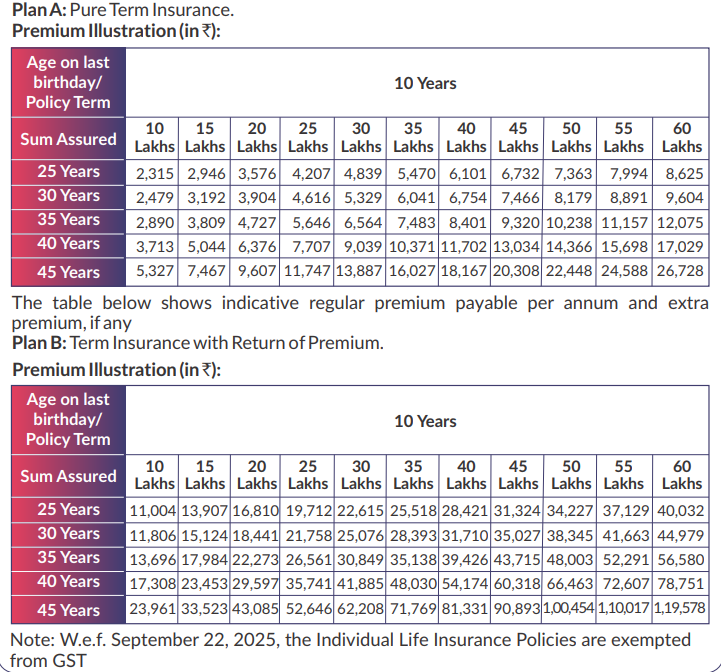

SBI Life eShield Insta is a digital, non-linked, non-participating term insurance plan for quick, paperless, and digital purchase. It caters to individuals aged 18 to 50 years and offers options for pure protection or return of premium if the policyholder survives the term. A 25-year-old male non-smoker opting for a ₹60 lakh cover under Plan A (Pure Term) until 10 years pays approximately ₹8,625 per year.

Additionally, SBI Life's three-year average CSR stands at 98.24% (FY 2022–25), reflecting strong and consistent claims performance.

This guide on SBI Life eShield Insta details is for first-time buyers, SBI brand loyalists, and digitally savvy buyers who want a no-frills term plan.

Buying term insurance is usually about one simple question: if something happens to you, will your family have enough money to continue their life without any financial stress?

That is where SBI Life eShield Insta comes in. It is built as a quick, digital protection plan, not a feature-heavy term policy. Think of it as a basic safety net. You get life cover for 10 years, choose between pure protection and return of premium, and pay premiums yearly or monthly.

But here’s the real question: is SBI Life eShield Insta good enough for your family’s long-term protection needs? Let’s break it down.

SBI Life eShield Insta is a non-linked, non-participating pure term insurance product with a return of premium option. Unlike most comprehensive private term plans which come with a long list of variants, various in-built features, and optional riders, eShield Insta keeps things deliberately simple.

It offers a clean digital onboarding process and a fixed 10-year premium payment term. The SBI Life eShield Insta plan offers two options. Plan A is Pure Term Insurance, under which only a death benefit is payable. Plan B is Term Insurance with Return of Premium (ROP). This means if the life assured survives till the end of the policy term and the policy is in force, 100% of the total premiums paid (total premiums under the base product, excluding any extra premium and taxes, if collected explicitly) will be refunded as a maturity benefit.

Once you choose the plan option at inception, you cannot change it during the policy term.

Please Note: At Ditto, we do not recommend ROP plans because they generally cost 80-100% more in premiums compared to regular, pure term insurance plans, providing lower value for the money spent.

CTA

Key Features, Benefits and Coverage Options

Key Features and Coverage

Parameter

Details

Entry Age

Minimum: 18 years, Maximum: 50 years

Maximum Age at Maturity

60 years

Policy Term

10 years

Premium Payment Term

Regular pay

Premium Payment Frequency

Yearly or monthly

Minimum Sum Assured

₹10 lakh

Maximum Sum Assured

₹60 lakh (based on underwriting)

SBI Life eShield Insta Benefits

Death Benefit

On the death of the life assured during the policy term, the sum assured is paid to the nominee or legal heir, and the policy terminates. The sum assured on death is the highest of: the sum assured, 11 times the annualized premium, or 105% of the total premium paid up to the date of death. This structure ensures the nominee always receives a meaningful payout, regardless of how early the death occurs during the policy term.

Maturity Benefit (Plan B Only)

If the life assured survives till the end of the policy term and the policy is in force, 100% of the total premiums paid will be refunded as a maturity benefit under Plan B. Note that this refund excludes taxes and extra premiums, which is standard across all return of premium plans in India.

Policy Loan

Under Plan A, no loan facility is available. Under Plan B, a loan can be taken out during the policy term, provided the policy has acquired a surrender value. The maximum loan amount can not exceed 50% of the surrender value.

Tax Benefits

Premiums paid under eShield Insta are eligible for deductions under Section 80C of the Income Tax Act (up to ₹1.5 lakh per year under the old tax regime). The death benefit payable to nominees is tax-exempt under Section 10(10D). Effective September 22, 2025, individual life insurance policies are exempt from GST, which directly reduces your annual premium cost.

Did You Know?

If the life assured passes away due to suicide within 12 months from the policy commencement or revival date, the nominee or beneficiary will receive a limited payout. The payout in such cases is 80% of the total premiums paid till the date of death.

Premium Calculator: How Much Will It Cost?

There is no separate SBI Life eShield Insta premium calculator available on SBI Life's official website. However, SBI offers a dedicated term insurance calculator to help you get premium quotes.

It requires details such as your name, age, gender, occupation, education, location, and contact information. The process takes under 2 minutes and requires no document submission at the quoting stage.

Meanwhile, here are the illustrative premiums for both plan variants of SBI Life eShield Insta as shown in the product brochure.

Note: All sample premiums are exclusive of taxes and underwriting charges. Your actual premium will depend on your specific health profile, income, and the underwriting outcome.

Should You Buy SBI Life eShield Insta?

SBI Life eShield Insta is a decent product for a specific type of buyer. It is not the most feature-rich term plan on the market, but it delivers clearly on what it promises. Here is how to decide.

SBI Life eShield Insta is a decent entry-level term plan that does its core job: providing affordable life cover in a fast, digital process. If you are a younger buyer seeking comprehensive, future-proof coverage for ₹1 crore or more, you will outgrow this plan quickly. But if you need quick, basic cover tied to SBI Life's brand credibility, eShield Insta delivers that without friction.

If you are comparing eShield Insta specifically against SBI Life's broader portfolio, Smart Shield Plus offers additional flexibility, including expanded cover options and rider benefits. For buyers willing to look outside SBI Life, Axis Max Life Smart Term Plan Plus and HDFC Life Click2Protect Supreme Plus offer significantly richer features, such as critical illness cover, waiver of premium, zero-cost exit options, at comparable or only marginally higher premiums. For more details, refer to our guide on the best term plans in India.

Frequently Asked Questions

What is SBI Life eShield Insta and how does it work?

SBI Life eShield Insta is a digital term insurance plan that offers life cover for a fixed 10-year policy term. It is non-linked and non-participating, meaning your premium does not depend on market performance. You can choose between two options: Plan A (Pure Term), which pays a death benefit to your nominee, and Plan B (Term with Return of Premium), which refunds 100% of premiums paid if you survive the term. The entire purchase process is paperless and cashless, making it one of the faster term plans to buy online.

What is the sum assured limit for SBI Life eShield Insta?

The minimum sum assured under SBI Life eShield Insta is ₹10 lakh, and the maximum is ₹60 lakh, subject to underwriting. This makes it suitable for buyers who need basic life cover rather than comprehensive, high-value protection. If you need coverage of ₹1 crore or more, you will need to look at other term insurance plans. At Ditto, we generally recommend that buyers consider their long-term income-replacement needs before settling for a lower coverage cap. In short, SBI Life eShield Insta can work as an entry-level term cover, but it may fall short for families that need meaningful income replacement over the long term.

Who is eligible to buy SBI Life eShield Insta?

SBI Life eShield Insta is available to individuals aged 18 to 50. The maximum age at policy maturity is 60 years, and the policy term is fixed at 10 years. There is no option to extend coverage beyond age 60 under this plan. If you are in your 30s or 40s and need protection into your 60s or 70s, this plan will fall short. Younger buyers looking for short-term cover while they plan their finances may find it a practical starting point.

How much does SBI Life eShield Insta cost for a 25-year-old?

A 25-year-old male non-smoker opting for ₹60 lakh cover under Plan A (Pure Term) for a 10-year term pays approximately ₹8,625 per year. Premiums vary based on age, health profile, income, and the plan option chosen. Plan B (Return of Premium) costs significantly more. At Ditto, we recommend sticking with pure term plans since ROP variants typically cost 80 to 100% more in premiums while delivering lower overall value for the money you spend.

Should I choose Plan A or Plan B in SBI Life eShield Insta?

Plan A is pure term insurance, where no benefit is paid if you survive the policy term. Plan B returns 100% of total premiums paid at maturity if you survive. While Plan B sounds appealing, at Ditto, we do not recommend return of premium plans because they cost 80-100% more than a regular term plan. That extra premium, if invested separately, could generate far better returns. Pure term insurance gives you maximum life cover at the lowest cost, which is what term insurance is actually meant to do.

What is the claim settlement ratio of SBI Life for eShield Insta?

SBI Life Insurance has a three-year average claim settlement ratio (CSR) of 98.24% for FY 2022 to 2025, reflecting strong and consistent claims performance. This is one of the highest CSRs among private life insurers in India and is an important factor when evaluating any term plan. At Ditto, we rate term plans on CSR, rider availability, premium competitiveness, and claims transparency. A high CSR means there is a greater likelihood your nominee's claim will be honored without unnecessary hassle.

Does SBI Life eShield Insta have any riders or add-on benefits?

No, SBI Life eShield Insta does not offer any riders like critical illness cover, waiver of premium, or accident benefits. This is one of its key limitations compared to comprehensive term plans. If you want riders, you will need to consider other plans like SBI Life Smart Shield Plus, Axis Max Life Smart Term Plan Plus, or HDFC Life Click2Protect Supreme Plus. At Ditto, we generally advise buyers who need broader protection to opt for plans that at least include a critical illness or waiver-of-premium rider.

Are the premiums for SBI Life eShield Insta tax-deductible?

Yes, premiums paid under SBI Life eShield Insta are eligible for a tax deduction of up to ₹1.5 lakh per year under Section 80C of the Income Tax Act, applicable under the old tax regime. The death benefit paid to the nominee is also tax-exempt under Section 10(10D). Additionally, effective September 22, 2025, individual life insurance policies are exempt from GST, which directly reduces your annual premium outgo. These tax benefits apply to both Plan A and Plan B variants of the policy.

What happens if I miss a premium payment in SBI Life eShield Insta?

SBI Life eShield Insta offers a grace period for premium payments, which is standard across most term insurance plans. The timeline is generally 30 days for yearly payment modes and 15 days for monthly modes, respectively. If the premium is not paid within the grace period, the term policy may lapse, and you could lose your life cover. Since the policy term is only 10 years with regular premium payments, consistent payments are important to keep the plan active.

How does SBI Life eShield Insta compare to other term plans in India?

SBI Life eShield Insta is a good entry-level digital term plan, but it has notable limitations: coverage is capped at ₹60 lakh, the term is fixed at 10 years, and there are no riders or in-built features. Plans like Axis Max Life Smart Term Plan Plus and HDFC Life Click2Protect Supreme Plus offer ₹1 crore or more in coverage, optional critical illness riders, waiver of premium, and various in-built features at comparable premiums. At Ditto, we recommend evaluating your long-term protection needs before choosing SBI eShield Insta, especially if you are the primary earner in your household.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.