Overview

As of 2026, Maharashtra’s inflation stands at 3.07%, but in Mumbai, everyday expenses like rent, school fees, and transport continue to rise. This makes financial protection essential. Term insurance helps ensure your family can manage these costs if your income stops unexpectedly.

In the next few minutes, you will understand how term insurance fits into Mumbai’s financial reality, and how to buy one.

Top Term Insurance Plans in Mumbai

- Axis Max Life Smart Term Plan Plus: A balanced option with competitive pricing and useful features. Axis Max Life Smart Term Plan Plus offers health support services and a top-up option, where female policyholders can enhance their cover through the Lifeline Plus feature after the spouse’s demise. The plan includes critical illness cover for up to 64 illnesses over 20 years, along with a terminal illness benefit that provides an accelerated payout of up to ₹1 crore.

- HDFC Life Click 2 Protect Supreme Plus: The policy offers flexible cover-increase and payout options. HDFC Life Click 2 Protect Supreme Plus allows life stage boosts, so you can increase your cover after key milestones like marriage or childbirth without fresh underwriting. Nominees can also choose structured income payouts instead of a lump sum. The critical illness rider covers up to 60 illnesses for 15 years.

- ICICI Prudential iProtect Smart Plus: The term plan suits salaried professionals with changing needs. ICICI Prudential iProtect Smart Plus offers a premium break option that allows you to defer payments for up to one year. The plan also offers an instant partial payout of ₹3 lakh at claim intimation for higher cover options. ICICI Prudential iProtect Smart Plus offers an optional critical illness cover for 60 illnesses over 20 years, along with a waiver of premium and accidental disability riders for added protection.

- Bajaj Life eTouch II: The plan is a simple term product with flexible payout options and limited pay choices. Bajaj Life eTouch II includes a terminal illness benefit with an early payout of up to ₹2 crore. It also offers an inbuilt waiver of premium in case of accidental disability or terminal illness.

- Aditya Birla Sun Life Super Term Plan: The policy suits individuals with changing income patterns. Aditya Birla Sun Life Super Term Plan offers an optional accelerated critical illness benefit covering 42 illnesses, with up to 50% of the sum assured payable. It also includes a terminal illness benefit with an early payout of up to ₹1 crore for financial support.

To explore these plans in detail, check our guide on the best term insurance options.

Note: As the financial capital, Mumbai is home to major insurers like Life Insurance Corporation of India, ICICI Prudential Life Insurance, HDFC Life Insurance, and Aditya Birla Sun Life Insurance.

Why Do You Need Term Insurance in Mumbai?

- Mumbai’s Housing Costs Can Strain a Family’s Finances: Mumbai is one of India’s most expensive housing markets, with high property prices across suburbs like Malabar Hill and Bandra. Navi Mumbai recorded a sharp 45.8% annual increase, highlighting strong demand and growing property costs. For most families, a home loan becomes the biggest long-term commitment. If the primary earner passes away, Equated Monthly Installments (EMIs) continue without change. A term plan helps ensure the family does not face pressure to sell the home or downgrade their lifestyle.

- Rent and Daily Expenses Add Constant Pressure: Rent in Mumbai stays high, along with costs like groceries, transport, school fees, and household help. Even a large life cover can quickly be reduced when these monthly expenses continue without income. Term insurance helps the family manage daily life with stability during a difficult time.

- Daily Commute Risk is a Part of Mumbai Life: In Mumbai, long and crowded commutes are a daily reality. In 2023, 2,590 deaths were reported on suburban railway tracks. While travel is essential, the financial risk is real. A term plan helps your family stay secure if your income stops unexpectedly.

- High Income Still Comes with High Commitments: Mumbai offers strong career opportunities, but higher income usually comes with higher fixed costs. Families manage EMIs or rent, education expenses, and dependent parents. Financial security depends on how long the family can sustain life without that income, not just on salary level.

- Education and Lifestyle Need Long-Term Protection: In Maharashtra, schools without a fixed long-term fee structure can increase fees by up to 15%, with revisions allowed periodically. This makes education costs unpredictable. Children’s education and future plans need steady funding. A term plan ensures that schooling and higher education do not get disrupted due to loss of income.

- Nuclear and Migrant Families Need Strong Backup: Many families in Mumbai live without extended family support. In such cases, term insurance acts as a financial safety net that replaces income and protects long-term stability.

Did You Know?

How Much Term Insurance Cover Do You Need in Mumbai?

The right term insurance cover depends on your income, expenses, goals, and liabilities. Here is a simple example to help you estimate your needs.

For instance, monthly household expenses of ₹80,000 and a home loan of ₹1 crore can suggest a required cover of around ₹5.2 crore. This example is based on a 30-year-old (assuming married) living in Thane, and coverage up to age 65.

At Ditto, we estimate your ideal cover using the expense and liabilities replacement method. For a clearer idea, you can use our cover calculator to find an amount that fits your needs.

Take Note:

Premium Comparison for Top Term Plans in Mumbai

Note: These premiums apply to non-smokers in Mumbai (pin code: 400050) with a ₹2 crore cover up to age 70, without first-year discounts. They are indicative only, and actual premiums may vary based on underwriting, health profile, and insurer terms.

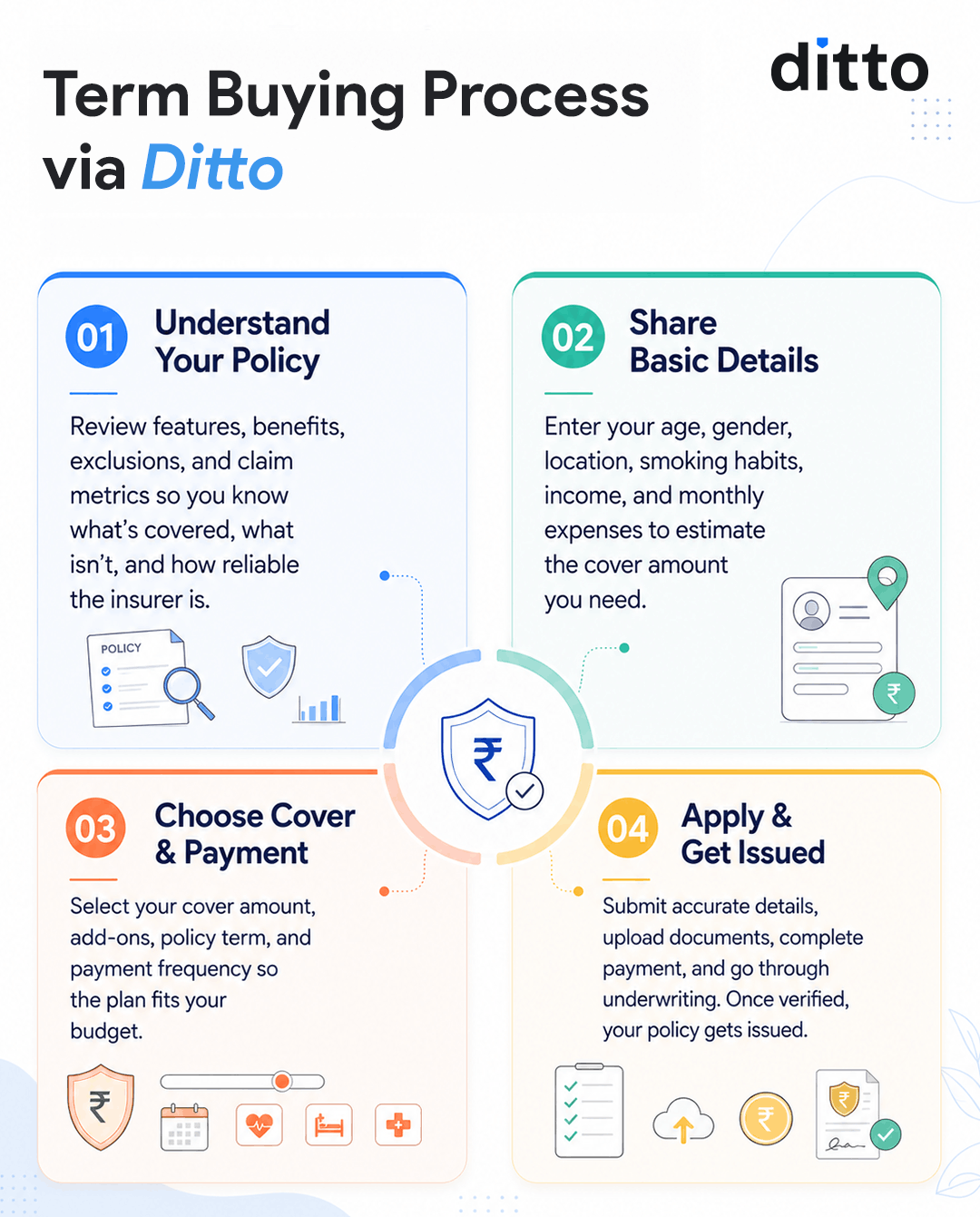

How to Buy Term Insurance in Mumbai via Ditto?

Buying term insurance online through Ditto is simple and consistent across cities. Not only do you get better pricing with online discounts, but you also get access to easy document upload and smooth tracking from purchase to policy issuance.

With Ditto, you pay the same premium as buying directly from the insurer, with no extra cost. Along with that, you get added guidance and dedicated help during claims and post-sales servicing. Connect with us to get started.

Check the infographic to understand how the process works.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Term insurance in Mumbai needs a practical approach. Expenses, loans, and income patterns vary across the city. The right plan is not just about buying cover. It is about choosing features that fit your life.

- Keep Your Cover Flexible: Increase your coverage after key events like marriage, childbirth, or buying a home. This keeps your protection aligned with your responsibilities.

- Plan for Income Disruption: Waiver of premium and critical illness cover support you if your income stops due to illness or disability. This is important for families with high fixed expenses.

- Stay Prepared for Cash Flow Changes: Options like premium break or premium holiday help you manage temporary income gaps during job changes or business slowdowns.

If you are considering term plans from established insurers, go through the best term insurance companies that offer strong claims support and long-term reliability.

Frequently Asked Questions

Last updated on: