When comparing the Sukanya Samriddhi Yojana vs LIC Kanyadan Policy, the biggest difference lies in their purpose. Sukanya Samriddhi Yojana (SSY) is a government-backed savings scheme focused on long-term wealth creation for a girl child through fixed, tax-free returns. LIC Kanyadan Policy (officially LIC Jeevan Lakshya) combines savings with life insurance protection for the earning parent.

SSY offers predictable returns, while LIC Kanyadan provides financial support to the family if the insured parent passes away during the policy term.

However, at Ditto, we do not recommend plans that combine insurance and investment, as both tend to underperform. Many financial planners prefer using SSY for wealth accumulation and adding separate term insurance for cost-effective life cover. This guide helps those who wish to explore the differences between the two plans.

Planning your daughter’s future often starts with one big financial question: Should you prioritize guaranteed savings, life insurance protection, or a mix of both? Sukanya Samriddhi Yojana and Life Insurance Corporation of India (LIC) Kanyadan-focused plans approach this goal very differently, and choosing the right strategy can significantly impact long-term financial security.

In the next few minutes, we will walk you through the difference between SSY and the LIC Kanyadan Policy and help you understand if they meet your future goals.

Confused if Sukanya Samriddhi Yojana or LIC Kanyadan Policy aligns with your long-term family goals? Book a free call or chat on WhatsApp with a Ditto advisor.

Is the LIC Kanyadan Policy a Separate LIC Life Insurance Policy?

No, LIC does not officially offer a standalone policy called “LIC Kanyadan Policy.” The term became popular through agents and advisors who used it as an emotional way to position daughter-focused financial planning. When LIC agents talk about Kanyadan Policy, the policy being referred to is LIC Jeevan Lakshya (Plan 733), which gradually became widely known online and offline as the “LIC Kanyadan Policy.”

Sukanya Samriddhi Yojana vs LIC Kanyadan Policy: Quick Comparison

Parameter

Sukanya Samriddhi Yojana

LIC Kanyadan Policy (LIC Jeevan Lakshya)

Nature of Product

Government-backed small savings scheme

Participating, non-linked life insurance savings plan

Who is it for?

Girl child

Usually bought by a parent for child-related goals

Whose Name is it in?

Girl child’s name (until age 10 is attained)

Life assured is usually the parent/proposer, not necessarily the daughter

Purpose

Long-term savings for daughter’s education/marriage/future

Savings plus life cover for the parent

Risk Level

Very low, backed by the government's small savings framework

Low to moderate, but returns are product/bonus dependent

Maturity

21 years from account opening, or premature closure for marriage after age 18

Policy term selected at purchase, usually 13 to 25 years under the current Jeevan Lakshya

Deposit/Premium Limit

₹250 minimum and ₹1.5 lakh maximum per financial year

Premium depends on age, policy term, sum assured, riders, and underwriting.

What Is Sukanya Samriddhi Yojana?

Sukanya Samriddhi Yojana (SSY) is a government-backed small savings scheme launched under the Beti Bachao Beti Padhao initiative in 2015. It is designed to help parents build long-term savings for a girl child’s education, marriage, or future financial needs.

SSY currently enjoys Exempt-Exempt-Exempt (EEE) tax status, which means investments made, interest earned, and maturity proceeds are tax-free under applicable rules.

Did You Know?

Sukanya Samriddhi Yojana had over 4.53 crore accounts and deposits exceeding ₹3.33 lakh crore by December 2025. The Government of India now positions SSY not just as a savings scheme, but as a major financial empowerment initiative focused on girl-child education and long-term financial security.

What Is the LIC Kanyadan Policy (Jeevan Lakshya)?

The LIC Kanyadan Policy is not a separate official LIC product but is marketed around LIC Jeevan Lakshya. It is a participating life insurance plan that combines savings with life cover for the earning parent. The policyholder gets to participate in LIC’s annual profits.

The policy offers a minimum basic sum assured of ₹2 lakh, with no upper limit (subject to underwriting). LIC Jeevan Lakshya offers three riders, which include the Accidental Death and Disability Benefit Rider, the Accident Benefit Rider, and the New Term Assurance Rider.

While purchasing a term plan, adding riders to the base policy increases premium cost, so add the ones you actually need. You can use a third-party LIC Kanyadan Policy calculator to get a rough estimate of premiums and maturity benefits.

Eligibility Criteria

Eligibility

Criteria

Age Band

18 to 50 years

Maturity Age

31 to 65 years

Policy Term

13 to 25 years

Premium Payment Term

(Policy Term minus 3) years

Premium Payment Frequency

Yearly, half-yearly, quarterly, and monthly

Payout Options

The death benefit can be received in installments over 5, 10, or 15 years (monthly, quarterly, half-yearly, or yearly) instead of a lump sum

CTA

Returns, Tax Benefits, and Flexibility: Head-to-Head

Parameter

Sukanya Samriddhi Yojana

LIC Kanyadan / Jeevan Lakshya

Return Type

Government-notified interest rate

Maturity benefit plus LIC bonuses, if declared (5% to 7% net IRR historically)

Current Rate

SSY rate is 8.2% for Q1 FY 2026-27, unchanged from the previous quarter

No fixed interest rate. LIC says the maturity benefit is the basic sum assured plus vested simple reversionary bonuses and the final additional bonus, if any

Tax on Investment / Premium

The investment deposit qualifies under Section 80C (old regime)

Premiums paid qualify under Section 80C, subject to limits and the old tax regime

Tax on Returns

Interest earned and maturity proceeds are exempt under Section 10

Maturity/death benefits may be exempt under Section 10(10D), subject to conditions

Liquidity

Low to moderate. Partial withdrawal up to 50% for education after age 18 or passing Class 10, whichever is earlier

Moderate. Loan and surrender options exist, but surrender can be inefficient

Note: IRR stands for internal rate of return.

Who Should Choose the Sukanya Samriddhi Yojana?

Parents with a Daughter Below 10 Years: Sukanya Samriddhi Yojana is ideal for parents who want to start early financial planning for their daughter. The account can only be opened before the girl child turns 10, which makes early planning important.

Families Looking for Safe and Stable Savings: This scheme suits conservative investors who prefer government-backed security over market-linked risk. Since the returns are backed by the Government of India, it offers a decent interest rate of 8.2%, well above the 7% fixed deposit rate.

Parents Planning for Education or Marriage Expenses: SSY works well for long-term goals such as higher education or marriage. The long lock-in period encourages disciplined savings over many years.

Investors Seeking Tax-Efficient Wealth Creation: The scheme is attractive to families seeking tax benefits and tax-free maturity proceeds under applicable rules.

People Comfortable with Limited Withdrawals: SSY is suitable for investors who do not require regular access to funds, as withdrawals are restricted and mainly allowed for specific milestones like education.

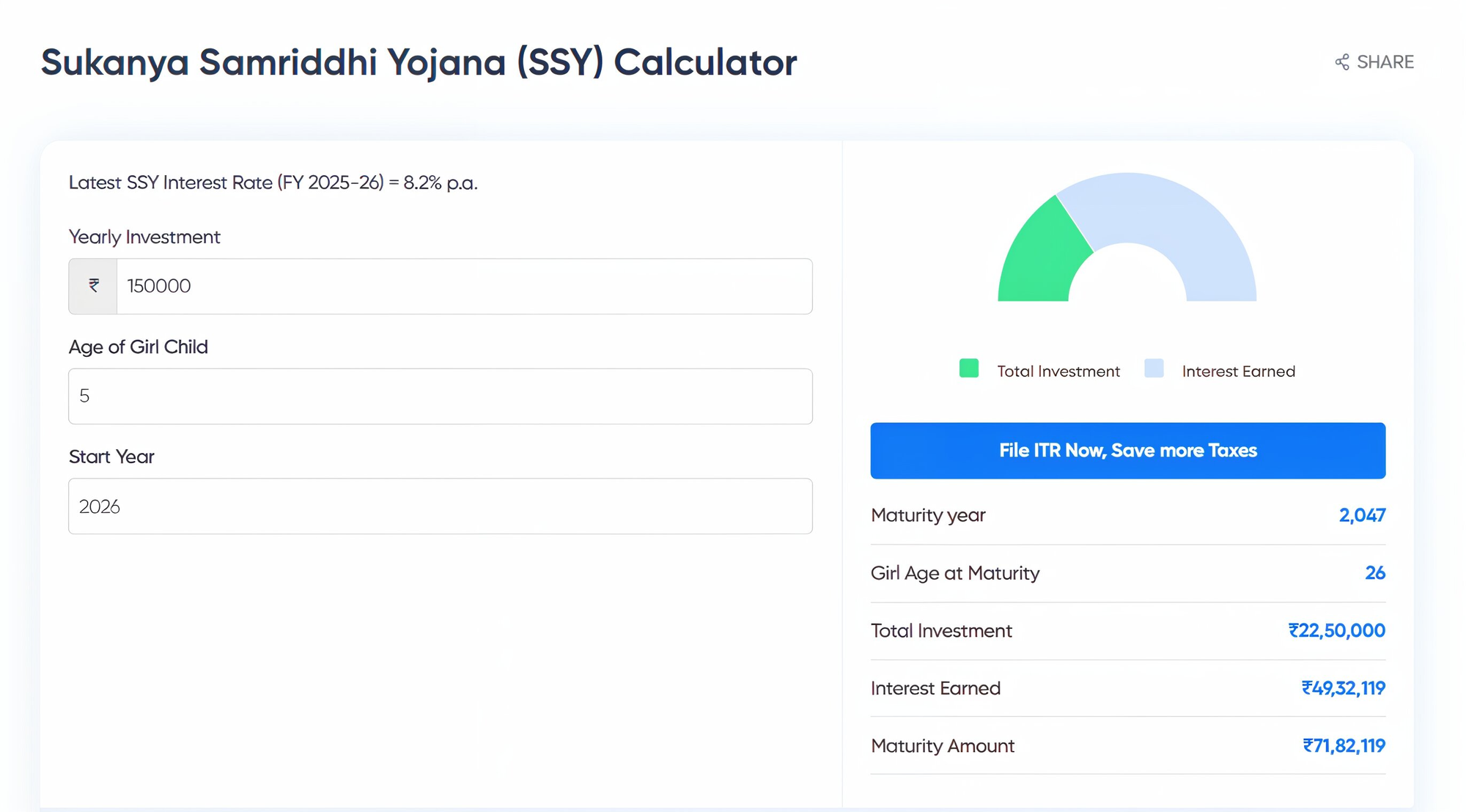

Note: There is no single official Government of India SSY calculator available on the primary Sukanya Samriddhi Yojana scheme portals. Parents can use third-party SSY calculators to estimate maturity value and yearly growth, but it is important to cross-check the assumptions with official SSY rules, contribution limits, tenure conditions, and the latest government-notified interest rate.

When comparing the Sukanya Samriddhi Yojana (SSY) and the LIC Kanyadan Policy, the better option depends on your financial goal.

SSY works better for pure long-term wealth creation for a girl child. It offers government-backed safety, predictable returns, flexible yearly contributions, and strong tax efficiency.

The LIC Kanyadan Policy becomes more relevant when life insurance protection is equally important. Unlike SSY, it provides financial support if the earning parent passes away during the policy term. However, at Ditto, we believe the most efficient approach is combining SSY with a separate term insurance plan.

What About Life Insurance Protection?

Neither option is ideal if your primary goal is adequate life insurance protection.

Sukanya Samriddhi Yojana (SSY) does not provide any life cover. It is purely a government-backed savings scheme designed to build a corpus for a girl child.

LIC Kanyadan Policy, on the other hand, includes a life insurance component, but the coverage is limited relative to a family's actual financial needs.

For most families, a separate term insurance plan for the earning parent, combined with an investment plan, works better. If you wish to explore term plans from established insurers, refer to the guide on the best term insurance plans.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 22,000+ happy customers

Sukanya Samriddhi Yojana (SSY) is usually the stronger choice if your primary goal is disciplined, tax-efficient wealth creation for your daughter. However, SSY should ideally not replace life insurance protection for parents, as the scheme has no insurance component.

A more balanced and financially efficient approach is to combine a pure term insurance plan for the earning parent with SSY for the girl child. This separates protection from investment and often provides better coverage, clearer returns, and greater flexibility.

For long-term financial planning, many families also combine SSY with products like Public Provident Fund (PPF), National Pension System (NPS), and low-cost mutual funds to build a diversified and goal-oriented portfolio for education, retirement, and wealth creation.

Frequently Asked Questions

What is the difference between the Sukanya Samriddhi Yojana and the LIC Kanyadan Policy?

The biggest difference between the Sukanya Samriddhi Yojana (SSY) and the LIC Kanyadan Policy lies in their primary purpose. SSY is a government-backed savings scheme focused purely on long-term wealth creation for a girl child through fixed, tax-efficient returns. LIC Kanyadan Policy, also known as LIC Jeevan Lakshya, combines savings with life insurance protection for the earning parent. SSY works better for disciplined wealth accumulation and predictable compounding. On the other hand, LIC Jeevan Lakshya adds financial protection if the insured parent passes away during the policy term. At Ditto, we usually prefer separating insurance and investment for better flexibility and cost efficiency.

Is the LIC Kanyadan Policy a real LIC product?

No, Life Insurance Corporation does not officially offer a standalone product called LIC Kanyadan Policy. The name became popular because agents and advisors used it as a relatable way to market daughter-focused financial planning solutions, and the actual product being discussed is LIC Jeevan Lakshya. It is a participating life insurance plan that combines savings with life cover. Over time, the phrase LIC Kanyadan Policy became widely used across social media and agent discussions because many parents search for financial plans linked to their daughter’s future education and marriage goals. However, the official LIC product name remains LIC Jeevan Lakshya.

What is the current interest rate of the Sukanya Samriddhi Yojana in 2026?

The Sukanya Samriddhi Yojana (SSY) interest rate for Q1 FY 2026-27 stands at 8.2% per annum. The Government of India reviews and notifies the rate every quarter. Interest rates in schemes like SSY usually do not fluctuate sharply. Since these are government-backed small savings and social security schemes, rates are often kept slightly higher than regular market deposit rates. For parents planning long-term goals such as higher education or marriage for their daughter, the combination of sovereign backing and tax-free compounding makes SSY highly attractive.

How many accounts have been opened under the Sukanya Samriddhi Yojana?

Sukanya Samriddhi Yojana crossed 4.53 crore accounts with deposits exceeding ₹3.33 lakh crore by December 2025. The scheme was launched in 2015 under the Beti Bachao Beti Padhao initiative and has since become one of India’s most widely adopted girl-child savings schemes. The government now positions SSY not only as a savings product but also as a financial empowerment initiative for families planning their daughter’s future. Its popularity comes from the combination of government backing, attractive interest rates, tax-efficient returns, and long-term discipline that encourages structured financial planning for education and marriage expenses.

What is the minimum and maximum deposit in the Sukanya Samriddhi Yojana?

Sukanya Samriddhi Yojana allows a minimum annual deposit of ₹250 and a maximum deposit of ₹1.5 lakh per financial year. The account can only be opened before the girl child turns 10 years old. Contributions are required for 15 years from the date of opening, while the account matures after 21 years. This flexible deposit range makes the scheme accessible across different income groups. Families can contribute small amounts consistently or maximize the yearly limit for stronger long-term compounding. The structure encourages disciplined saving while still giving parents enough flexibility to contribute according to their financial capacity each year.

What are the tax benefits of the Sukanya Samriddhi Yojana?

Sukanya Samriddhi Yojana enjoys strong tax benefits under Indian tax laws. Deposits qualify for deduction under Section 80C up to ₹1.5 lakh annually under the old tax regime. The interest earned on the account is fully tax-free, and the maturity amount is also exempt from tax under current rules. This gives SSY an EEE or exempt-exempt-exempt status, which is one of its biggest advantages. Few traditional savings products in India offer this level of tax efficiency. LIC Jeevan Lakshya premiums may also qualify under Section 80C, while maturity proceeds can remain tax-exempt under Section 10(10D).

What are the eligibility criteria for the LIC Kanyadan Policy (Jeevan Lakshya)?

LIC Jeevan Lakshya, commonly marketed as LIC Kanyadan Policy, is available for individuals between 18 and 50 years of age. The maturity age ranges from 31 to 65 years, depending on the selected policy term. The policy term generally ranges from 13 to 25 years, while the premium payment term is shorter by three years. The minimum basic sum assured starts at ₹2 lakh, with no fixed upper limit subject to underwriting approval. Premiums can usually be paid yearly, half-yearly, quarterly, or monthly. The policy combines long-term savings with life insurance protection for the earning parent during the policy tenure.

Can I withdraw money from the Sukanya Samriddhi Yojana before maturity?

Yes, Sukanya Samriddhi Yojana allows partial withdrawals under specific conditions. Parents can withdraw up to 50% of the account balance for higher education expenses once the girl child turns 18 or passes Class 10, whichever happens earlier. Premature closure is also allowed in limited cases, such as the girl’s marriage after age 18 or certain compassionate grounds. Apart from these situations, the Sukanya Samriddhi Yojana has relatively low liquidity and is best suited to families comfortable with long-term financial discipline.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.