From a consumer’s perspective, there are two primary types of life insurance: protection plans (which provide a death benefit) and savings or investment products (which provide life cover and wealth accumulation). But IRDAI’s formal product categories are more detailed and include linked and non-linked products, as well as pension, annuity, and pure-risk products.

At Ditto, our one and only recommendation is term insurance because it provides high life cover (such as ₹2 crore) at affordable premiums. For example, a healthy 25-year-old salaried non-smoker can get ₹2 crore coverage until 65 under Axis Max Life Smart Term Plan Plus for an annual premium of around ₹17,222.

In comparison, other life insurance policies, such as Unit Linked Insurance Plans (ULIPs), pension plans, or whole life insurance, come with significantly higher premiums and often deliver lower protection value.

Many families in India buy life insurance because a bank executive, agent, relative, or colleague recommended a policy. The pitch usually sounds comforting: “You’ll get insurance, savings, tax benefits, and returns in one plan.” As a result, people may believe they are financially protected while remaining underinsured.

A key reason behind this is confusion around the different types of life insurance and what they actually offer.

In this guide, we'll break down the different types of life insurance as defined by IRDAI, explain how each works, and help you understand which option makes the most sense for your needs.

Need help choosing the right life insurance policy for you? Book a call or chat on WhatsApp with our IRDAI-certified advisors.

Goal-based savings offered as ULIPs or endowment plans

Child education planning

Parents should first secure their own term cover because better investment options like NPS Vatsalya, Sukanya Samriddhi Yojana, PPF, etc., exist

SBI Life Smart Scholar

Annuity/Pension

Retirement income

Retirement planning and cashflow management

Useful only for retirement-income needs, not suitable for life insurance

LIC Jeevan Akshay VII

Note: In this table, PPF stands for Public Provident Fund, and NPS stands for National Pension Scheme.

Term Insurance Plans

Among all types of life insurance policy, term insurance is the simplest, purest, and, in our view, the most effective option.

You pay a premium for a fixed period, and if something happens to you during the policy term, your family receives the payout. There is no investment component, no complicated structure, and no hidden calculations. Because it focuses only on protection, premiums stay affordable while life cover remains high. You can also check out our comprehensive guide on the best term insurance plans in India to find the right pick for you.

You could get coverage of ₹2 crore or more at a fraction of what traditional policies would cost.

Premium Comparison of Term Insurance Plans

Profile

Axis Max Life Smart Term Plan Plus

HDFC Life Click2Protect Supreme Plus

ICICI Prudential iProtect Smart Plus

25, Male

₹17,222

₹19,719

₹16,111

25, Female

₹14,640

₹16,761

₹13,694

30, Male

₹20,656

₹25,153

₹19,283

30, Female

₹17,558

₹21,380

₹16,391

35, Male

₹26,552

₹31,118

₹26,030

35, Female

₹22,570

₹26,451

₹22,126

For this illustration, we’ve considered sample profiles of healthy, salaried, non-smoking individuals living in a tier-1 city such as Delhi (pincode: 110010) and covered until age 65 (without first-year discounts). The premiums are indicative and vary based on your age, sum assured, policy term, riders chosen, and underwriting.

Key Takeaway: For a relatively small premium, you can secure a large financial safety net for your family.

Unit Linked Insurance Plans (ULIPs)

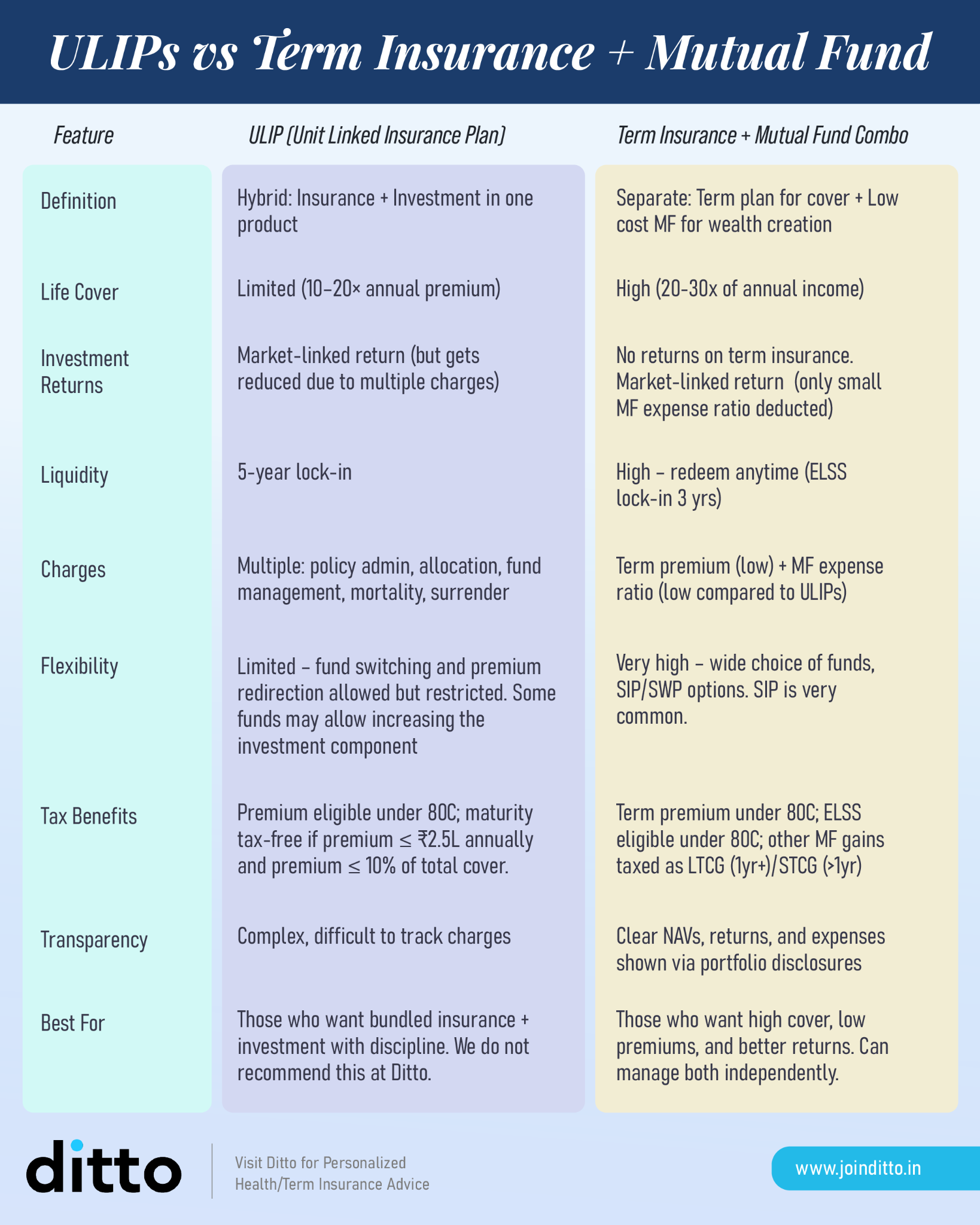

ULIPs combine insurance with investments. A part of your premium goes toward life cover, while the rest is invested in market-linked funds such as equity or debt funds. On paper, this sounds attractive because you get both insurance and investing in a single product. However, ULIPs involve multiple charges, 5-year lock-in periods, and limited flexibility compared to simply buying term insurance and investing separately in mutual funds.

Note: IRDAI also states that in ULIPs, the investment risk is borne by the policyholder, so returns are not guaranteed. The 4% to 8% returns you see in your policy brochures are IRDAI-mandated illustrations, but in reality, the returns depend on market performance and can vary.

Due to these drawbacks, ULIPs often fall short in comparison to term insurance. For more details, refer to the infographic attached below:

Endowment, Money-Back, Whole Life & Other Plan Types

You pay premiums regularly, and at maturity, you receive a lump-sum payment if you survive the policy term. Your family also gets a death benefit if something happens to you during the policy period.

While they provide certainty, returns are generally modest (under 7%, which is usually in line with or lower than Fixed Deposit (FD) rates), and premiums can be quite high. Moreover, some benefits may be guaranteed, while bonuses or additions depend on the product type and insurer declarations.

CTA

Money-Back/Cashback Plans

Money-back plans return a percentage of the sum assured at regular intervals during the policy term. Many people like them because they create a sense of receiving periodic returns. The downside is that these policies generally cost more and often provide lower overall insurance value compared to term plans.

Whole Life Plans

Whole life insurance provides coverage for your entire life rather than for a fixed duration. Some policies may also build cash value over time. While lifelong coverage may sound appealing, most people need substantial financial protection only during their working years, when their families depend on their income. Because of this, whole life plans may not always justify their higher costs.

Children Policies

Child insurance plans are designed to help build a financial corpus for future goals like education or marriage. These plans combine life cover with savings or investment components. While the idea is understandable, parents can often achieve the same goal more efficiently by purchasing a term plan and investing separately in the kid’s name.

Annuity/Pension Plans

According to IRDAI, there are two types of annuity plans: immediate and deferred annuity. These aim to provide income during retirement. In an immediate annuity, you pay a purchase price, and income starts immediately or shortly after purchase. In a deferred annuity, income starts after the chosen deferment period. These plans may offer less flexibility than building retirement investments independently.

Note: The benefit illustration matters more than the sales pitch when it comes to life insurance policies. IRDAI requires life insurers to provide a customized benefit illustration at the point of sale, and it becomes part of the policy document. This is where you should check what is guaranteed, what is not guaranteed, what charges apply, and what your family actually receives.

How to Choose the Right Type of Life Insurance?

Understand Why You’re Buying Insurance

Before choosing a life insurance policy, get clear on its purpose. If your goal is to financially protect your family in your absence, a simple term insurance plan is often the most effective choice. Your needs may vary based on your income, dependents, loans, and future responsibilities, so the right policy should align with those realities rather than marketing promises.

Calculate Your Required Life Cover

Your life cover should be large enough to replace your income, pay off liabilities, and support your family’s future goals. A common starting point is to calculate it by considering your present expenses, outstanding liabilities, future financial goals, and inflation. You can also use the cover calculator on Ditto’s website if you need help, because choosing an insufficient cover just to save on premiums can leave your family underprotected.

Keep Insurance and Investment Separate

Life insurance works best when it focuses purely on protection. Plans that combine insurance with returns or savings usually come with higher premiums and lower overall value. A straightforward term plan gives you higher coverage at a lower cost, while your investments can be managed separately through options better suited for wealth creation.

Compare Different Plans and Insurers

Don’t choose a policy based only on the cheapest premium. Compare insurers on key factors such as claim settlement performance, financial strength, customer service, and policy features. Also, review riders, payout options, and exclusions carefully to ensure the policy genuinely fits your long-term needs and provides dependable support when your family needs it most. You can also check our comprehensive guide on the best term insurance companies in India to find the right one for you.

Note: If you’re ineligible for a term plan due to income, education, or occupation criteria, an alternative such as a ULIP or endowment may be considered after a thorough review.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

There are many types of life insurance policies available today, but more choices don't automatically mean better decisions. The key is understanding what problem you're trying to solve.

If your goal is to protect your family's financial future, term insurance often provides the best balance of high coverage and affordability. Other types of life insurance plans may work for specific situations, but many people end up paying extra for features they don't actually need.

The right policy isn't the one with the longest brochure or the most promises. Instead, it's the one that gives your family meaningful protection without complicating your finances.

Frequently Asked Questions

What are the different types of life insurance in India?

There are primarily two categories of life insurance in India: pure protection plans and investment or savings plans. Protection plans, such as term insurance, pay a death benefit if the policyholder dies. Investment plans, like Unit Linked Insurance Plans (ULIPs) and endowment policies, combine life cover with wealth accumulation. Within these two categories, there are 7 main types: term insurance, ULIPs, endowment, money-back, whole life, child plans, and annuity/pension plans. At Ditto, we always recommend starting with a pure protection plan before exploring anything else.

What is the best type of life insurance to buy in India?

For most Indian families, term insurance is the best type of life insurance to buy. It offers high coverage, typically between ₹1 crore and ₹5 crore or more, at affordable premiums. A healthy 25-year-old male non-smoker can get ₹2 crore coverage until 65 under Axis Max Life Smart Term Plan Plus for an annual premium of around ₹17,222. At Ditto, our recommendation is term insurance because it provides real financial protection without unnecessary complexity or high costs.

What is term insurance and how does it work?

Term insurance is the simplest type of life insurance policy. You pay a fixed premium for a chosen policy period, and if the policyholder passes away during that term, their family receives the death benefit. There is no investment component or maturity value at the end of the term. Because term insurance focuses solely on protection, premiums remain low while life cover remains high. It is straightforward, transparent, and at Ditto, we consider it the most effective life insurance option for the majority of working individuals and families.

What is a ULIP and is it worth buying?

A ULIP, or Unit Linked Insurance Plan, combines life insurance with market-linked investments. A portion of your premium goes toward life cover, while the rest is invested in equity or debt funds. ULIPs come with a 5-year lock-in period, multiple charges, and limited flexibility overall. According to IRDAI, the investment risk in ULIPs is borne entirely by the policyholder, so returns are not guaranteed. At Ditto, we believe it is better to separate your insurance and investments rather than bundle them in a ULIP.

What is the difference between term insurance and endowment plans?

Term insurance provides pure life coverage. You pay a premium, and your family gets a payout only if you pass away during the policy term. Endowment plans combine insurance with guaranteed savings and pay a lump sum at maturity even if you survive. The trade-off is significant: endowment plans charge much higher premiums for a much lower life cover. For someone who needs meaningful financial protection for their family, term insurance typically delivers far greater value. At Ditto, we recommend separating your insurance and savings goals for better outcomes.

What is a money-back policy in life insurance?

A money-back plan is a type of life insurance that returns a percentage of the sum assured at regular intervals during the policy term, rather than only at maturity. While people often find the periodic payouts appealing, these plans typically cost more and deliver lower overall value compared to term insurance. The premiums are higher, the life cover is lower, and the periodic returns are modest. At Ditto, we generally find that money-back plans are a poor substitute for a solid term plan combined with a separate, more efficient investment option like PPF, FDs or Debt mutual funds.

What is whole life insurance and do I need it?

Whole life insurance provides coverage for your entire lifetime rather than for a fixed policy term, and some policies build a cash value over time. While lifelong coverage sounds attractive, most people need only substantial financial protection during their working years, when their family depends on their income. After retirement or once dependents become financially independent, the need for large life cover typically reduces. Because whole-of-life plans carry higher premiums, at Ditto, we believe they are unnecessary for the majority of working-age buyers in India.

What are child insurance plans and should parents buy them?

Child insurance plans are savings-linked policies designed to build a financial corpus for a child's education or future goals. They combine life cover with an investment or savings component. While the intention is sound, these plans often come with higher costs and lower flexibility. Parents can usually achieve the same goal more efficiently by first securing their own term life insurance, then investing separately in instruments better suited to long-term wealth creation. At Ditto, we suggest parents prioritize securing their own term life cover before exploring any goal-based child policy.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.