![Investment Plans for Girl Child in India [2026]](https://stat.joinditto.in/images/2026/07/Investment-Plan-for-Girl-Child-@2x.webp)

Overview

According to the Press Information Bureau (PIB), over 4.53 crore SSY accounts had been opened as of December 2025. This remarkable adoption shows why SSY remains one of India's most trusted savings schemes for securing a daughter's education and future financial goals.

In the next few minutes, you'll discover popular investment options for a girl child, compare returns and risks, and learn how to build a strong financial future with confidence.

Popular Investment Plans for a Girl Child in India

Note: Investing in gold, silver, and child education plans can complement a girl's financial plan, but they are usually best used as supporting investments rather than as the primary vehicle for funding long-term goals such as higher education or marriage.

If you wish to explore plans from established insurers, refer to our guide on SBI Life Insurance Child Plan and ICICI Prudential Child Insurance.

Why Plan Early for Your Daughter's Future?

- Starting early gives your investments more time to grow through compounding, allowing smaller monthly contributions to build a much larger corpus.

- A longer investment horizon lets you combine safe options like SSY with growth-oriented investments such as mutual funds.

- Shorter timelines often force parents to rely on lower-return options such as FDs, debt funds, or fixed-income products.

- Education costs rise faster than general inflation, so your savings must grow fast enough to keep pace, not just remain safe.

Example: If your daughter is 2 years old and you are saving for college at 18, you have 16 years to combine growth-oriented investments, such as mutual funds, with safer options, such as SSY. But if you begin when she is 13 or 14, your investment horizon shrinks to just 4–5 years, leaving far less room to take market risk.

Sukanya Samriddhi Yojana: Returns and Rules

- Number of Accounts: Only one SSY account per girl child is allowed.

- Family Limit: A maximum of two girl children is covered, with exceptions for twins or triplets.

- Where to Open: Available at India Post, public sector banks, and authorized private banks.

- Contribution Period: Deposits are required for only 15 years from the account opening date.

- Maturity: The account matures 21 years after opening.

- Partial Withdrawal: Permitted for higher education, subject to scheme conditions.

- Tax Benefits: Enjoys EEE status: eligible for deduction, tax-free interest, and tax-free maturity, subject to prevailing tax rules.

Note: A parent or legal guardian can open an SSY account for a girl child under 10 years old. At the current 8.2% annual interest rate, investing ₹1.5 lakh annually for 15 years could yield a maturity corpus of ₹66-₹72 lakh after 21 years, depending on the timing of each deposit.

LIC Plans for Girl Child Compared

- LIC Amritbaal: It is a non-participating, non-linked child savings plan. LIC Amritbaal is best suited for parents who want to build a guaranteed corpus for their child's future without taking market risk. The plan provides guaranteed additions of ₹80 for every ₹1,000 of basic sum assured throughout the policy term.

- LIC Jeevan Tarun: It is a participating, non-linked child insurance plan.LIC Jeevan Tarun is suitable for parents seeking financial support for their child's higher education.

- LIC New Children's Money Back Plan: It is a participating, non-linked money-back insurance plan. LIC New Children's Money Back Plan is ideal for families who prefer periodic payouts to meet education expenses at different stages. The plan pays 20% of the basic sum assured at ages 18, 20, and 22, while the remaining 40% is paid at maturity, along with eligible bonuses.

Note: In addition to the listed plans, you might have heard of the LIC Kanyadan Policy. It is a popular market term used by agents to describe LIC Jeevan Lakshya (Plan 733) because the plan is often positioned as a solution for funding a daughter's education or marriage. Before buying, always verify the actual policy name and features.

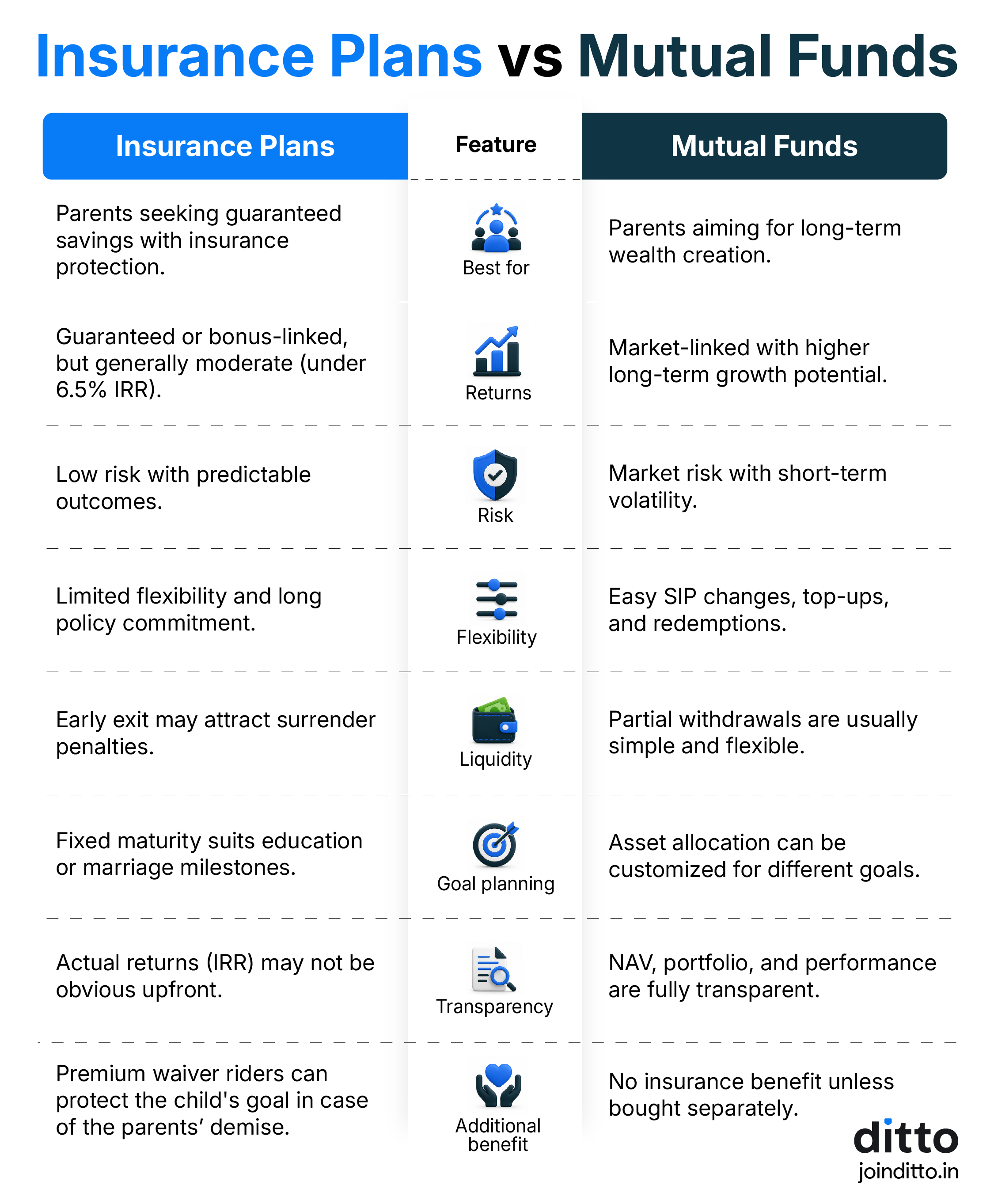

Mutual Funds vs Insurance for Girl Child

Choosing between mutual funds and insurance for a girl child's future depends on your primary goal. Mutual funds focus on long-term wealth creation, while insurance plans combine savings with life cover. Both have a role, but they serve very different purposes.

Take a look at the infographic below to see how they compare and which option may better suit your family's needs.

Note: In the above infographic, IRR stands for internal rate of return, and NAV stands for net asset value.

One-Time Investment Options Explained

- SSY Lump Sum Deposit: Offers attractive sovereign-backed returns with tax benefits, but the money remains locked in until maturity, except for limited withdrawals.

- Bank Fixed Deposit (FD): Provides predictable returns with low risk, though premature withdrawals may reduce the interest earned.

- National Savings Certificate (NSC): Offers fixed returns backed by the Government of India and qualifies for tax benefits under eligible provisions. The current interest rate offered is 7.7% per annum.

- Post Office Time Deposit: Available with multiple tenure options and suits those who prioritize capital safety over higher returns.

- Public Provident Fund (PPF): Combines government-backed safety with tax-free interest and maturity, making it a strong long-term savings option. The current interest rate is 7.1% per year.

- Debt Mutual Fund: Offers better flexibility than traditional deposits, but returns are market-linked and not guaranteed. For example, HDFC Short Term Debt Fund Direct has offered 7.91% since inception.

- Hybrid Mutual Fund: Balances equity and debt investments, aiming for growth above fixed-income products while offering lower volatility than pure equity funds. For instance, HDFC Balanced Advantage Fund Direct has offered 14.56% since inception.

- Equity Index or Flexi-Cap Mutual Fund: Has the highest growth potential but also carries market risk, making patience and a long investment horizon essential.

- NPS Vatsalya: Invests in market-linked assets for long-term growth, but the money remains locked in primarily for retirement rather than education or marriage goals.

Tax Benefits, Lock-In Period, and What Option to Choose

Tax Benefits

- SSY: Sukanya Samriddhi Yojana follows the EEE (Exempt-Exempt-Exempt) structure. The investment deposit qualifies under Section 123 (previously Section 80C), subject to the overall ₹1.5 lakh limit under the old tax regime.

- Mutual Funds & FDs: Mutual fund gains are taxed as capital gains when redeemed. Interest earned on Bank FDs and RDs is generally taxable as per your income tax slab.

- Insurance Plans: Insurance plans offer tax deductions on premiums under the old tax regime. Premiums qualify for deductions under Section 123. Policy proceeds, including guaranteed additions, are tax-free under Section 11 (previously Section 10(10D)). Death benefits paid to nominees are generally tax-free. Maturity proceeds, including bonuses or guaranteed additions, remain tax-free only if the policy satisfies the applicable Income-tax Act conditions.

Lock-In Period

- SSY: 21-year maturity with limited withdrawals for education or marriage.

- PPF: 15-year lock-in with limited withdrawal and loan provisions.

- NSC: Fixed 5-year lock-in.

- Bank FD: Flexible tenure; premature withdrawal may attract penalties.

- Mutual Funds: Generally, no lock-in (except for equity-linked savings schemes), but a long investment horizon is recommended.

- LIC Child Plans: Long-term insurance contracts with surrender rules.

- NPS Vatsalya: Long-term retirement-focused investment with limited liquidity.

The ideal investment option depends on when you start.

No matter which option you choose, adequate parental term insurance is essential. A ₹2 crore term plan can protect your child's education far better than a low-cover savings policy. Don't buy child plans based on emotions alone. Compare returns, lock-in, and flexibility, and choose a solution that fits your daughter's age and your financial goals.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 25,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Conclusion

Choosing the right investment plan for a girl child depends on your goals, time horizon, and risk appetite. For most parents, a combination of SSY for guaranteed savings and equity mutual funds for long-term growth offers a balanced approach. No single product is ideal for every family, so build a portfolio that can keep pace with rising education and marriage costs.

Alongside investing, protect your family's financial future with adequate insurance. Before committing to child-focused savings plans, ensure both parents have one of the best term insurance plans for income and liability protection and one of the best health insurance plans to safeguard savings from unexpected medical expenses.

Frequently Asked Questions

Last updated on: