Quick Overview

For many ICAI members, the real challenge isn’t whether they need term insurance but whether the ICAI scheme is enough for them. Most available information is scattered, technical, or hidden inside official documents, making objective evaluation difficult.

At Ditto, we reviewed the official ICAI details, insurer’s policy documents, and ICAI annual reports. In this blog, we break down what the ICAI term insurance scheme covers, its key limitations, and whether it’s sufficient on its own or needs to be supplemented with an individual term plan.

Available Insurance Products for ICAI Members

- ICAI HDFC Term Insurance (Group Poorna Suraksha): Term life cover with special group benefits for ICAI members.

- ICAI LIC Term Insurance: Group term life insurance providing life cover at competitive premiums.

Apart from term insurance, ICAI also offers medical insurance, professional indemnity insurance, motor vehicle insurance, personal accident policy, householder insurance, and office protection shield.

These services are facilitated through tie-ups with LIC, HDFC Life, and New India Assurance, allowing members to benefit from improved coverage options and preferential pricing.

Who is Eligible for ICAI Term Insurance?

Eligibility is subject to ICAI membership status and insurer underwriting rules.

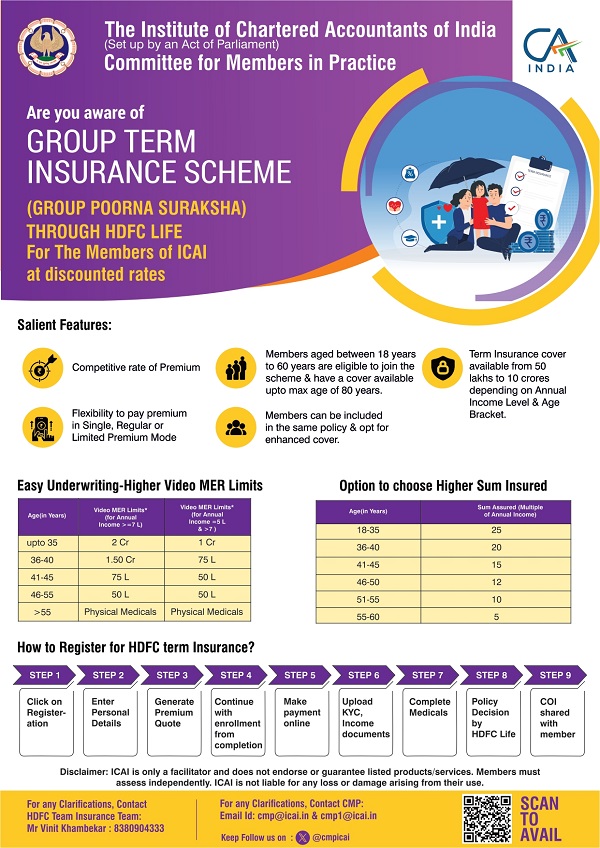

1) HDFC Group Poorna Suraksha Term Insurance

- Entry age: 18 to 60 years

- Maximum maturity age: 80 years

- Available only to eligible ICAI members under the group scheme

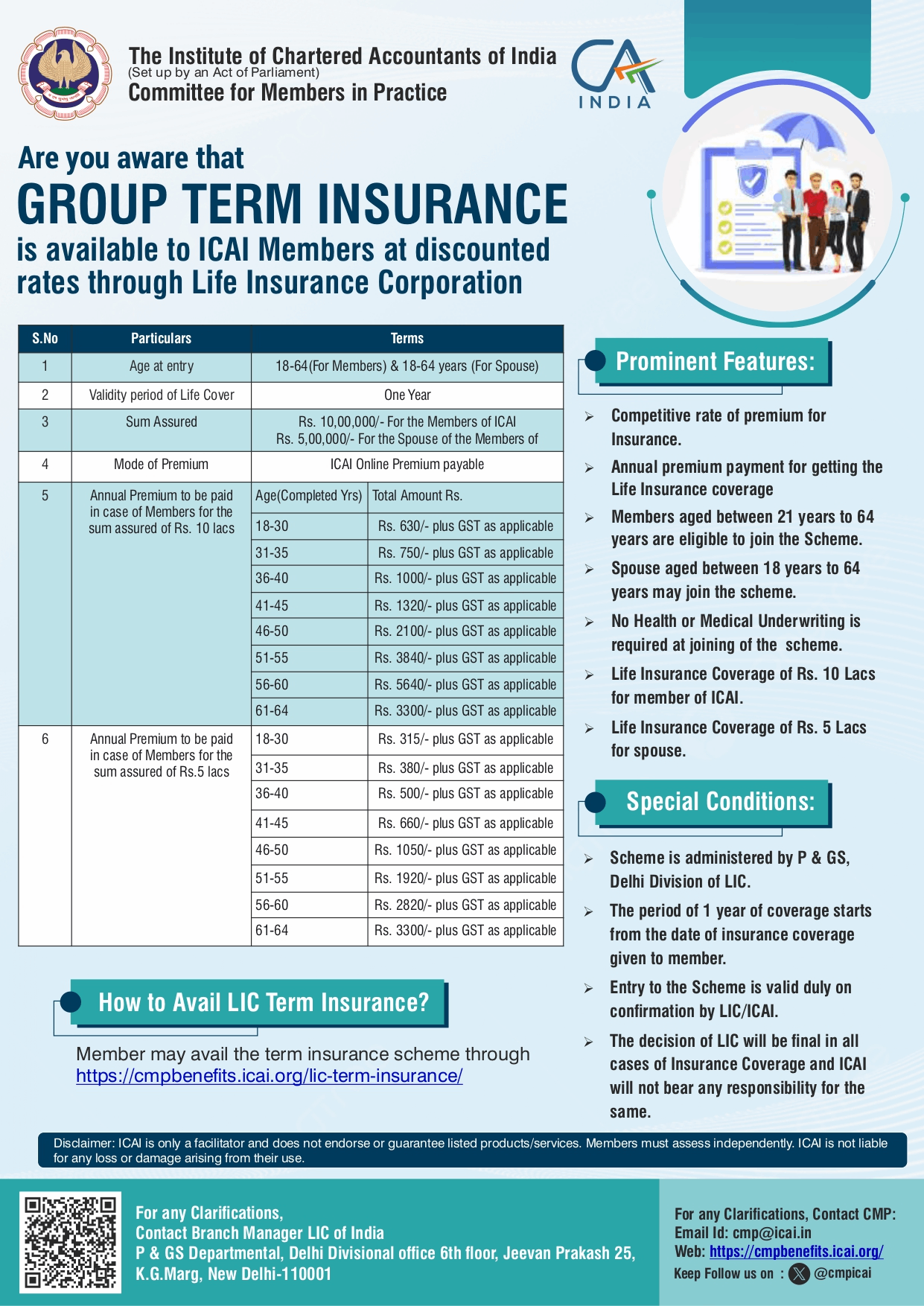

2) LIC Term Insurance

- Entry age: 18 to 64 years (as on last birthday)

- Available to active ICAI members and their spouses

Features and Benefits of the ICAI Term Insurance Scheme

1) HDFC Group Poorna Suraksha Term Insurance

- The death benefit is payable to the nominee in case of the insured member’s demise.

- An optional accelerated critical illness benefit rider is also available.

- Flexible premium payment option where you can choose from single pay, regular pay, or limited pay (5/10/12/15 years).

- The sum assured can range from ₹30 lakhs to ₹1 crore or more (depending on underwriting)

- The nominee can opt for a lump sum or installment payouts of 5-15 years.

2) LIC Term Insurance

- The sum assured is ₹10 lakhs for members and ₹5 lakhs for members’ spouses.

- You get life cover under a group term policy.

- The premiums are highly competitive (due to the group structure).

- Insurance is issued for one year at a time with the option to renew at the end of the policy period.

- There is no medical underwriting required (but the applicant should be healthy to be eligible)

What is Covered and Not Covered in ICAI Term Insurance?

Note: This coverage applies only as long as the policy is active, premiums are paid, and the member continues to meet scheme conditions.

ICAI Term Insurance Premium

Premiums are generally lower than individual term plans due to group pricing. However:

- Rates can change at renewal

- Premiums are not locked in for life

- Long-term predictability is limited

1) HDFC’s Premium Chart

The premium is calculated using the member’s age, opted sum assured, and chosen premium payment term.

2) LIC Premium Chart

For Members (₹10 Lakh Cover)

For Spouse (₹5 Lakh Cover)

How to Apply for ICAI Term Insurance?

- Visit the ICAI CMP Benefits portal

- Choose the preferred insurer (LIC or HDFC Life) and fill out the application form

- Complete required documentation and medical requirements (if applicable)

- Pay the premium directly to the insurer.

ICAI Term Insurance vs Individual Term Insurance

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion: Is ICAI Term Insurance Enough?

ICAI term insurance is a good starting point and works well as an affordable additional layer of protection or as temporary, supplementary cover for members. However, it should not replace an individual term insurance plan, especially if you have dependents, ongoing loans or liabilities, or long-term income replacement needs.

Disclaimer (as given on the ICAI website): All services are delivered directly by respective providers. ICAI does not endorse or guarantee the quality, reliability, or accuracy of these offerings. Members are advised to exercise independent judgment and due diligence before availing any product or service. ICAI shall not be liable for any loss or damage arising from its use.

Full Disclosure: Ditto has no affiliation with the ICAI, and all the information mentioned in the article is for informational purposes only. We would recommend verifying all the details from the institute and the respective insurers directly.

Frequently Asked Questions

Last updated on:

{kind=link}

{kind=link}