Quick Overview

What if your life insurance could protect your family today and still leave behind a lasting legacy? HDFC Life Sanchay Legacy is designed to do exactly that. It offers lifelong protection with the option to get your premiums back. This guide breaks down the benefits and drawbacks of HDFC Life Sanchay Legacy.

HDFC Life: Performance Metrics

Key Insights:

- The insurer offers strong CSR compared to the industry average, which indicates reliability in honoring claims. HDFC Life also ranks among the top insurers by claim settlement ratios.

- A high ASR suggests that the insurer treats high and low value claim settlements fairly.

- The insurer offers good customer service with significantly lower complaint levels.

- A much larger business scale, around 10 times the industry average, shows strong market presence and customer trust.

- Slightly lower solvency position compared to industry median, but still above IRDAI requirement of 1.5x.

HDFC Life Sanchay Legacy: Key Details

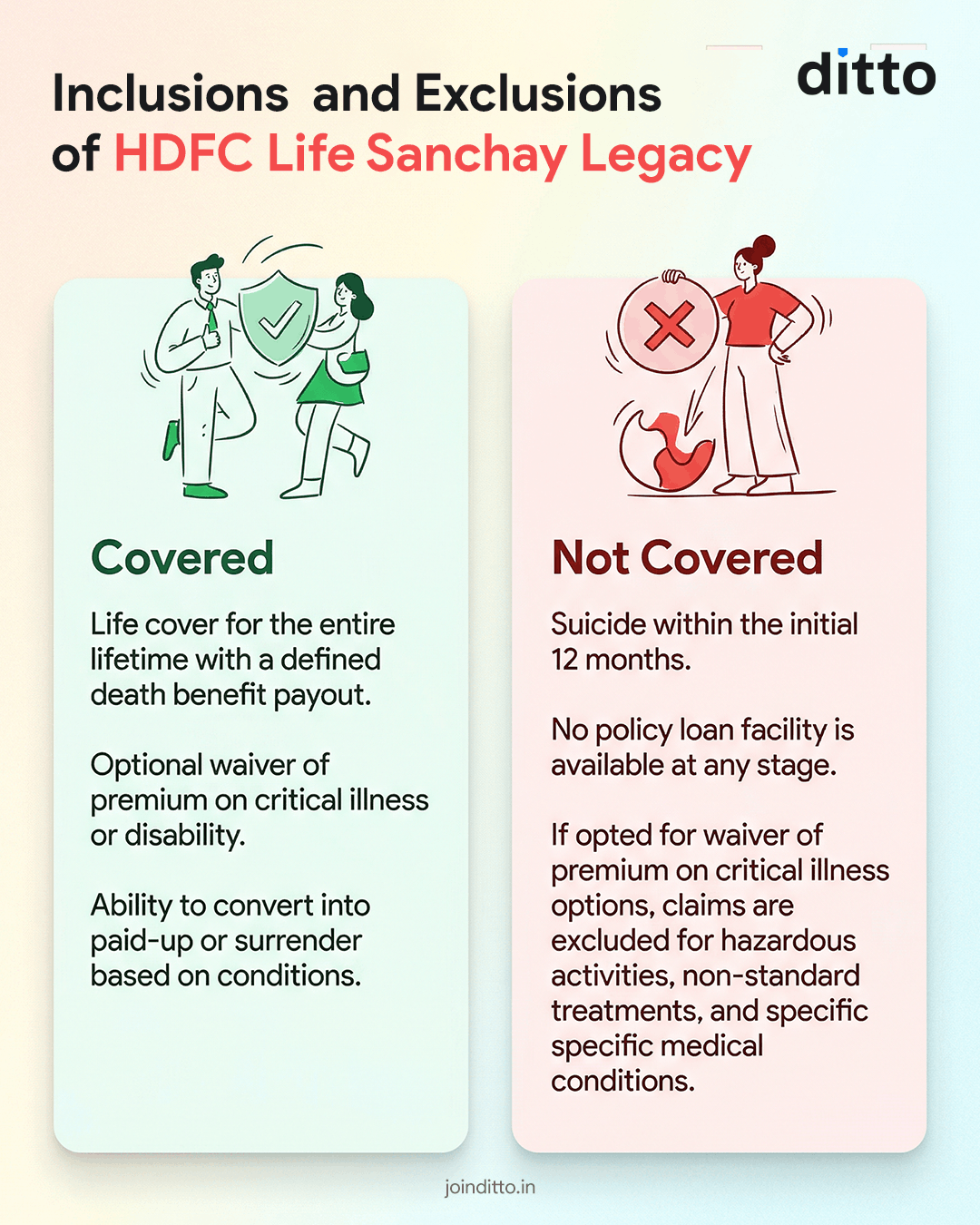

Take a look at the infographic below to understand what is covered and not covered under the plan.

Key Benefits of HDFC Life Sanchay Legacy

Legacy Planning

This is a whole-life plan designed for long-term wealth transfer. It stays active for your lifetime and ensures your family receives a financial legacy.

Strong Death Benefit

The payout is calculated as the highest of multiple values, which adds an extra layer of protection and ensures your nominee receives a meaningful amount.

Flexible Payout

Your nominee can choose how to receive the claim. They can take it as a lump sum or spread it over 5 to 15 years. This helps your family to manage daily expenses in a better way.

Continuity Features

The plan allows you to reduce premiums after five years if needed, which can help during financial stress. Optional waiver benefits ensure the policy continues even if you face any critical illness or disability.

Drawbacks of HDFC Life Sanchay Legacy

- Not a Low-Cost Plan: This plan comes with relatively high premium commitments and starts at a later entry age.

- Critical Illness Features can Mislead: The critical illness benefit is not an additional payout. It simply gives early access to the death benefit. This can reduce the final payout to your nominee, which is often misunderstood at the time of purchase.

- Product Complexity: There are multiple elements to understand, such as cover multiples, plan options, and value calculations. For someone looking for a simple protection plan, this structure can feel complicated.

- Premium Reduction Trade-off: While the option to reduce premiums exists, it comes with a direct reduction in the sum assured. Once reduced, it cannot be reversed, so this flexibility should be used carefully after understanding the long-term impact.

- Limited Liquidity: The plan does not offer a loan facility, and surrender value builds up only after certain conditions are met. This means you cannot rely on it for quick access to funds in case of emergencies.

Is the ROP option Worth it?

Add-ons Offered By HDFC Life Sanchay Legacy

- Waiver of Premium Options: You can choose Waiver of Premium on Critical Illness or Total Permanent Disability at the start. If triggered, all future premiums are waived while your policy continues.

- Instalment Payout Option: The death benefit does not have to be taken as a lump sum. You or your nominee can choose to receive it in instalments over 5 to 15 years, with flexible payout options like monthly, quarterly, or yearly.

- Premium Reduction Flexibility: After completing five policy years, you can reduce your premium by up to 50 percent. However, this also reduces the sum assured proportionately.

- Acceleration of Benefits: In case of diagnosis of any of the listed 19 critical illnesses, the policy pays the death benefit early as an accelerated payout. However, this reduces the final payout available to your nominee since it is not an additional benefit. This benefit becomes available only after completing 10 policy years or the PPT, whichever is later.

Premium Comparison for HDFC Life Sanchay Legacy

Illustration 1: Life Option

- Entry Age: 45 years

- Annual Premium: ₹10,00,000

- PPT: 10 years

- Death Benefit Multiple: 7x

If the policyholder dies at 85, the nominee receives ₹7.98 crore.

Key Takeaway: This highlights that the Life option is designed for lifelong protection, with a higher death benefit focused purely on legacy creation for the nominee.

Illustration 2: ROP Option

- Entry Age: 55 years

- Annual Premium: ₹10,00,000

- PPT: 10 years

- Death Benefit Multiple: 7x

- ROP: ₹1 crore at age 85

If the policyholder dies at 95, the nominee receives a death benefit of ₹5.44 crore.

Key Takeaway: This shows how the ROP option can return your base premiums at a later stage, while continuing life cover, though the final death benefit may be lower.

Note: Premiums and benefits shown above are illustrative and have been extracted from the Sanchay Legacy brochure for comparison purposes. Actual premiums may vary based on age and insurer underwriting.

Who Should Buy HDFC Life Sanchay Legacy?

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Conclusion

Sanchay Legacy is a niche offering within HDFC Life’s portfolio, positioned for buyers who seek lifelong cover or ROP features. Sanchay Legacy suits a narrower goal of long-term legacy planning, due to which HDFC does not actively market the plan.

It is not a core protection plan and is less suitable for those who prioritize low-cost, high-cover term insurance. That said, for most buyers, term insurance remains the smarter choice for pure protection. Plans like HDFC Life Click 2 Protect Supreme Plus offer flexibility and value.

If you wish to explore other term options, explore our guide on the best term insurance plans.

Frequently Asked Questions

Last updated on: