Term insurance for High Net-Worth Individuals (HNIs) is less about replacing income and more about protecting wealth. It can create instant liquidity, so families do not need to sell property, investments, or business stakes in a hurry. Term insurance for HNIs can also cover large loans, support business continuity, and simplify estate transfer.

In India, premiums may qualify for Section 80C (old regime) benefits, while eligible payouts are usually tax-free under Section 10(10D). Our top pick is Axis Max Life Smart Term Plan Plus, backed by a 99.62% average claim settlement ratio (average FY 2022-25), strong features, and competitive pricing. A 40-year-old non-smoking male HNI in Delhi may pay about ₹98,625 yearly for a ₹5 crore cover. This guide explores the best term insurance plans for HNIs.

When wealth grows, so do responsibilities. For high-net-worth individuals, term insurance is a smart way to secure family wealth, cover large liabilities, and create instant liquidity when it matters the most.

This article helps you understand how term insurance for HNIs works, how to choose the right coverage, and how to use it effectively for wealth protection, liquidity, and long-term financial security.

A High Net-Worth Individual is someone with meaningful liquid wealth that can be accessed quickly, such as cash, stocks, bonds, or mutual funds. In India, HNIs are commonly viewed as individuals with liquid assets up to ₹5 crore. Those with wealth above ₹25 crore are often classified as Ultra-HNIs (UHNIs).

The key idea is not total wealth, but how much liquid capital is readily available when opportunities or emergencies arise. As per Economic Times, India had 85,698 High Net-Worth Individuals, ranking 4th worldwide. This reflects rising entrepreneurship, expanding capital markets, and growing private wealth across sectors.

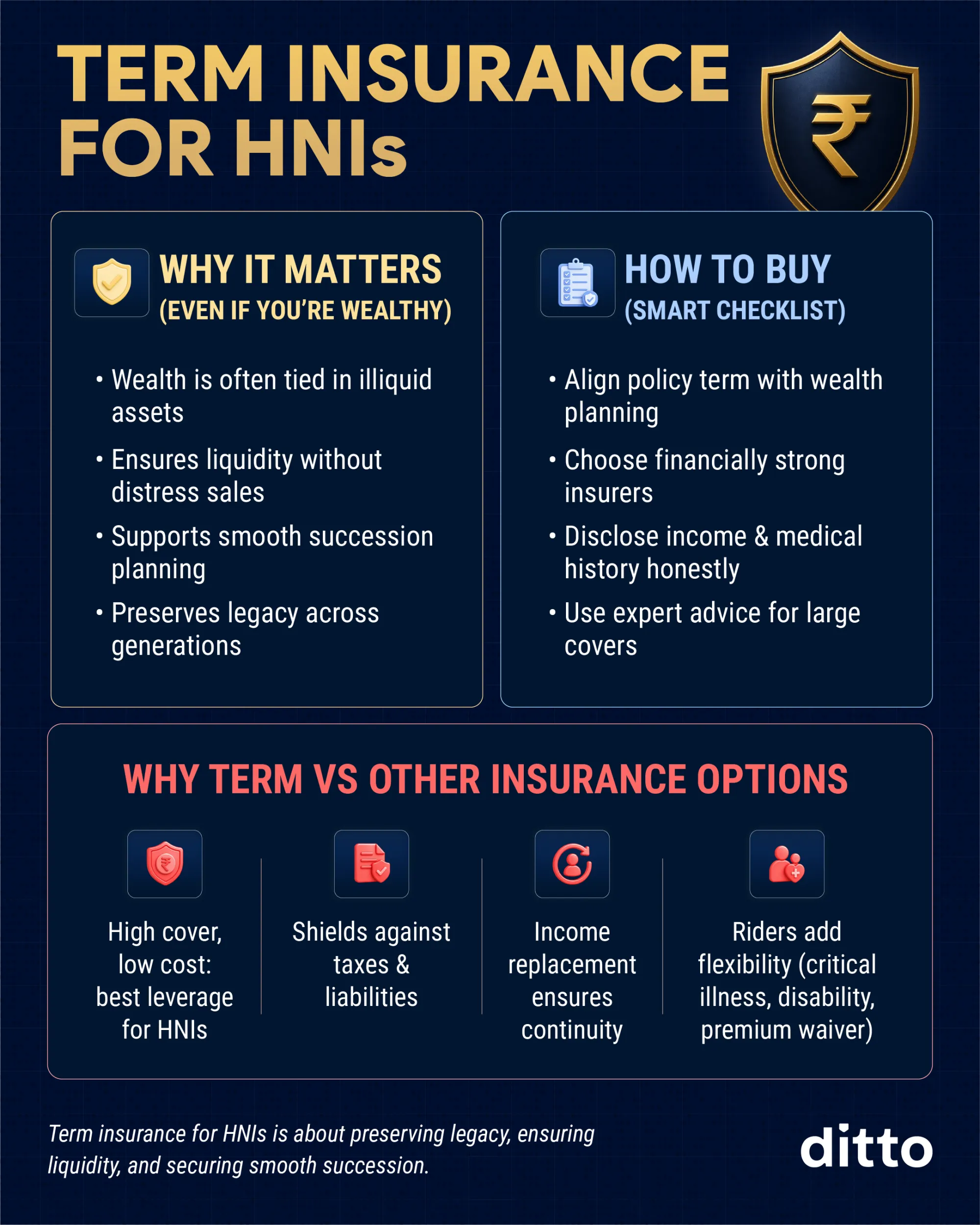

This above infographic explains why term insurance still matters for high net worth individuals, even if they already have substantial wealth. It shows how term plans help maintain liquidity, support smooth succession, and protect legacy, while also guiding you on how to choose and structure the right policy.

Best Term Insurance Plans for HNIs

01

Axis Max Life

Smart Term Plan Plus

Axis Max Life Smart Term Plan Plus stands out as a strong all-around term insurance option for buyers who want reliable claims support, practical features, and competitive pricing in one plan.

Axis Max Life

Smart Term Plan Plus

4.7

Overall Rating

Insurer Rating

5.0/5

Customer Service

5.0/5

Feature Rating

4.1/5

Premium Rating

5.0/5

Key Features:

Critical Illness Cover: Protection for up to 64 listed illnesses for a fixed period of 20 years.

Terminal Illness Benefit: Accelerated payout of up to ₹1 crore on diagnosis of a covered terminal illness.

Cover Continuance Benefit: Option to defer premiums for up to one year under eligible conditions without immediate loss of cover.

Instant Claim Support: Advance payout of up to ₹2 lakh at claim intimation, subject to policy terms.

Waiver of Premium: Future premiums may be waived on 11 specified illnesses or 4 disability events.

Health Services: Teleconsultation, wellness support, and network discounts through the insurer app.

Final Take:Axis Max Life Smart Term Plan Plus is one of the best overall term plans in India because it combines useful benefits with strong claim credibility. Axis Max Life has also reported an excellent recent claim settlement track record, which adds confidence for long-term buyers.

2

HDFC Life

Click 2 Protect Supreme Plus

HDFC Life Click 2 Protect Supreme Plus is a strong choice for buyers who value insurer reputation, flexible features, and dependable long-term service. It may not always be the lowest-priced option, but it offers solid overall value.

HDFC Life

Click 2 Protect Supreme Plus

4.4

Overall Rating

Insurer Rating

4.5/5

Customer Service

5.0/5

Feature Rating

4.4/5

Premium Rating

3.0/5

Key Features:

Waiver of Premium: Future premiums may be waived on 60 critical illnesses or disability events while coverage continues.

Life Stage Benefits: Option to increase cover after marriage, home loan, or childbirth without fresh underwriting in eligible cases.

Flexible Claim Payouts: Nominees can choose monthly income or structured payouts instead of only a lump sum.

Critical Illness Rider: Additional protection for up to 60 listed illnesses for a fixed benefit period.

Premium Break Option: Temporary premium pause for one year with later repayment, subject to terms.

Digital Support Tools: Includes partial instant payout options and wellness services.

Final Take:HDFC Life Click 2 Protect Supreme Plus suits buyers who prefer a trusted large insurer with a strong claims history and useful flexibility. It is ideal for those comfortable paying slightly more for service, confidence, and brand strength.

3

ICICI Prudential

iProtect Smart Plus

ICICI Prudential iProtect Smart Plus is a practical term insurance option for buyers who want a trusted private insurer, competitive pricing, and useful features without unnecessary complexity. It balances affordability with flexibility well.

ICICI Prudential

iProtect Smart Plus

4.3

Overall Rating

Insurer Rating

4.4/5

Customer Service

5.0/5

Feature Rating

3.8/5

Premium Rating

5.0/5

Key Features:

Life Stage Protection: Option to increase cover after marriage, childbirth, or home loan disbursement in eligible cases.

Smart Exit Benefit: Choice to exit after a defined period and receive eligible premiums back under selected variants.

Premium Break Option: Temporary pause on premiums for up to one year after regular payments, subject to terms.

Instant Partial Payout: Early claim support with accelerated payout of ₹3 lakh for eligible higher covers.

Flexible Claim Payouts: Nominees can choose lump sum or income-based payout formats.

Final Take:ICICI Prudential iProtect Smart Plus suits buyers who want a clean mainstream product with strong brand confidence and sensible flexibility. It is especially appealing if price matters, but you still want practical long-term features.

4

Bajaj Life

eTouch II

Bajaj Life eTouch II is a solid term insurance option for buyers who want affordable premiums, dependable core benefits, and a simple product structure. It offers strong value without sacrificing credibility.

Bajaj Life

eTouch II

4.2

Overall Rating

Insurer Rating

4.4/5

Customer Service

5.0/5

Feature Rating

3.4/5

Premium Rating

5.0/5

Key Features:

Terminal Illness Benefit: Early payout on diagnosis of a covered terminal illness, up to ₹2 crore.

Waiver of Premium: Future premiums may be waived on specified accidental disability or terminal illness events.

Flexible Claim Payouts: Nominees can choose structured income payouts instead of only a lump sum.

Premium Holiday Add-on: Option to temporarily skip premiums under eligible conditions while keeping cover active.

Early Exit Value: Available at older ages under selected terms and policy conditions.

Health Services: Includes teleconsultation, health checkups, and discounts on pharmacy or lab services.

Final Take:Bajaj Life eTouch II suits buyers who prioritize lower premiums and practical benefits. It is especially attractive for value-conscious customers and can also be a strong option for Non-Resident Indians (NRIs) seeking competitive pricing.

5

Aditya Birla Sun Life

Super Term Plan

Aditya Birla Sun Life Super Term Plan is a well-rounded option for buyers who want term insurance with meaningful inbuilt illness benefits. It can be especially useful for those who prefer broader protection inside one policy instead of adding multiple riders separately.

Aditya Birla Sun Life

Super Term Plan

4.0

Overall Rating

Insurer Rating

3.7/5

Customer Service

5.0/5

Feature Rating

4.3/5

Premium Rating

5.0/5

Key Features:

Inbuilt Accelerated Critical Illness Cover: Protection for 42 listed illnesses with payout up to 50% of sum assured, capped at ₹50 lakh.

Terminal Illness Benefit: Early payout support of up to ₹1 crore on diagnosis of a covered terminal illness.

Disability Support: A premium waiver may apply for accidental total and permanent disability when selected.

Life Stage Flexibility: Option to increase cover after marriage, childbirth, or home purchase in eligible cases.

Cover Continuance Benefit: Premium deferment option under specific policy conditions.

Early Claim Support: Includes partial payout on claim intimation and exit value under selected terms.

Final Take: Aditya Birla Sun Life Super Term Plan suits buyers who value flexibility and built-in protection benefits. It is a strong fallback option when illness cover matters as much as life cover.

Plans like SBI Life Smart Shield Premier and Tata Maha Raksha Supreme Select are positioned for high-value buyers, with minimum sum assured requirements that often start at ₹2 crore or higher. For such high covers, insurers often require higher minimum income levels, usually ₹10–15 lakh per annum or more, to qualify for large term insurance coverage.

Talk to an expert today and find the right insurance for you.

How Is Term Insurance for HNIs Different From Regular Policies?

Term insurance for HNIs usually involves stricter underwriting than standard retail policies. However, these policies are largely similar to standard term plans, with the main difference being a higher sum assured. Since cover amounts can run into several crores, insurers assess both health risk and financial justification more carefully.

Deeper Underwriting: For covers above ₹5 crore, insurers often ask for advanced medical tests such as 2D Echo, treadmill stress test, pulmonary function test, and expanded blood panels. For larger covers, especially above ₹10 crore, reinsurer approval may also be required, which can increase processing time.

Stronger Financial Documentation: Insurers typically request the last three years of Income Tax Returns (ITRs), recent bank statements, salary slips, or audited business financials. Business owners may need Chartered Accountant-certified statements.

Extra Checks for Complex Income Profiles: If income comes from multiple sources such as business profits, rent, dividends, or capital gains, insurers may ask for additional clarity and proof.

Sample Premiums for HNI Term Insurance Plans

Age

HDFC Life Click 2 Protect Supreme Plus

Axis Max Life Smart Term Plan Plus

ICICI iProtect Smart Plus

30 (Male)

₹60,540

₹55,800

₹53,561

30 (Female)

₹51,459

₹47,430

₹45,527

35 (Male)

₹81,152

₹71,165

₹69,611

35 (Female)

₹68,979

₹60,495

₹59,169

40 (Male)

₹1,04,149

₹98,625

₹94,989

40 (Female)

₹88,527

₹83,835

₹80,741

Note: The listed premiums are illustrative and based on non-smoker profiles in Delhi (110001) with a ₹5 crore sum assured (cover up to age 70 with no first-year discount). Actual premiums may vary based on age, health, occupation, and insurer underwriting.

Women can get up to 15% lower premiums due to lower mortality risk, but age has a much bigger impact on pricing.

Premiums for ₹5 crore and ₹10 crore plans rise sharply between ages 30 and 40 as risk increases.

High cover plans remain cost-efficient when you buy early, especially for the level of protection they offer.

Waiting often costs more than increasing your cover early.

For affluent buyers, securing the right cover sooner usually makes more financial sense.

Take Note: Premiums do not rise in a proportionate way when you choose higher coverage. In many cases, increasing cover from ₹5 crore to ₹10 crore or ₹15 crore does not mean paying exactly double or tripling the premium, as insurers often price larger covers more efficiently at younger ages.

Let’s take the example of HDFC Life Click 2 Protect Supreme Plus. The annual premiums shown are for non-smoker profiles with coverage continuing up to age 70. The illustrative figures exclude first-year discounts and taxes.

Sample Premiums Across Sum Assured and Profiles

Age

₹10 crore

₹15 crore

30 (Male)

₹1,09,591

₹1,62,202

30 (Female)

₹93,152

₹1,37,872

40 (Male)

₹1,89,716

₹2,81,411

40 (Female)

₹1,61,259

₹2,39,199

At age 30, if you choose a ₹10 crore cover under HDFC Life Click2Protect Supreme Plus, the premium is about 1.81 times that of a ₹5 crore cover, not double. Even at ₹15 crore, which is three times the cover, the premium is only about 2.67 times higher.

Which Premium Payment Mode Do HNIs Prefer for Term Insurance?

Many HNIs may prefer regular pay or limited pay based on their cash flow and how they want to allocate capital efficiently. The decision often comes down to cash flow, capital efficiency, and how they prefer to deploy wealth.

Regular Pay: This suits HNIs who have strong alternate uses for capital. Instead of paying a large amount upfront, they keep funds available for business expansion, market investments, or strategic opportunities. It also reduces immediate cash outflow.

Limited Pay: Often the most practical choice for affluent buyers. Premiums are completed within 5, 10, or 15 years, while cover continues for a longer period. It appeals to entrepreneurs with high current income, promoters nearing retirement, or those who want future obligations reduced early.

Single Pay: Usually chosen for simplicity, certainty, or excess liquidity. It removes future premium risk, but the upfront capital may have earned better returns elsewhere.

Why HNIs Need a High Cover Term Insurance?

01

Wealth on Paper Is Not Always Cash in Hand

Many HNIs hold assets in real estate, private businesses, Employee Stock Option Plans (ESOPs), promoter shares, or long-term investments. These may carry high value, but they cannot always be converted into cash quickly. If an unexpected death occurs, the family may face a cash shortage despite substantial net worth. A high-cover term plan solves that liquidity gap immediately.

02

Liabilities Are Usually Larger and More Complex

For affluent families, obligations often extend far beyond a home loan. They may include loans against property, business borrowings, personal guarantees, children’s overseas education, elderly parent support, and premium lifestyle commitments. A higher term cover helps absorb these responsibilities without disrupting family finances.

03

It Prevents Forced Sale of Valuable Assets

This is one of the most overlooked reasons. Without liquid cash, families may be pushed to sell property at a discount, exit investments during a market decline, or accept poor terms in a business buyout. A large insurance payout gives heirs time, flexibility, and negotiating power.

04

Lifestyle Continuity Matters

Many HNI households run on meaningful monthly expenses such as school fees, healthcare, staff salaries, travel, and maintenance. Even a wealthy family can feel pressure if regular cash flow stops suddenly. A high sum assured term cover acts as a financial bridge during transition.

05

Useful for Estate and Succession Planning

Large estates often involve multiple heirs, family businesses, or blended family structures. Insurance can create immediate, ring-fenced liquidity for a spouse or children while other assets are sorted separately. This can reduce conflict and simplify inheritance planning.

Should You Split Your Term Insurance Across Insurers or Choose One?

When you plan your term insurance, how you structure your cover matters as much as the amount you choose. Many people think splitting coverage across insurers is better, but in most cases, keeping it with one insurer can save money and simplify things.

Lower Cost per Lakh: Insurers often offer better pricing as your sum assured increases. This means a larger policy usually costs less per lakh compared to multiple smaller policies.

Tiered Pricing Benefits: Most insurers follow slab-based pricing. As you move into higher cover brackets, the premium per unit of coverage reduces.

Simpler Management: One policy is easier to track, pay, and manage compared to handling multiple policies across insurers.

Better Underwriting Clarity: A single insurer assesses your full risk profile once, which can avoid inconsistencies or complications during claims.

That said, diversification may still make sense in specific cases, but purely from a cost perspective, a higher cover with one insurer is often more efficient.

Benefits of Term Insurance for HNIs

High Sum Assured Options: HNIs often require far higher cover than the average policyholder. Standard ₹1 crore plans may not be enough when there are large loans, business exposure, or significant family obligations. Many insurers offer multi-crore cover, sometimes ₹20 crore or more, subject to underwriting and financial eligibility. This allows affluent families to match insurance cover with real financial risk.

Global Coverage: Many HNIs travel frequently, own overseas assets, or have family members living abroad. Most quality term plans provide payout even if death occurs outside India, provided travel, residency, and disclosure norms are followed correctly. This adds confidence for globally connected families.

Long Policy Tenure Supports Legacy Goals: Many insurers now offer coverage up to age 80, 85, or even 99 and 100 under select plans. For HNIs, longer tenure can make sense because financial responsibilities often continue later in life through dependent spouses, estate planning, or intergenerational wealth transfer.

Protects Wealth From Forced Liquidation: This is one of the most important benefits. Without adequate liquidity, families may need to sell real estate, exit investments, or dilute business ownership under pressure. A strong term payout provides immediate cash and protects long-term assets from a distress sale.

Helps Business and Family Continuity: If one person is central to family wealth creation or business operations, term insurance can help stabilize both the household and enterprise. It gives survivors time to reorganize finances without rushed decisions.

Tax Efficiency: Term insurance can also offer useful tax advantages when structured correctly. Under Section 80C (old regime) of the Income Tax Act, 1961, premiums paid may qualify for deductions up to ₹1.5 lakh annually under the old tax regime, subject to applicable limits and conditions. More importantly, the death benefit paid to nominees is tax-exempt under Section 10(10D), subject to prevailing tax rules.

Customizable Rider Protection: Basic life cover may not be enough for HNIs' households. Riders can strengthen protection based on risk profile. For example, a Waiver of Premium rider can keep the policy active if the insured faces disability or severe illness. Critical Illness or Accidental Disability riders can also provide additional financial support during major setbacks.

See the infographic below to understand which riders to consider and which ones to avoid.

Pure Term Insurance vs Other Life Insurance Products: Which is Better for HNIs?

For HNIs, insurance decisions should start with the financial problem to be solved. Many HNI families tend to compare term insurance with other life insurance products as if they are direct substitutes. However, each serves a different purpose.

Plan Type

Ideal For

Whole Life Insurance

Whole life plans may suit HNIs who want liquidity support whenever death occurs, not only during a fixed term. This can help with legacy transfer, trust planning, or permanent dependent support.

Guaranteed Savings Plans

These can create a dedicated corpus for a spouse, child, or future milestone. They are useful when certainty matters more than return optimization.

Unit-Linked Insurance Plans (ULIPs)

ULIPs may suit HNIs who want long-term market participation inside an insurance structure and are comfortable with lock-in periods and product charges.

Note: Tax benefits on high-premium insurance products have become narrower. ULIPs with annual premiums above ₹2.5 lakh and other policies above ₹5 lakh may face taxation on maturity proceeds, while death-benefit exemptions generally continue under prevailing rules.

The infographic below also explains how term insurance differs from other life insurance products:

Why Term Insurance Often Wins Over Other Life Products for HNIs?

For many HNIs, the primary requirement is liquidity and large protection, not bundled savings. That is why term insurance often works better.

Creates Liquidity: Wealth may sit in property, business stakes, or private investments that take time to sell. A term payout gives immediate cash to the family.

Prevents Forced Sales: Without liquid funds, families may sell assets under pressure. Term cover helps protect wealth from a distress sale.

Best for High-Responsibility Years: During years with loans, children’s education, or business liabilities, term insurance offers strong cover at a lower cost.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

For HNIs, term insurance is a liquidity and wealth-protection tool. The right cover can support family cash flow, clear liabilities, and protect business continuity. Buying early often means lower premiums, easier underwriting, and stronger long-term value before health risks rise.

Choose an insurer with strong financials, and choose a coverage size that accounts for your lifestyle, debts, and estate goals. Some HNIs use multiple policies for very large cover, but for moderate needs, one strong policy often keeps disclosures, servicing, and claims simpler for the family.

In term insurance, HNI usually refers to a High Net-Worth Individual with substantial liquid wealth, not just property ownership. Liquid assets may include cash, stocks, mutual funds, and other investments that can be accessed relatively quickly. In India, HNIs are commonly associated with multi-crore investable assets, while Ultra-HNIs hold significantly higher wealth. In insurance, this matters because HNIs often seek larger cover amounts such as ₹5 to ₹10 crore, or more, which usually involve stricter underwriting and deeper financial checks. A term plan for HNI is designed to offer high coverage limits that align with long-term financial commitments.

Why do high-net-worth individuals need term insurance?

HNIs often have wealth tied up in business ownership, real estate, or long-term investments like alternative investment funds. These assets may be valuable but not instantly liquid. Term insurance offers a high sum assured, which creates immediate cash for the family if something happens unexpectedly. It can help repay liabilities, maintain lifestyle needs, support children’s education, and avoid forced sale of assets at poor prices. For many affluent families, term insurance is less about basic survival and more about preserving wealth, continuity, and financial stability during a difficult transition.

Which are the best term insurance plans for HNIs in India?

What is the difference between regular term insurance and HNI plans?

HNI term insurance is usually not a separate product category. It is often a high-cover version of regular term insurance with deeper underwriting. For large covers such as ₹5 crore or more, insurers may request advanced medical tests, detailed financial documents, and stronger income proof. Covers above ₹10 crore may also need a reinsurer review. Standard retail policies with lower cover amounts usually involve simpler processing. For HNIs, approval depends on the underwriting process, health profile, visible income, liabilities, and insurable need, not wealth alone.

What are the tax benefits of term insurance for HNIs in India?

HNIs can still use term insurance efficiently for protection and estate planning. Premiums may qualify for a deduction under Section 80C (old regime) up to the applicable limit under the old tax regime, subject to current tax rules. More importantly, death benefits paid to nominees are tax-exempt under Section 10(10D), subject to prevailing conditions. For affluent families, this means the payout can pass to beneficiaries with strong tax efficiency. Since tax laws change, it is wise to verify current rules before purchase.

How to calculate the sum assured for HNI term insurance?

HNIs should calculate cover based on liabilities, family cash flow needs, and liquidity gaps rather than using only a salary multiple. Add home loans, loans against property, business guarantees, children’s education costs, and 5 to 10 years of lifestyle expenses. Then assess how much wealth is illiquid and difficult to access quickly. Many affluent buyers start with ₹5 crore or more, but the right number depends on obligations and estate structure. A personalized review is usually smarter than a generic formula. Use our online calculator to get an estimate of how much cover you require.

Is pure term insurance better than ULIP for HNI?

Yes, for most HNIs, pure term insurance is better when the goal is maximum protection at the lowest cost. It can create large liquidity cover without tying up significant capital. Unit-linked insurance plans may suit buyers who want insurance plus market-linked investing in one product, but they are usually less efficient for pure risk cover. Recent tax rules have also reduced the appeal of some high-premium insurance-investment products. Many HNIs prefer term insurance for protection and use separate investment vehicles for wealth growth.

Does term insurance cover HNIs living abroad?

Yes, many Indian term insurance plans can cover HNIs who live abroad or travel frequently, subject to insurer rules. Death benefits are often payable even if death occurs outside India, provided residency status, travel history, occupation, and country of residence were accurately disclosed at the application stage. Premiums and underwriting may differ for term insurance for NRIs or globally mobile applicants. This feature can be valuable for high-net-worth families with overseas assets, children studying abroad, or business interests across countries.

Is HNI term insurance used for estate planning and succession?

Term life insurance can be a powerful estate planning tool for HNIs because it creates immediate, ring-fenced liquidity for selected beneficiaries. This can help a spouse, children, or dependents receive cash quickly while business interests, trusts, or property assets go through legal transfer. It can also reduce pressure to sell valuable assets in a hurry. In blended families or multi-heir estates, the payout may help balance inheritances and lower conflict risk. For many HNIs, term insurance adds clarity and speed during succession.

Is regular pay better than limited pay for HNI term insurance?

Many financially aware HNIs prefer limited pay or regular pay based on a cash flow strategy. Limited Pay allows premiums to finish in 5, 10, or 15 years while cover continues longer. This suits entrepreneurs with high current income or those who want no premiums near retirement. Regular Pay spreads cost across the policy term and keeps more capital free for business or investments. The better option depends on returns available elsewhere, future income visibility, and comfort with long-term payment commitments.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.