Quick Overview

Here's a situation many of us have faced: a friendly insurance agent walks in, pitches a plan that gives you "insurance and investment," and it sounds like the perfect deal. Why buy two separate products when one does it all, right? That product is almost always a ULIP.

But when you compare ULIP vs term insurance, the differences become clear. A term insurance plan focuses purely on protection, offering high coverage at a low cost. A ULIP, on the other hand, mixes insurance with market-linked investments, often with higher charges and complexity. So, which one should you choose? Let’s break it down in this guide.

What Are ULIPs and Term Insurance?

Term Insurance

Term insurance is the simplest form of life insurance. You pay a premium, and if something happens to you during the policy term, your nominees receive the sum assured. These plans do not have a maturity benefit unless you opt for the Return of Premium (ROP) variants, which are 80%-100% expensive. Because of this simplicity, they offer very high coverage (₹1 crore or more) at affordable premiums, providing peace of mind for your family.

Unit-Linked Insurance Plan

A ULIP plan combines life insurance with market-linked investment. Part of your premium goes toward life cover, and the rest is invested in funds (equity, debt, or balanced). Your returns depend on market performance. That sounds convenient, but the cost and complexity often make ULIPs less straightforward than they appear.

ULIP vs Term Insurance: Key Differences

Tax Benefits: ULIP vs Term Insurance

- Section 80C: Both term insurance and ULIPs qualify for tax deductions under Section 80C (old regime) of the Income Tax Act, 1961, up to the overall limit of ₹1.5 lakh per year. Premiums paid toward a term plan are fully eligible, provided they do not exceed 10% of the sum assured (for policies issued after April 2012). ULIP premiums also qualify under the same limit and conditions.

- Section 10(10D): Under Section 10(10D), the death benefit from both term insurance and ULIPs is fully tax-free in the hands of the nominee. However, the maturity proceeds from ULIPs are tax-free only if the annual premium does not exceed ₹2.5 lakh (for policies issued after February 1, 2021). If the premium crosses this threshold, ULIP gains are taxed as equity capital gains, reducing their tax efficiency compared to term plans.

Premium Comparison: Term Insurance vs ULIP

Term Insurance Premiums

For this example, we’ve considered profiles of healthy, salaried, non-smoking individuals living in a tier-1 city like Delhi (pin code: 110010) with a sum assured of ₹1 crore and coverage until age 65. The premiums are indicative and can vary depending on your age, sum assured, health conditions, lifestyle choices, and underwriting decisions.

ULIP Premiums

Unlike term insurance, ULIP premiums are not directly comparable across insurers in a simple table format. This is because your premiums are split into life insurance, investment components, and multiple policy-related charges.

Let’s take a similar profile for comparison: A 30-year-old covered for a sum assured of ₹10 lakh with a policy term of 20 years and an annual premium of ₹1 lakh.

Here’s how your premium is typically allocated in a ULIP:

Note: These charges are illustrative in nature and not definitive. They do not pertain to any specific ULIP.

What This Means in Reality:

- In the initial years, a noticeable chunk of your premium is deducted before investment even begins.

- Even after that, annual charges (FMC, admin, and mortality) continue to reduce your returns.

- Mortality charges increase with age, further impacting long-term performance.

Simple Way to Think About It:

If you invest ₹1 lakh annually in a ULIP:

- Only ₹90,000 (or less in early years) may actually get invested.

- From that, 1%- 2% is deducted each year as ongoing charges.

Over 10-15 years, this can significantly reduce your effective returns compared to cleaner investment options.

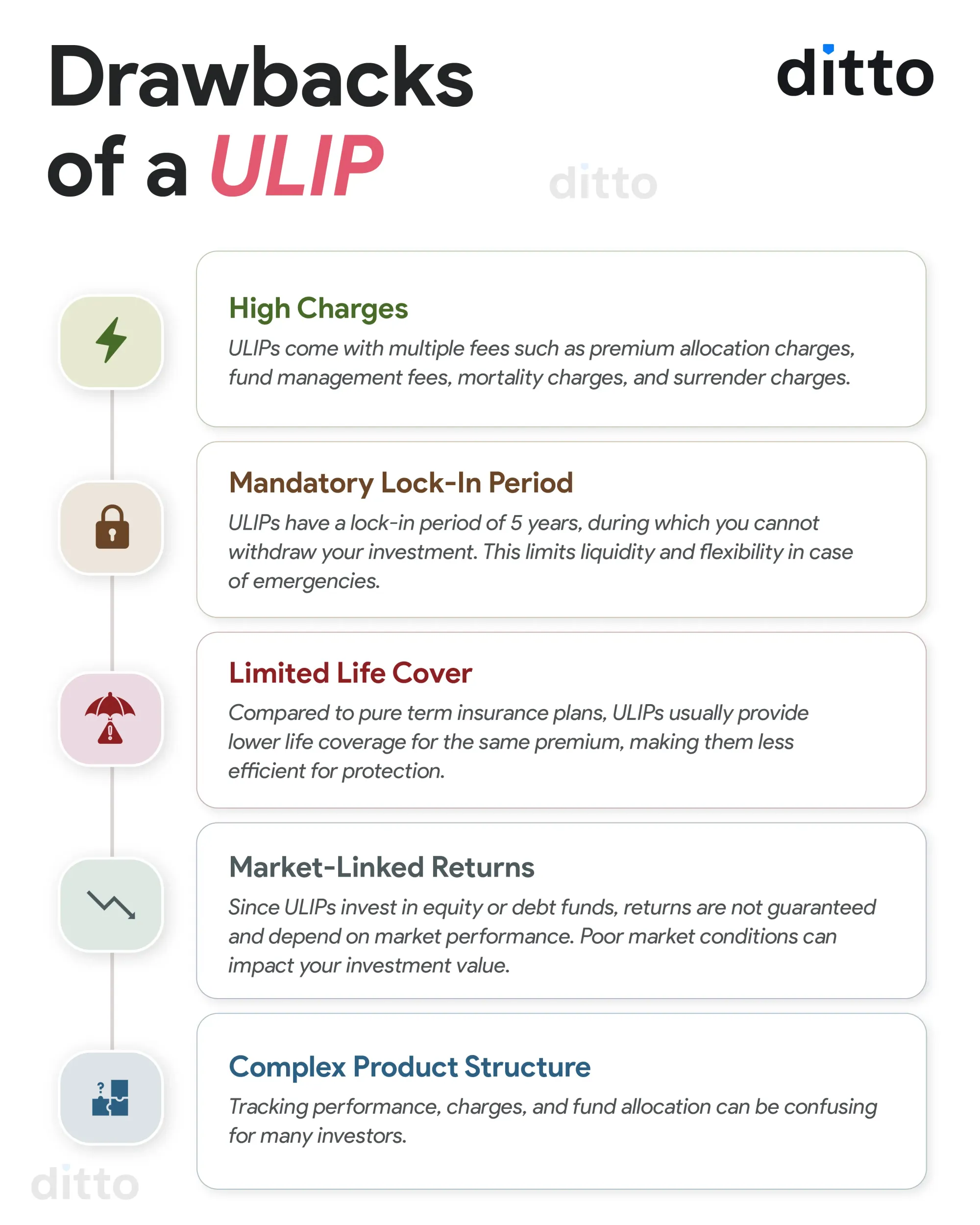

Drawbacks of ULIPs

On paper, ULIPs look attractive, but in reality, they come with many drawbacks. For more details, you can refer to the attached infographic:

When Does a ULIP Make Sense Over Term Insurance?

A ULIP may make sense if you:

- Want forced long-term investing discipline

- Are comfortable with market-linked risk

- Prefer a single bundled product

- Plan to stay invested for 10-15 years or more

However, even in these cases, you should carefully evaluate the charges, fund performance, and lock-in restrictions.

The Verdict: Why Most People Should Choose Term + Investment

For most people, combining insurance and investing in a single product is not ideal.

Instead, a smarter approach is:

- Buy a term insurance plan for protection.

- Invest separately in mutual funds or other instruments.

This works better because you get maximum life cover at minimum cost while maintaining flexibility in investments. You also avoid unnecessary fees and can adjust your investments to align with your goals.

You can also refer to our guide on the best term insurance plans in India to find the right fit for your needs.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

In the ULIP vs term insurance debate, the latter stands out as the clear choice for pure financial protection. ULIPs, while combining insurance and investment, often fall short due to higher charges, complexity, and restricted flexibility.

For most individuals, the smarter strategy is to separate the two: opt for a term insurance plan for robust protection and invest independently in more transparent, cost-efficient instruments. This approach not only maximizes coverage but also gives you better control over your financial goals and returns.

Frequently Asked Questions

Last updated on: