beyond its maximum entry age limit of 60 years.

How to Choose the Best Health Insurance Plans for Family in India?

01

Decide the Structure First

Figure out who goes on which policy before you start comparing plans. The most common and recommended structure: one floater for you, your spouse, and children; separate coverage for parents. Getting this right saves you from buying a plan that isn't priced for your actual household.

02

Set a Realistic Sum Insured:

Don't just pick the lowest sum insured to keep premiums down. A single hospitalization at a tier-1 private hospital can easily run ₹4-8 lakh for a moderately serious condition. Medical inflation in India is running higher than general inflation. We recommend a base cover of at least ₹15-25 lakh for a young family, with unlimited restoration as a backup layer.

03

Prioritize "Clean" Plans

A plan that looks cheap but has room rent limits, co-pay clauses, or disease-wise sub-limits can cost you significantly more at claim time. These are not minor fine-print details. Room rent limits, for example, can trigger proportionate deductions across your entire hospital bill, not just the room cost. Always ask: Does this plan create any out-of-pocket costs for me at claim time?

04

Evaluate the Insurer, Not Just the Plan

Check CSR trends over 3-5 years, not just the latest year. Look up the insurer's hospital network in your specific city. Check how many complaints were filed with IRDAI against this insurer. A plan from a reliable insurer with a slightly smaller feature set is usually better than a feature-rich plan from an insurer with poor claim handling.

05

Add Riders Thoughtfully

Not every add-on is worth its cost. We recommend consumables coverage and add-ons to reduce waiting periods (for those with PEDs). Don't add riders just because they exist; add them because your family's specific situation calls for them.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat with us on WhatsApp now!

Conclusion

Choosing a family health insurance plan is one of the most important financial decisions you'll make. And yet, most people spend more time picking a phone than picking a health plan.

Here's what we want you to walk away with: The best plan for your family is one you never regret at claim time. It won't necessarily be the cheapest. It won't have the most features. It will be the one that pays cleanly, covers your family's specific structure correctly, and comes from an insurer you can trust when you're sitting in a hospital at midnight.

Our final advice?

Keep your parents on a separate policy.

Pick a plan without room rent limits or co-pays.

Don't rely on restoration as your primary safety net.

Talk to a trusted advisor like Ditto who understands the fine print.

Remember, your family's financial safety net is too important to be rushed.

Disclaimer

We believe in full transparency around our partnerships. Our current insurer partners are HDFC Ergo, Care, Aditya Birla, and Niva Bupa. But as you can see in this list, the rankings include both partners and non-partners because the methodology is unbiased and applied uniformly across all insurers. Always speak to an IRDAI-certified advisor to find out which plans best suit your needs.

Frequently Asked Questions

What is covered and not covered in family health insurance?

Coverage typically includes inpatient hospitalization expenses, pre-hospitalization and post-hospitalization expenses, and daycare expenses. Exclusions (cosmetic procedures, substance abuse, and experimental procedures) vary but often involve non-payable items or specific waiting periods for pre-existing diseases.

For example, the HDFC Ergo Optima Secure+ plan covers consumables like masks and gloves by default, which are often excluded in basic policies and may need add-ons. You must always check for sub-limits on room rents, as these can trigger proportionate deductions on your entire bill rather than just the room cost.

How to buy the best health insurance plans for family online?

First, decide on your family structure, as adding parents to a floater is usually discouraged because their age drives up premiums. Aim for a base cover of at least ₹15-25 lakh, especially since medical inflation is rising faster than general inflation in India.

Evaluate the insurer’s CSR and network hospital strength in your city rather than just the premium. Ensure you are not paying for unnecessary add-ons.

Is a family floater better than individual health insurance?

For most households, a family floater is the superior choice because it is 40-50% more cost-effective than buying separate individual policies for every person. Everyone shares a single pool of coverage, making it simpler to manage and track during renewals.

However, individual plans make more sense if a member has a complex medical history or if you want to protect their accumulated no-claim bonus. Family floater policies usually don’t allow members with large age gaps to be covered together.

They also restrict certain relationships, such as siblings, from being included under the same plan. The ideal approach is often a floater for you, your spouse, or your children, with separate coverage for your parents.

Should I include my parents in my family health insurance plan?

It is generally best to keep parents on a separate policy. The age of the oldest member determines floater premiums, so including parents significantly inflates the cost for everyone. Furthermore, parents often file more frequent claims, which can deplete the shared sum insured, leaving you with less coverage for your spouse and children in the same policy year.

By maintaining separate policies, you ensure premiums remain predictable for your younger family unit while guaranteeing that a claim from one group does not affect others.

What is a restoration benefit in health insurance?

The restoration benefit is a safety net that replenishes your sum insured if you exhaust it during the policy year. For instance, the Niva Bupa ReAssure 2.0 Platinum+ plan offers a "ReAssure+" feature that restores your cover an unlimited number of times for each claim in the same year. Similarly, the SBI Super Health Platinum Infinite plan provides unlimited reinstatement of up to 200% of the sum insured.

This means you don’t have to worry about running out of coverage after a major hospitalization. It is especially useful for families, where multiple members may need to claim in the same policy year.

Why are room rent limits a problem in health insurance?

Room rent limits are a major issue because they often trigger proportionate deductions. They reduce the payout for every single item on your hospital bill, not just the room itself. A plan that appears cheap but includes these sub-limits can leave you with substantial out-of-pocket costs at claim time.

When selecting a policy, it is much safer to prioritize plans that avoid these restrictive clauses. This ensures that your insurance actually covers the full cost of treatment without arbitrary financial constraints placed on your hospital stay.

How much sum insured do I need for my family?

You should avoid selecting the bare minimum sum insured just to save on premiums, as a single hospitalization at a tier-1 private hospital can easily cost between ₹4 lakh and ₹8 lakh for moderately serious conditions.

Given that medical inflation is outpacing general inflation, we recommend a base cover of at least ₹15-25 lakh for a young family. You should also have restoration benefits and a comprehensive bonus structure as a backup layer to protect your family's savings from being wiped out by a single health event.

What is the claim settlement ratio, and does it matter?

The claim settlement ratio indicates the percentage of claims an insurer successfully processes and pays out. It is a key metric for judging insurer reliability. For example, insurers for all the top 5 plans listed in our guide maintain a CSR above 90%.

While a high CSR is a positive signal, it shouldn't be the only factor you check. You should also examine the number of complaints received per 10,000 claims, annual business volume, and the size of the hospital network to get a comprehensive view of the insurer.

What are consumables in health insurance?

Consumables are non-medical items used during treatment, such as gloves, masks, and syringes, that were traditionally excluded from coverage. However, modern, high-quality plans like the HDFC Ergo Optima Secure+ and Aditya Birla Activ One MAX include inbuilt coverage for these items under the "Protect Benefit".

Paying out of pocket for these small items can add up to a significant expense (5-15% of the overall bill) during a long hospital stay. Selecting a policy that covers consumables reduces your out-of-pocket burden and ensures that your insurance provides a truly comprehensive safety net.

Do I really need add-ons or riders?

Add-ons should be purchased only if your family's specific situation requires them, not simply because they are available. Common add-ons include reducing the pre-existing disease waiting period or adding coverage for consumables. For example, if you frequent outpatient clinics, an OPD add-on might be beneficial, but it will increase your premium.

Avoid adding riders just for the sake of having them; focus on those that directly mitigate your specific risks to ensure you are paying for real claim protection rather than unnecessary features.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.