Overview

With the average expenditure on course fees in urban areas estimated at ₹15,143 per student, planning early for your child’s future has become essential. As education costs continue to rise over time, many parents look for dedicated financial products that can help build a future corpus in a structured manner. SBI Life child insurance plan combines savings, protection, and long-term wealth creation to help parents prepare for rising education and milestone expenses.

In this guide, we break down child plans by SBI Life, their features, and if they are a good fit for your family's needs.

What Is an SBI Life Insurance Child Plan?

Child plans by SBI Life Insurance are designed to help parents build a dedicated financial corpus for their child’s education, higher studies, and future milestones.

Most child insurance plans in the market keep the parent as the life assured, since the earning parent is the financial risk being covered. However, SBI Life Smart Platina Young Achiever and Smart Future Star are unique in that regard because the child is the life assured.

This distinction is important because it determines how the policy responds if something happens to either the parent or the child. While no parent buys a child plan expecting a death benefit on the child’s life, the structure affects policy benefits and how the final payout is handled.

Did You Know?

Features of an SBI Life Child Insurance Plan

Protection for the Child’s Future

SBI child plans include an in-built waiver of premium benefit, helping the child’s financial goal continue even if the parent dies or suffers a disability.

Disciplined Long-Term Savings

These plans encourage structured investing for education and future milestones, reducing the likelihood that parents will interrupt savings midway.

Multiple Return Options

SBI offers guaranteed, bonus-linked, and market-linked child plans, allowing parents to choose based on their risk appetite and financial comfort.

Flexible Maturity Payouts

Benefits can support education, marriage, or career goals through lump sum or milestone-based payouts aligned with the child’s future needs.

Detailed Review of Popular SBI Life Insurance Plans

1. Smart Platina Young Achiever

SBI Life Insurance Smart Platina Young Achiever is an individual, non-linked, non-participating child savings insurance plan. In this policy, the child is the life assured, while the parent, grandparent, or legal guardian acts as the proposer and policyholder. The policy offers flexible settlement options and guaranteed additions.

Key Features:

- Guaranteed Maturity Benefit: If the policy stays active till maturity, the child receives the sum assured on maturity along with accrued guaranteed additions.

- Waiver of Premium Benefit: If the proposer dies or suffers accidental total permanent disability during the premium payment term, future premiums are waived while the policy continues uninterrupted for the child.

- Child Death Benefit: If the child dies during the policy term, the insurer pays the higher of the sum assured on death plus accrued guaranteed additions or 105% of total premiums paid.

Eligibility Criteria

2. Smart Future Star

SBI Life Insurance Smart Future Star is a participating plan which is designed to create long-term savings for a child’s future goals. It includes an in-built waiver of premium benefit linked to the proposer’s life.

Key Features

- Maturity Benefit: If the child survives till policy maturity, the plan pays the sum assured on maturity along with vested reversionary bonuses and terminal bonus, if declared.

- Waiver of Premium Benefit: If the proposer dies or suffers accidental total permanent disability during the premium payment term, future premiums are waived while the policy continues for the child.

Eligibility Criteria

3. Smart Scholar Plus

SBI Life Insurance Smart Scholar Plus is an individual, unit-linked, non-participating child savings insurance plan and comes with a mandatory 5-year lock-in period. The plan offers 10 different fund options and includes loyalty additions and maturity benefits. You also receive a premium waiver and accidental benefits.

Key Features

- Market-Linked Investment: Premiums are invested in market-linked funds chosen by the policyholder. The final maturity value depends on how these funds perform over the policy term.

- Death Benefit: If the life assured (parent) dies during the policy term, the higher of sum assured or 105% of total premiums paid is paid immediately. Future premiums are waived, and the policy continues for the child.

- Partial Withdrawals & Fund Switching: Partial withdrawals are allowed from the 6th policy year. The plan also allows fund switching and premium redirection flexibility.

Eligibility Criteria

Note: Such child plans neither offer enough life cover nor adequate returns which is why some parents prefer to separate insurance and investments rather than combine both within a child plan. If you prefer SBI Life, you can explore term plans like Smart Shield Plus.

Premium Illustration and Payout Structure

In this illustration, a 35-year-old person purchases a child plan for her 3-year-old child with an annual premium of ₹50,011. The premium is payable for 10 years, while the policy continues for a total term of 20 years. Over the policy duration, the total premium outgo amounts to ₹5,00,110, and the plan provides a sum assured of ₹6,32,000.

Maturity Benefit

Note: The illustrated figures are derived from the Smart Future Star policy brochure. Actual figures depend on the sum assured, age, and insurer’s underwriting policy. The maturity value in this illustration translates to an estimated net annualized return of about 2.3% at the 4% scenario and around 6.4% at the 8% scenario.

The net return is lower than the illustrated growth rates because a portion of the premium goes towards insurance costs and policy expenses instead of being fully invested. For long-term goals such as higher education, a net return of 2.3% may struggle to keep pace with inflation, while 6.4% may still fall short of the returns many investors seek over a 15–20 year horizon.

SBI Life Insurance also offers a Child Education Planner to estimate future education funding needs. However, it should be treated only as a planning tool. The final choice should depend on affordability, liquidity, risk appetite, waiver benefits, charges, flexibility, and overall long-term suitability.

Is SBI Life Insurance the Right Choice for Your Child?

SBI Life Child Plans can suit parents who want disciplined long-term savings, structured milestone-based payouts, and financial continuity for their child’s future goals, even if something happens to the earning parent.

However, parents primarily focused on maximizing long-term returns or minimizing costs may find a simpler approach more efficient. At Ditto, we believe the first priority should be securing adequate life cover through the best term insurance plans available for the parent.

After that, options like low-cost mutual funds, Public Provident Fund (PPF), Sukanya Samriddhi Yojana (SSY), or other goal-based investments may offer greater flexibility, lower costs, and potentially better long-term wealth creation.

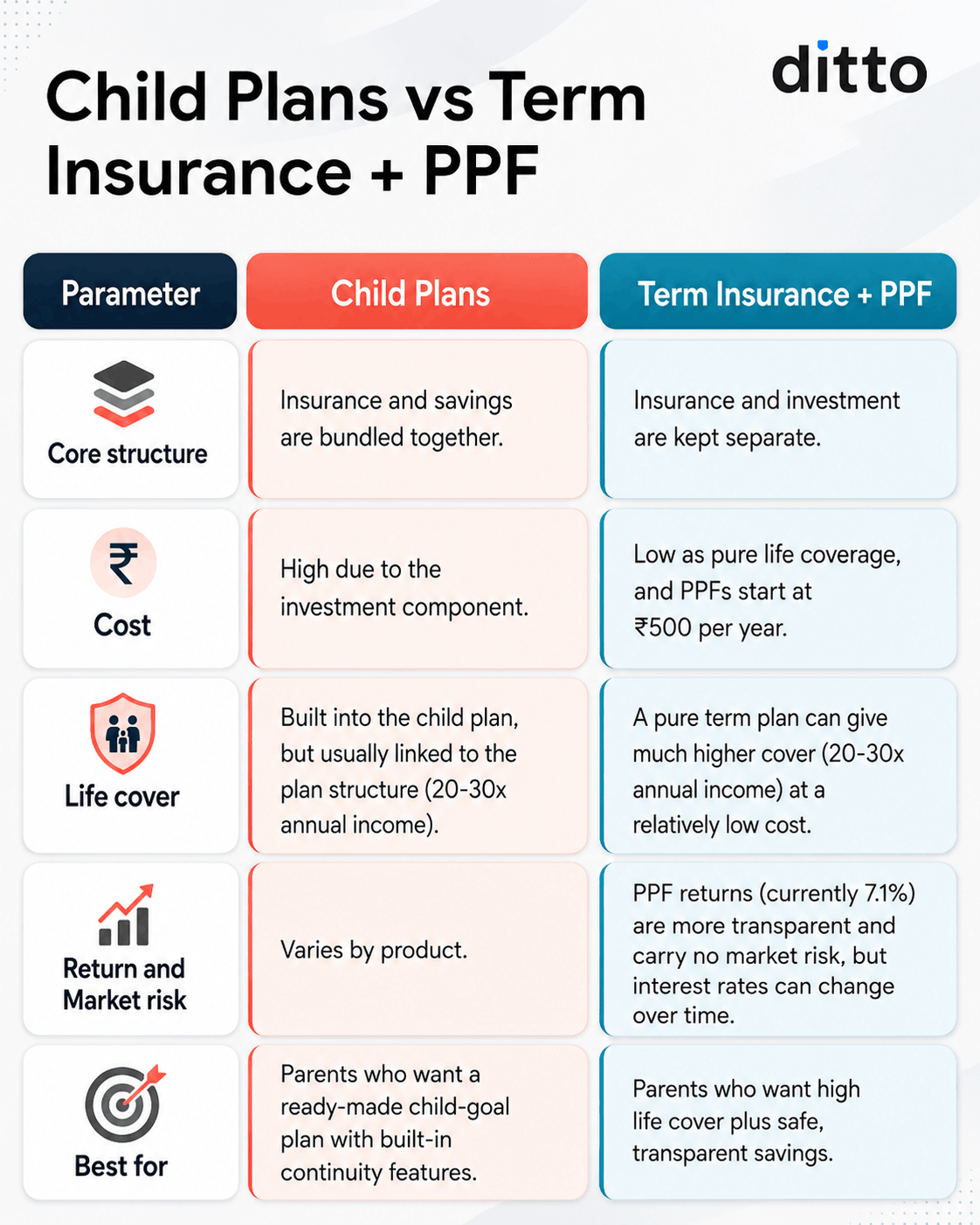

Take a look at the infographic to get an idea of how a child plan compares with a separate investment in term insurance and PPF.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 22,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

SBI Life Child Plans can suit parents who want structured savings with milestone-based payouts and waiver-of-premium protection for the child’s future. They work best for families seeking disciplined long-term planning through guaranteed, bonus-linked, or market-linked options.

Those exploring SBI Life Insurance plans may first consider Smart Shield Plus or Smart Shield Premier to secure adequate life cover for the earning parent. Once the protection need is addressed, the child's education or future corpus can be built separately through investment options such as mutual funds, PPF, SSY (for a girl child), or other goal-based investments. This approach keeps insurance and wealth creation separate, often resulting in higher life cover, greater flexibility, better liquidity, and potentially stronger long-term outcomes.

Frequently Asked Questions

Last updated on: