SBI Life Smart Swadhan Supreme is a non-linked, non-participating Return of Premium (ROP) life insurance plan. It provides life cover during the policy term and guarantees a 100% refund of the base premiums paid if the policyholder survives to maturity. The plan offers coverage up to age 75, multiple premium payment options, and limited-pay variants, making it suitable for buyers who prefer a maturity benefit along with insurance protection.

However, ROP plans are typically 60% to 100% more expensive than comparable pure term insurance plans and can sometimes cost even more. Despite the higher premiums, the maturity benefit consists mainly of the policyholder's own money being returned without interest, bonuses, or investment growth.

This guide is ideal for buyers evaluating whether the premium refund feature justifies the additional cost.

What if you could buy life insurance and get your premium back if you outlive the policy term? That’s the promise behind SBI Life Smart Swadhan Supreme (UIN: 111N140V02), a Return of Premium (ROP) life insurance plan. For many buyers, this feature offers peace of mind by avoiding the feeling of “losing” money if no claim is made.

However, this reassurance comes at a price and in most cases isn’t worth it at all. This SBI Life Smart Swadhan Supreme review examines the plan’s key features, costs, benefits, and limitations. We’ll also compare it with pure term insurance alternatives to help you make the right choice.

If you’d like to compare SBI Life Smart Swadhan Supreme with other term plans, book a free call or WhatsApp us.

Key Features of SBI Life Smart Swadhan Supreme

Parameter

Details

Entry Age

18 to 60 years

Maximum Maturity Age

75 years

Sum Assured

₹25 lakh to no limit (subject to underwriting)

Policy Term

10 to 30 years

Premium Payment Options

Regular pay, limited pay (7 years, 10 years, or 15 years)

Premium Frequency

Yearly, half-yearly, and monthly

Maturity Benefit

100% of total base premiums paid, excluding taxes and rider premiums

Rider Available

Offers the SBI Life Accident Benefit Rider, which provides coverage through Accidental Death Benefit (ADB) and Accidental Partial Permanent Disability Benefit (APPD) options.

Note: Policy term availability varies based on the selected premium payment option. The loan facility is available only after the policy has acquired a surrender value.

Tax Benefits Under Section 80C and Section 10(10D)

Premiums paid towards SBI Life Smart Swadhan Supreme qualify for tax deductions under Section 80C of the Income Tax Act, 1961, under the old tax regime, subject to the overall deduction limit and applicable conditions.

Death benefits received by the nominee are exempt from tax under Section 10(10D). Maturity benefits also qualify for tax exemption under Section 10(10D), provided the policy satisfies the prescribed conditions, including applicable premium-to-sum-assured limits under prevailing tax laws.

Since tax treatment depends on policy features, premium amounts, and changes in tax regulations, buyers should consult a qualified tax advisor before making decisions based primarily on tax benefits.

Should You Buy Smart Swadhan Supreme?

The plan's key strengths are its guaranteed premium refund, simple structure, flexible premium payment options, and the backing of SBI Life Insurance. However, these benefits come at the cost of lower financial efficiency, limited rider options, a maximum policy term of 30 years, and substantially higher premiums. Moreover, the maturity benefit does not include any interest, bonus, or investment growth. By the time you get your money back, it will have lost value due to inflation.

Instead, at Ditto, we prefer pure term plans such as SBI Life Smart Shield Plus or Smart Shield Premier. A pure term insurance plan, paired with separate investments in options such as the Public Provident Fund (PPF), the National Pension System (NPS), or mutual funds, is usually a far more efficient way to achieve both protection and wealth creation.

Premium Comparison

The table below compares a ₹1 crore cover for a 30-year-old non-smoker with coverage up to age 60.

Profile

Smart Swadhan Supreme (ROP)

Smart Shield Plus (Pure Term)

Annual Premium Difference

Male, Age 30

₹26,472

₹11,266

₹15,206

Female, Age 30

₹22,284

₹9,548

₹12,736

Key Insights

SBI Smart Swadhan Supreme costs more than twice as much as Smart Shield Plus for the same ₹1 crore cover.

A 30-year-old male could accumulate approximately ₹12.02 lakh by investing the premium difference at 6%, versus a maturity benefit of ₹7.94 lakh under Smart Swadhan Supreme. For a female, the corresponding figures are ₹10.07 lakh and ₹6.69 lakh, respectively. This illustrates the opportunity cost of choosing the Return of Premium (ROP) option over a pure term plan.

Return of Premium vs Pure Term Insurance: Which Is Better?

Factor

Return Of Premium Plan

Pure Term Plan

Premium

Significantly higher

Lower

Life Cover

Available

Available

Maturity Benefit

Base premiums refunded

No survival payout

Investment Growth

Not available

Premium savings can be invested separately

Riders & Features

Usually limited

More comprehensive rider and feature options

Best Suited For

Buyers wanting a premium refund

Buyers seeking cost-efficient protection

Another limitation of many ROP plans, including SBI Life Smart Swadhan Supreme, is the lack of several modern term insurance features, such as:

Critical illness rider

Waiver of premium benefit

Health management services

Premium break options

Instant payout on claim intimation

The plan also comes with restrictions on policy term and maximum maturity age compared to several modern pure term plans.

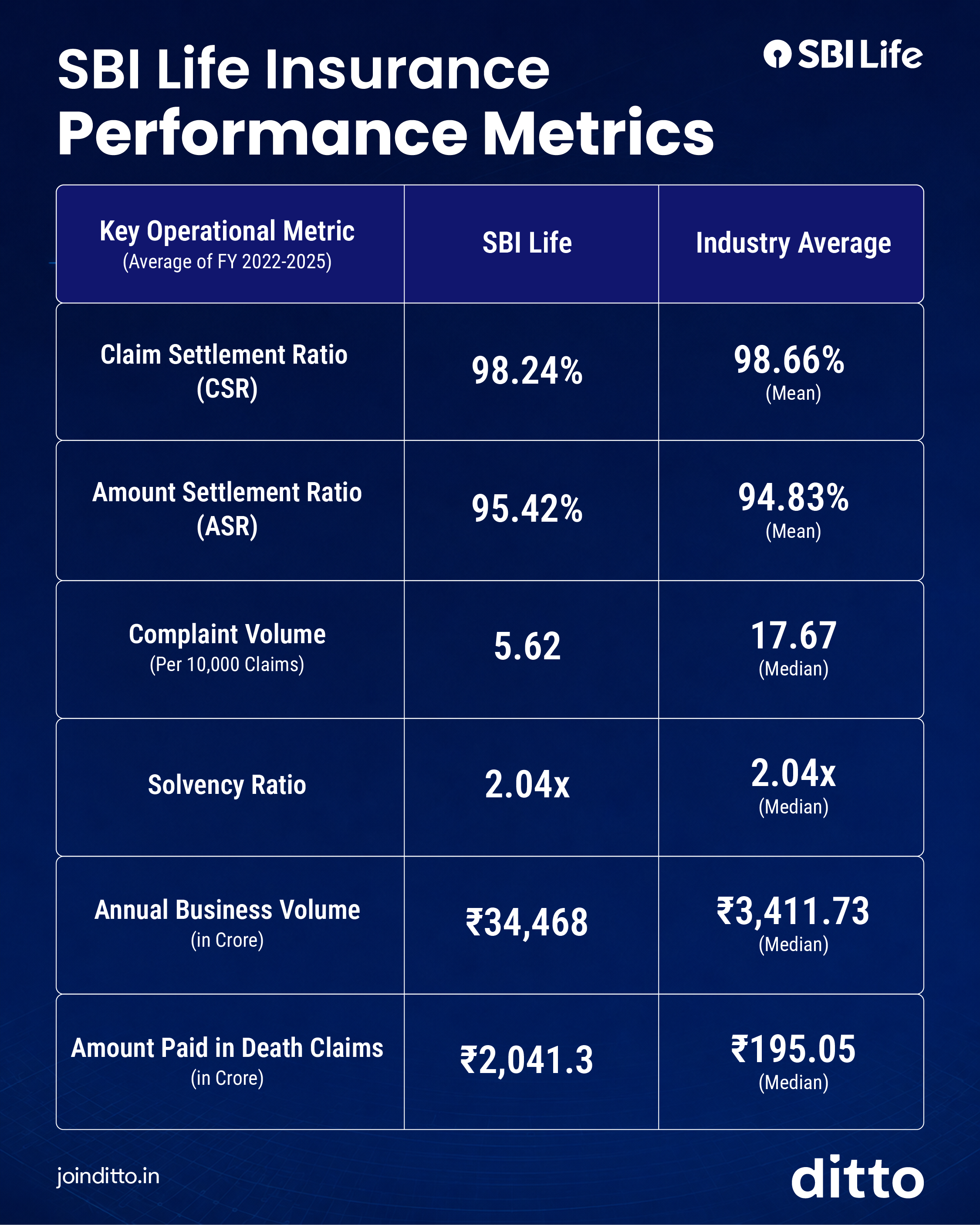

SBI Life’s Performance Metrics

Key Insights

SBI Life has maintained a strong claim settlement record, with steady improvement over the years.

Its Amount Settlement Ratio (ASR) is above the industry average, indicating balanced payouts across claim sizes.

Complaint levels are lower than those of many peers, reflecting a relatively smooth customer experience.

The insurer's solvency ratio comfortably exceeds the Insurance Regulatory and Development Authority of India (IRDAI) requirement of 1.5x, indicating sound financial strength.

SBI Life operates at a significantly larger scale than the industry median, indicating its established market position.

Note: These figures represent SBI Life's overall performance and are not specific to Smart Shield Plus, Smart Shield Premier, or any individual policy. Ditto uses 3-year averages for key metrics to minimize the impact of short-term fluctuations.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 22,000+ happy customers

While Smart Swadhan Supreme offers the psychological comfort of getting money back on survival, the trade-off is substantially higher premiums and limited potential for wealth creation. For buyers focused on maximizing protection, flexibility, and long-term financial value, pure term insurance remains the more practical choice. If you are looking for reliable long-term coverage, explore our guide on the best term insurance plans in India.

Frequently Asked Questions

What is SBI Life Smart Swadhan Supreme?

SBI Life Smart Swadhan Supreme is a non-linked, non-participating Return of Premium (ROP) plan from SBI Life Insurance. It provides life cover during the chosen policy term and refunds 100% of the base premiums paid if the policyholder survives till maturity. The plan is designed for buyers who want insurance protection along with a guaranteed maturity payout. However, the maturity amount does not include any bonus, interest, or market-linked returns. The plan offers flexible premium payment options, policy terms ranging from 10 to 30 years, and a maximum maturity age of 75 years.

Is SBI Life Smart Swadhan Supreme worth buying?

SBI Life Smart Swadhan Supreme may suit buyers who strongly prefer getting their premiums back at maturity. However, for most buyers, it is not the most cost-efficient option because premiums are significantly higher than those of pure term insurance plans. The maturity benefit primarily consists of the policyholder’s own premiums being returned, with no investment growth. In many cases, buying a pure term insurance plan and investing the premium difference separately in options like Public Provident Fund (PPF), National Pension System (NPS), or low-cost mutual funds can create much better long-term financial value and flexibility.

What is the maturity benefit under Smart Swadhan Supreme?

If the policyholder survives the entire policy term, SBI Life returns 100% of the total base premium paid as a lump sum maturity benefit. This excludes taxes, rider premiums, and extra underwriting charges. The maturity payout does not include any interest, loyalty additions, bonus, or market-linked growth. For this reason, the effective long-term return on the policy remains zero, unlike traditional investment products. While the guaranteed refund may appeal to conservative buyers, the purchasing power of the maturity amount will decline over time due to inflation and rising living costs.

What riders are available with SBI Life Smart Swadhan Supreme?

Smart Swadhan Supreme offers the SBI Life Accident Benefit Rider, which includes Accidental Death Benefit (ADB) and Accidental Partial Permanent Disability Benefit (APPD) options. The ADB option provides an additional payout if the life assured dies due to an accident, while the APPD option pays a benefit if the life assured suffers a specified partial permanent disability caused by an accident. However, the plan does not offer a critical illness rider, waiver of premium benefit, health management services, premium break options, or instant claim payouts. As a result, its protection features are relatively limited compared to many modern pure term insurance plans.

How does Smart Swadhan Supreme compare with SBI Life Smart Shield Plus?

SBI Life Smart Shield Plus is a pure term insurance plan designed to provide high life cover at a lower premium, whereas Smart Swadhan Supreme includes a Return of Premium (ROP) feature that significantly increases the cost. For example, a 30-year-old male seeking ₹1 crore cover till age 60 would pay approximately ₹11,266 annually under Smart Shield Plus compared to ₹26,472 under Smart Swadhan Supreme. At Ditto, we generally prefer Smart Shield Plus because it offers the same protection at a much lower cost, allowing buyers to invest the premium savings separately.

Is Return of Premium term insurance a good investment?

No, Return of Premium (ROP) term insurance should not be treated as an investment product. The maturity benefit returns the base premiums paid by the policyholder without any interest, profits, bonus, or market-linked growth. As a result, the long-term returns are poor compared to traditional investment avenues. Since ROP plans also charge substantially higher premiums than pure term insurance plans, Ditto advisors recommend avoiding them for wealth creation. A more efficient strategy is usually to purchase a pure term insurance plan and invest the premium savings separately in long-term assets with better return potential.

How expensive is Smart Swadhan Supreme compared to pure term plans?

Return of Premium (ROP) plans like SBI Life Smart Swadhan Supreme are typically 60% to 100% more expensive than comparable pure term insurance plans and can sometimes cost even more. For example, a 30-year-old male seeking ₹1 crore cover till age 60 would pay approximately ₹26,472 per year under Smart Swadhan Supreme compared to ₹11,266 per year under SBI Life Smart Shield Plus. Similarly, a 30-year-old female would pay around ₹22,284 versus ₹9,548. The additional premium mainly funds the maturity refund and does not increase the life cover. For most buyers, investing this premium difference separately is likely to create greater long-term value.

What is the death benefit under SBI Life Smart Swadhan Supreme?

If the life assured passes away during the policy term, the nominee receives a lump-sum death benefit. The payout will be the highest of the basic sum assured, 11 times the annualized premium, or 105% of the total premiums paid until the date of death. For example, if the policy has a ₹1 crore sum assured, the nominee will generally receive ₹1 crore, provided it is higher than the other applicable calculations. The death benefit is designed to provide financial security to the policyholder’s family and help them meet future financial obligations in the policyholder’s absence.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.