Overview

Estimating the right premium for your term insurance cover can be confusing. How much cover do you actually need? And how much will it cost you?

That’s where HDFC Life’s premium calculator helps. Enter your age, income, and desired cover amount, and you can quickly estimate how much premium you’ll pay for a specific level of life insurance coverage.

The tricky part is knowing what inputs to use and how each one affects the final premium. That’s exactly what this guide will help you understand.

How to Use the HDFC Life Term Insurance Calculator?

Using the HDFC Life Term Insurance Calculator is straightforward. Follow these steps:

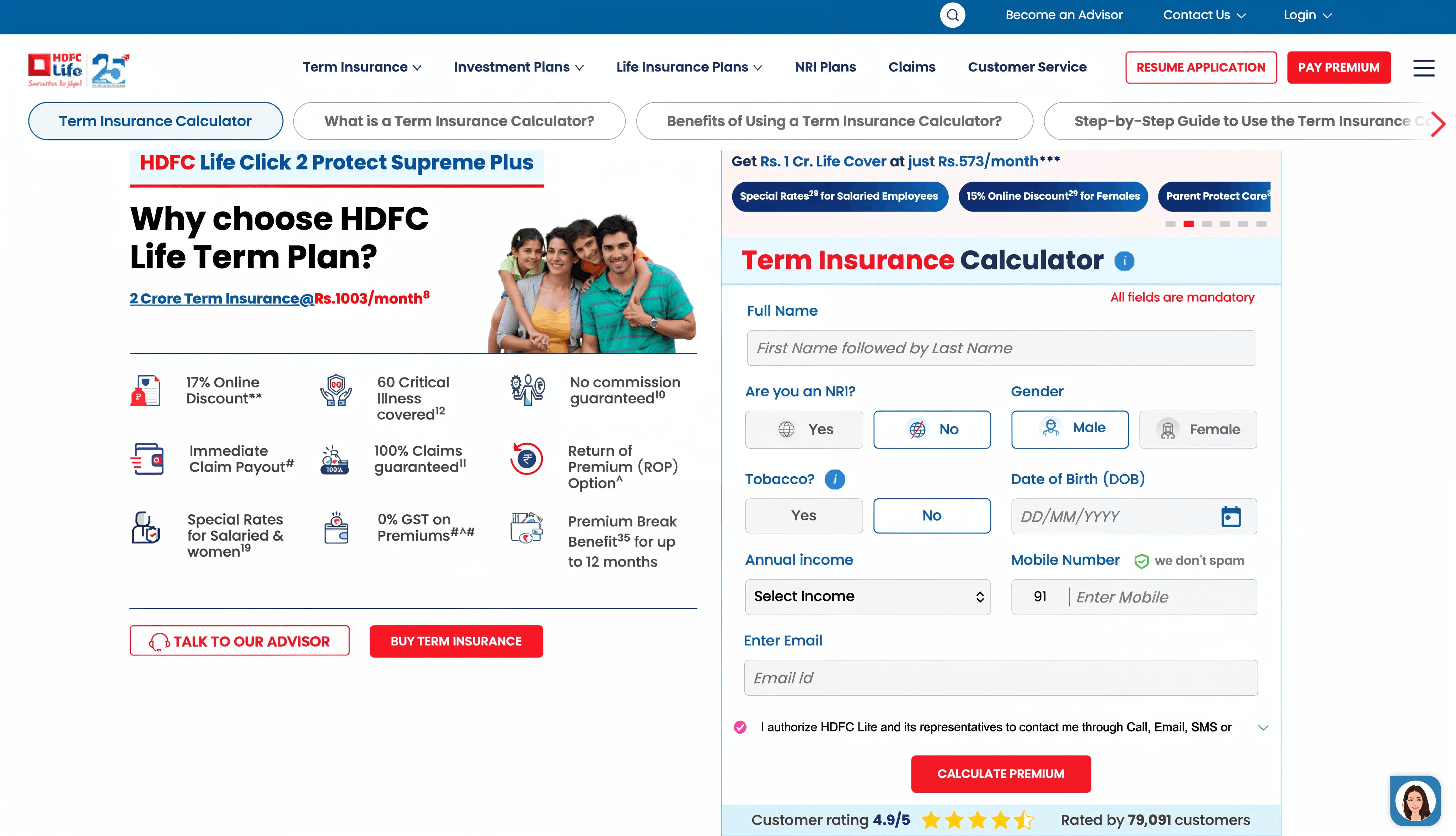

Step 1: Visit the HDFC Life website.

Step 2: Click on the ‘Term Insurance Calculator’ tab.

Step 3: Enter your basic details, including your full name, date of birth, residential status, mobile number, and annual income. Click on 'Calculate Premium.'

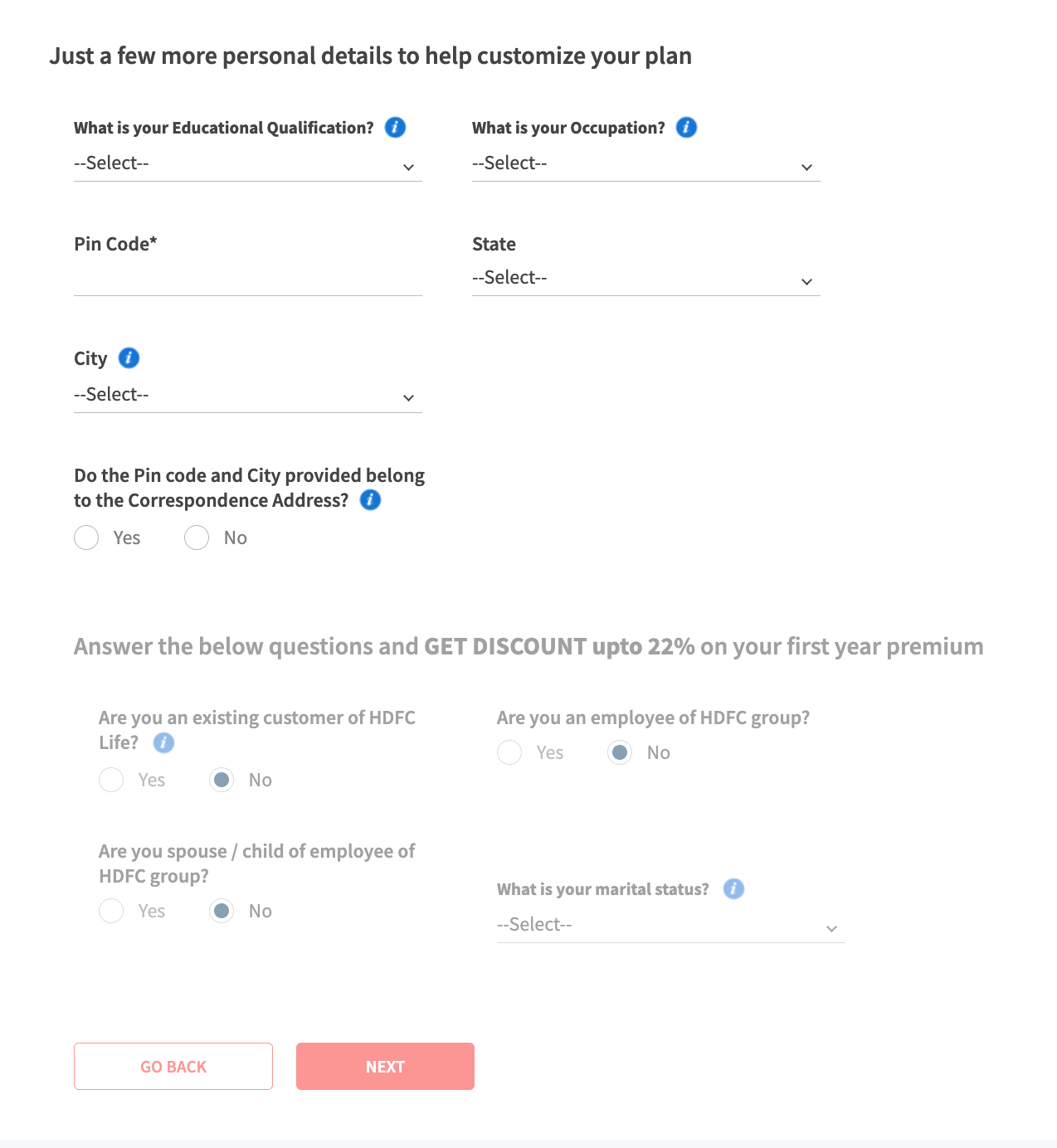

Step 4: You'll then be asked to fill in a few more personal details: your educational qualification, occupation, pin code, state, and city. You'll also need to answer whether the PIN code and city belong to your correspondence address.

Step 5: This page also has a discount section. Answer a few quick questions, such as whether you're an existing HDFC Life customer, an HDFC group employee, or a spouse/child of one, along with your marital status. Answering these can get you a discount of up to 22% on your first year's premium.

Step 6: Enter your preferred life cover (sum assured), policy term, premium payment term, and payment frequency to see your base premium.

Step 7: Once you have the base premium, you can explore available riders and see how they affect the final amount.

Note: Once you share your contact details, expect follow-up calls from the insurer.

Factors That Affect Your HDFC Life Term Insurance Premium

1. Age: The earlier you buy, the less you pay. Insurers price younger applicants lower because they're seen as less risky, and your premium stays locked in once you've bought the plan. Waiting even a few years can make a noticeable difference to what you end up paying.

2. Sum Assured: A higher cover means a higher premium, but the two don't scale equally. Before picking a number, think about your outstanding loans, future expenses, and how inflation might affect your family's needs. If you're unsure, Ditto's cover calculator can help you land on a reasonable figure.

3. Policy Term: Covering yourself until 60 or 70 works well for most people since that's roughly when dependents become financially independent and income stops. If you opt for a longer term, say until 85 or whole life, expect to pay more as insurers factor in the increased likelihood of a claim.

4. Smoking Status: If you smoke or use tobacco, your premium can be 50% higher or more compared to a non-smoker. To put that in perspective, a 25-year-old male smoker could pay around ₹18,000 a year for a ₹1 crore cover until age 65.

5. Health Conditions: Conditions like diabetes, high blood pressure, or obesity can raise your premium or lead to additional underwriting requirements. Most insurers will ask for medical tests before finalizing your policy.

6. Riders: Riders can meaningfully improve your coverage, but they do add to your premium, so only pick what you actually need. At Ditto, we usually suggest a critical illness rider for the lump sum payout on diagnosis and a waiver of premium rider so your policy stays active even if you're unable to pay due to a permanent disability or listed illness.

Note: How you pay also matters. Annual payments tend to be more cost-effective than monthly ones, so that's what we usually recommend at Ditto.

Sample HDFC Term Insurance Premiums by Age and Cover

Note: As you age, your annual premiums increase sharply, even though your policy term reduces. Despite fewer years of coverage, the total premiums paid remain similar or even higher, which is why buying early is more cost-effective.

These premiums are for a non-smoker male opting for a ₹1 crore cover under the HDFC Life Click 2 Protect Supreme Plus plan until age 60, residing in Delhi. They're illustrative, and your actual premium will vary based on the factors discussed above.

The calculator quote is not the final approved premium. HDFC Life may revise the premium after reviewing your medical history, income documents, lifestyle disclosures, occupation, and test reports.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat with us on WhatsApp!

Is HDFC Life Click 2 Protect Supreme Plus the Right Plan for You?

HDFC Life Click 2 Protect Supreme Plus is one of Ditto's top recommendations for term insurance. The plan gives you a lot of room to customize, so you're not stuck with a rigid structure that may not fit your situation. Here's why it stands out:

- High claim settlement ratio (99.55% for FY 22-25)

- Low complaint volume (1.33 per 10,000 claims for FY 22-25)

- Flexible plan structure with multiple customisation options

- Family-first design with strong continuity features

- Backed by one of India's most established and operationally reliable insurers

It does cost a little more than some competing plans. But that higher premium reflects what you're actually getting: a credible insurer with a strong claim track record and the reliability that matters when your family needs to file a claim. At Ditto, we think that peace of mind is worth paying for.

That said, the right plan depends on your specific needs, budget, and health profile. Check out our guide to the best term insurance companies in India to compare your options before deciding.

Frequently Asked Questions

Last updated on: