Overview

SBI Life Smart Swadhan Neo is a term plan that pays a death benefit to the nominee if the policyholder passes away. It also returns 100% of your total premiums paid if the person survives the policy term.

But is this benefit worth it in the long run? At Ditto, we usually prefer pure term plans because they offer higher cover at a much lower premium.

Let’s walk you through what Smart Swadhan Neo is, what it costs, and how it compares to other life insurance plans.

Key Features of SBI Life Smart Swadhan Neo

Premium Payment Term

You can pay premiums through a single payment, for a limited period (7, 10, 15 years), or throughout the policy term.

Flexibility

You can choose the policy term between 15 and 30 years.

Enhanced Protection

The optional accident benefit rider (accidental death + accidental partial permanent disability) pays a lump sum to the nominee if you die due to a covered accident or are diagnosed with an accidental disability.

Death Benefit

In the unfortunate event of the policyholder’s death during the policy term, the sum assured is paid to the nominee as a lump sum.

Maturity Benefit

100% of the total premiums paid during the policy term will be paid as a lump sum on the survival of the policyholder.

Eligibility and Plan Parameters

Should You Buy Smart Swadhan Neo

Opt for SBI Life Smart Swadhan Neo if you need:

- Simple product with a straightforward and easy-to-understand structure.

- 100% premium refund at maturity provides a psychological safety net for people who are uncomfortable with “losing” premiums.

- Accidental death benefit up to 3× the base sum assured and accidental partial permanent disability cover up to the base sum assured.

However, you should skip the plan if the following limitations bother you:

- The sum assured of ₹24.9 lakh is inadequate for most urban families that may need ₹1 crore or more in life cover.

- Premiums are significantly higher than a comparable pure term plan for the same cover (often more than 100%).

- The maturity benefit only returns your own money. There is no interest, profit, or capital gain.

- No critical illness rider or modern term plan features such as health management services or premium breaks.

What Are Return of Premium (ROP) Plans in Term Insurance?

A Return of Premium (ROP) plan is a variant of term insurance in which the insurer refunds all premiums paid if the policyholder survives the full policy term. Smart Swadhan Neo is a pure ROP plan with no pure protection variant available within the same product. If you want life cover from SBI Life without the ROP structure, you need to look at a different product entirely.

Return of Premium vs Pure Term Insurance: Which Is Better?

At Ditto, we do not recommend term plans with ROP because they can cost 60% to 100% more than a regular term plan.

Premium Comparison: ROP vs Pure Term

Here, PA stands for per annum, PPF denotes Public Provident Fund, and NPS denotes the National Pension System. Premiums are indicative and vary based on the profile, sum assured, and policy term.

Note: With a pure term plan, you can invest the premium difference separately in options like PPF, NPS, or mutual funds. The ROP plan only returns your premiums with no real growth. In this case, you also get 4x higher life cover, and if the ₹5,900 yearly difference is invested at a simple 6% FD return, it can grow to about ₹4.9 lakh, roughly matching the ROP maturity amount.

Smart Swadhan Neo vs Smart Swadhan Supreme: How Do They Compare?

Takeaway: Smart Swadhan Neo has a fixed cover cap of ₹24.9 lakh, making it weak for income replacement. Smart Swadhan Supreme removes this cap but comes with much higher premiums. Both plans have the accident benefit rider but do not offer the critical illness or waiver of premium riders.

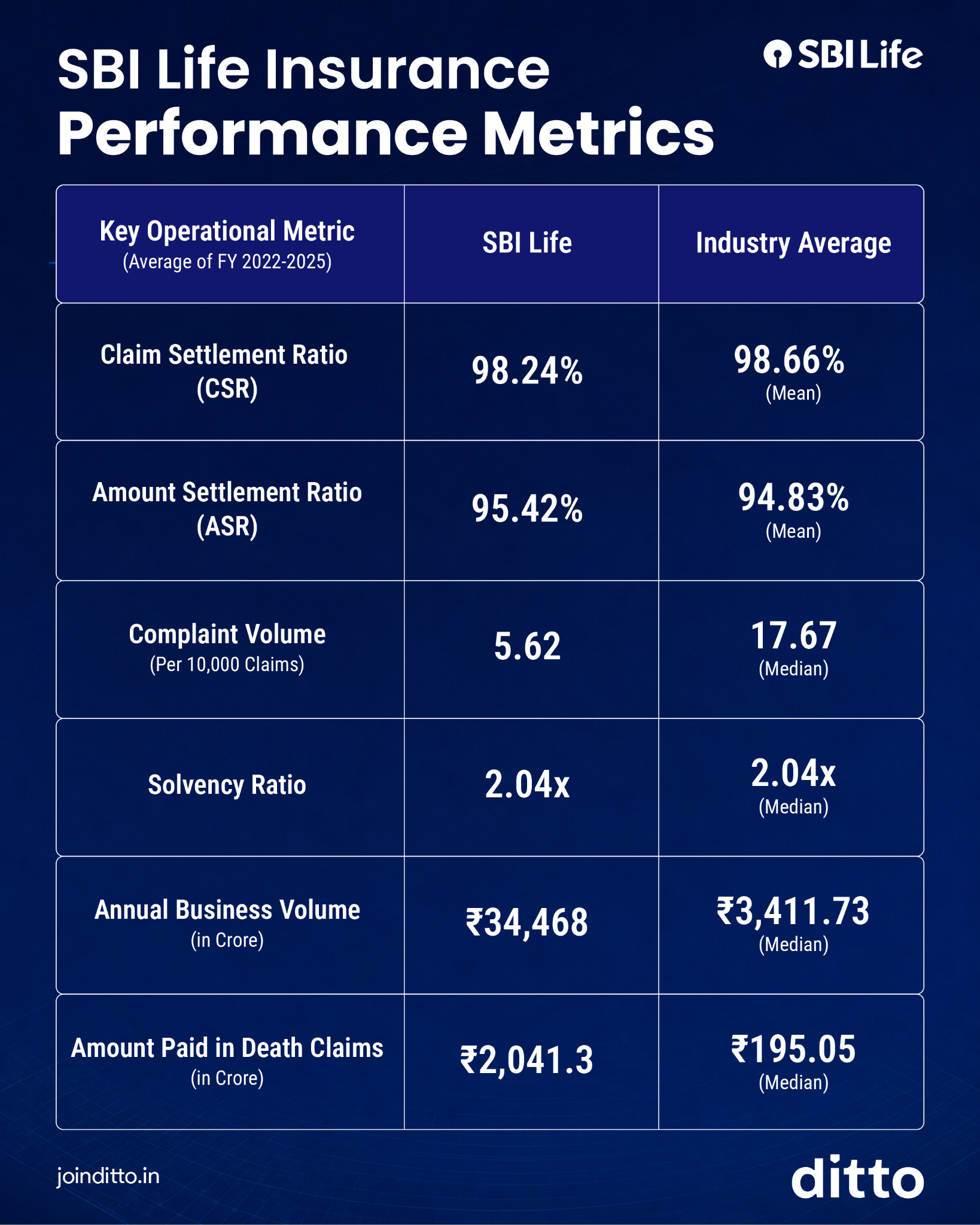

SBI Life: Performance Metrics

SBI Life demonstrates strong operational scale, healthy claims-paying ability, and relatively low complaint levels, supported by adequate solvency. Take a look at the infographic below to learn more about its performance metrics.

For details, refer to our review of SBI Life Insurance.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

SBI Life Smart Swadhan Neo is a straightforward product that provides a life cover during the term, and a full premium refund if you survive it.

However, the maximum sum assured of ₹24.9 lakh falls far short of what most families need for meaningful income replacement. Premiums are higher than pure term plans offering 4× the coverage. And the maturity benefit offers no real return.

At Ditto, we believe the first step towards financial protection is always an adequate life cover at the lowest possible cost. A pure term plan covers that. Education, retirement, emergency savings, and other goals are better handled through PPF, NPS, FDs, or mutual funds, where your money can grow.

If you prefer staying within the SBI Life ecosystem, SBI Life Smart Shield Plus and Premier deliver more meaningful coverage, modern features, and honest pricing.

Frequently Asked Questions

Last updated on: