HDFC Life QuickProtect is a bundled term insurance plan that combines life cover, accidental death benefit, critical illness protection, and disability income support in one product. In simple terms, the policy combines HDFC Life Click 2 Protect Life with 3 in-built features. The plan mainly suits buyers aged 18 to 45, with limited options up to age 50. It can be useful for those who prefer a ready-made cover.

A 35-year-old non-smoking male pays an annual premium of ₹20,802 for a sum assured of ₹1.09 crore for QuickProtect. However, if you wish to purchase an HDFC Life term plan, we recommend Click 2 Supreme Plus, with a 99.55% average claim settlement ratio and competitive pricing. This guide explains HDFC Life QuickProtect and its key comparisons.

Want term insurance without the hassle of comparing multiple add-ons? HDFC Life QuickProtect is built as a simple, ready-made protection plan that helps you secure your family with one streamlined choice. However, this will restrict your freedom to choose among the riders which you actually need. In the next few minutes, you will understand if QuickProtect is the right choice for your family's needs.

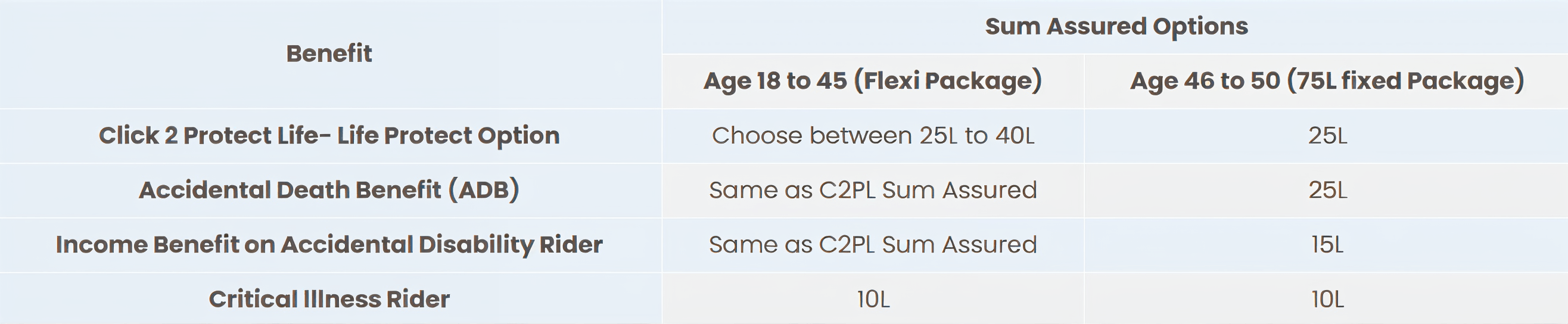

Here’s a snippet from the HDFC Life official website about the sum assured options offered by the plan.

Key Benefits of HDFC Life QuickProtect

Easy All-in-one Solution: You get term cover and useful add-on benefits in one package, instead of selecting a base policy and multiple riders separately. This can save time and make the buying process easier.

Broader Protection: This is more than just life cover. It also includes accidental death enhancement, disability-linked income support, and critical illness protection. That means the plan aims to support your family across different financial risks, not only in case of death.

Useful for Young Buyers: It might work well for younger individuals who want moderate coverage without spending too much time comparing rider combinations. A structured package may feel easier to understand and manage in the early earning years.

CTA

Drawbacks of HDFC Life QuickProtect

01

Less Customization

This is more of a ready-made package than a fully flexible term plan. Buyers who want to choose each rider separately or fine-tune coverage amounts may find fewer options compared to standalone term plans.

02

Coverage Caps Across Benefits

The life cover and rider benefits come with fixed upper limits. This can restrict buyers who need higher protection or want to scale individual covers over time as income and family responsibilities increase.

03

Policy Terms Matter

Actual benefits depend on underwriting approval and the detailed terms of the base policy and riders. It is important to read the brochure and policy wording carefully before buying.

Add-ons Offered by HDFC Life QuickProtect

Accidental Death Benefit (ADB): Pays an additional lump sum to nominees if the insured passes away due to an accident, over and above the base life cover.

Income Benefit on Accidental Disability Rider: Provides regular monthly income if the insured suffers accidental disability, helping manage lost earnings and ongoing household expenses.

Critical Illness Rider: Pays a lump sum on diagnosis of 19 listed illnesses, which can help cover treatment costs, recovery expenses, or income disruption.

Quick Note: These benefits are sold together as part of one bundled solution and are compulsory to purchase.

Premium Comparison

Package Size

Base Life Cover

ADB

Disability Income Rider

Annual Premium

₹94 lakh

₹28 lakh

₹28 lakh

₹28 lakh

₹19,082

₹1.09 Crore

₹33 lakh

₹33 lakh

₹33 lakh

₹20,802

₹1.21 Crore

₹37 lakh

₹37 lakh

₹37 lakh

₹22,621

Note: The listed figures are for a 35-year non-smoker male profile. The premiums, which include a ₹10 lakh critical illness rider, are for the non-ROP variant. These premiums are illustrative and are sourced from the HDFC Life QuickProtect brochure.

Who Should Buy HDFC Life QuickProtect?

People who seek bundled options.

Individuals aged 18 to 45 get the widest choice under QuickProtect, with access to the flexible package variants and broader cover options.

Those aged 46 to 50 can still buy the plan, but only under the ₹75 lakh fixed package.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

HDFC Life QuickProtect can appeal to buyers who want a simple, ready-made term insurance package. It offers convenience, but it is not positioned as the insurer’s flagship protection plan. If you wish to buy an HDFC term plan, Click 2 Protect Supreme Plus is usually the stronger choice.

Better Core Protection: It is more suitable for buyers who want a strong primary term plan built around family security.

More Flexibility: You usually get better scope to choose payout structures, high sum assured options, and features like premium break.

Useful as Life Changes: It gives more room to shape your cover as responsibilities grow, such as marriage, children, home loans, or higher income needs.

If you wish to compare other term plans which align with your future goals, explore our guide on the best term insurance plans.

Frequently Asked Questions

What is HDFC Life QuickProtect, and how is it different from a regular term plan?

HDFC Life QuickProtect is a bundled term insurance plan that combines four benefits in one package. It includes base life cover, accidental death benefit, critical illness cover for listed illnesses, and income support for accidental disability.

In a regular term plan, you usually choose the base cover first and then add riders separately. QuickProtect offers a ready-made solution, which makes the purchase simpler and faster. However, it gives less flexibility if you want to customize each benefit according to your personal needs.

What is HDFC Life's claim settlement ratio, and is it reliable?

HDFC Life reported an average claim settlement ratio of 99.55% for FY 2022 to FY 2025, which is above the industry average of 98.66% for the same period. Its 30-day claim settlement rate stood at 98.93%, which also compares well with peers. These numbers suggest strong reliability in handling valid claims.

The insurer also reported low complaint levels (1.33 per 10000 claims) compared with many competitors. While no metric should be viewed alone, this record gives buyers added confidence during insurer selection.

What is the eligibility age for HDFC Life QuickProtect?

The minimum entry age for HDFC Life QuickProtect is 18 years. The maximum entry age is 45 years for the Flexi package and 50 years for the Fixed package. HDFC Life QuickProtect offers coverage up to a maximum maturity age of 75 years.

Policy terms can range from 5 to 40 years for regular pay options, while limited pay options have a short fixed structure of 10 years. This means the plan mainly suits younger and middle-aged buyers rather than late-entry applicants.

What are the premium amounts for HDFC Life QuickProtect?

A 35-year-old non-smoker male may pay around ₹19,082 yearly for the ₹94 lakh package, ₹20,802 for the ₹1.09 crore package, and ₹22,621 for the ₹1.21 crore package. These examples are for non-return of premium variants and as per the policy brochure.

Actual premiums can differ based on your age, health, and underwriting results. The final premium should always be checked through the insurer's quote before purchase. Female policyholders receive up to 15% discount on annual premiums.

Who should buy HDFC Life QuickProtect?

HDFC Life QuickProtect suits buyers aged 18 to 45 who want an all-in-one protection package without spending time comparing multiple riders. The plan can work well for those who prefer a simple buying experience with life cover, accidental protection, critical illness support, and disability income in one plan.

Buyers aged 46 to 50 may have limited package access. If you want higher customization, larger critical illness cover, or broader flexibility, HDFC Click 2 Protect Supreme Plus will suit you better.

What is the difference between HDFC Life QuickProtect and Click 2 Protect Supreme Plus?

HDFC Life QuickProtect is a bundled plan built for simplicity, with fixed rider combinations included in one package. Click 2 Protect Supreme Plus is HDFC Life’s flagship term plan and offers more flexibility in cover amount, payout choices, and rider selection. It also provides broader critical illness coverage than QuickProtect and offers health management services.

If you want a ready-made option, QuickProtect may appeal to you. However, if you want long-term flexibility, Click 2 Protect Supreme Plus is the better choice.

Can you choose your own riders with HDFC Life QuickProtect?

No, HDFC Life QuickProtect does not allow separate rider selection. The plan comes as a bundled package where base life cover, accidental death benefit, critical illness rider, and disability income support are included together. You cannot remove one rider, add a different rider, or set separate cover amounts for each feature.

However, buyers who want personalized cover structures may find this plan less flexible than standard term plans. If you wish to select the riders, we recommend exploring other term options provided by HDFC Life.

Is HDFC Life QuickProtect HDFC Life's flagship term plan?

No, HDFC Life QuickProtect is not the insurer’s flagship term insurance plan. It is a bundled combo product designed for convenience-focused buyers who want one ready-made package. HDFC Life’s flagship protection plan is Click 2 Protect Supreme Plus, which offers stronger flexibility and better rider choices. It is generally better suited for long-term family financial planning.

QuickProtect can still work well for buyers who value simplicity over customization and advanced features. Click 2 Protect Supreme Plus is the right choice for those who wish to strike the correct balance between coverage and affordability.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.