Quick Overview

According to SBI Life’s Chief Executive Officer (CEO) and Managing Director (MD), Amit Jhingran, traditional insurance plans often struggle to keep pace with inflation, prompting more investors to explore alternatives like ULIPs.

An SBI ULIP plan attempts to bridge this gap by combining insurance and investment into a single product. But the real question is: does it actually deliver better value than simpler alternatives?

In this guide, we take a closer look at SBI Life’s ULIP offerings, their key features, potential drawbacks, and how they stack up against a term insurance plus mutual fund strategy.

SBI Life: Performance Metrics

Key Insights:

- Although SBI Life’s CSR falls slightly below the industry mean, it remains within the acceptable range.

- The insurer’s ASR indicates that it settles both low and high-value claims fairly.

- The low complaint volume indicates a smooth claim experience.

- SBI Life’s solvency ratio is comfortably above the minimum requirement of 1.5x set by the Insurance Regulatory and Development Authority of India (IRDAI).

- SBI Life is the second-largest insurer after LIC (Life Insurance Corporation of India) by business volume.

ULIP Plans Offered by SBI Life

1) eWealth Plus

SBI Life eWealth Plus is a relatively simple, online ULIP designed for hands-off investors. It offers a minimum sum assured of 10 times the annualized premium. You can choose between regular pay or limited pay (7 or 10 years), with policy terms ranging from 10 to 30 years. The entry age ranges from 5 to 50 years, with maturity capped at 65 years.

Standout Feature: The Automatic Asset Allocation (AAA) strategy gradually shifts your investments from equities to safer assets as you near maturity, effectively serving as a built-in risk-management tool.

2) Smart Fortune Builder

SBI Life Smart Fortune Builder offers a sum assured of 10 times the annual premium (or 1.25 times for single pay) and supports all three premium payment options: regular, limited (7/10/12/15 years, depending on the term), and single pay. Policy terms typically range from 15 to 30 years, with entry age starting as low as 2 years and maturity capped at 70 years.

Standout Feature: The guaranteed additions begin from the 10th policy year and continue at regular intervals, along with a maturity booster linked to premium size and tenure.

3) Smart Elite Plus

SBI Life Smart Elite Plus is positioned as a premium ULIP for high-income investors, offering a sum assured of 7 times the annualized premium (or 1.25 times for single pay). The plan also offers limited pay (7/10/12 years) or single pay options, with policy terms ranging from 15 to 30 years. The entry age starts at 18 years, with maturity up to 70 years.

Standout Feature: It includes an in-built accident benefit (Accidental Death Benefit and Total Permanent Disability) without the need for a separate rider.

4) Smart Privilege Plus

SBI Life Smart Privilege Plus provides a sum assured of 7 times the annualized premium (or 1.25 times for single pay). You can choose from regular, limited, and single pay options, with a policy term of 10-30 years. The entry age starts at 8 years, with a maturity cap of 70 years.

Standout Feature: Its loyalty additions begin from the end of the 6th policy year and increase progressively over time, directly boosting your fund value.

You can explore the official plan details on SBI Life’s official ULIP page.

Available Riders

- Accidental Death Benefit (ADB)

It provides an additional payout over and above the base death benefit if the policyholder dies due to an accident (typically within 180 days from the date of the accident). It is capped at 3 times the base sum assured for most plans. However, in plans like Smart Elite Plus, this is an in-built feature, and the accident cover equals the base sum assured (with a cap of ₹50 lakh). - Accidental Partial/Total Disability Benefit

The Accidental Disability Benefit provides financial support if the policyholder suffers a permanent disability resulting from an accident, such as the loss of limbs or eyesight. The policy continues even after payout, ensuring life cover remains intact. As with ADB, the disability must occur within a defined window (typically 180 days of the accident) and meet strict medical definitions.

Drawbacks of Buying an SBI ULIP Plan

High Initial Charges

Mandatory 5-Year Lock-in Period

Complex Structure and Lack of Transparency

Market-Linked Returns

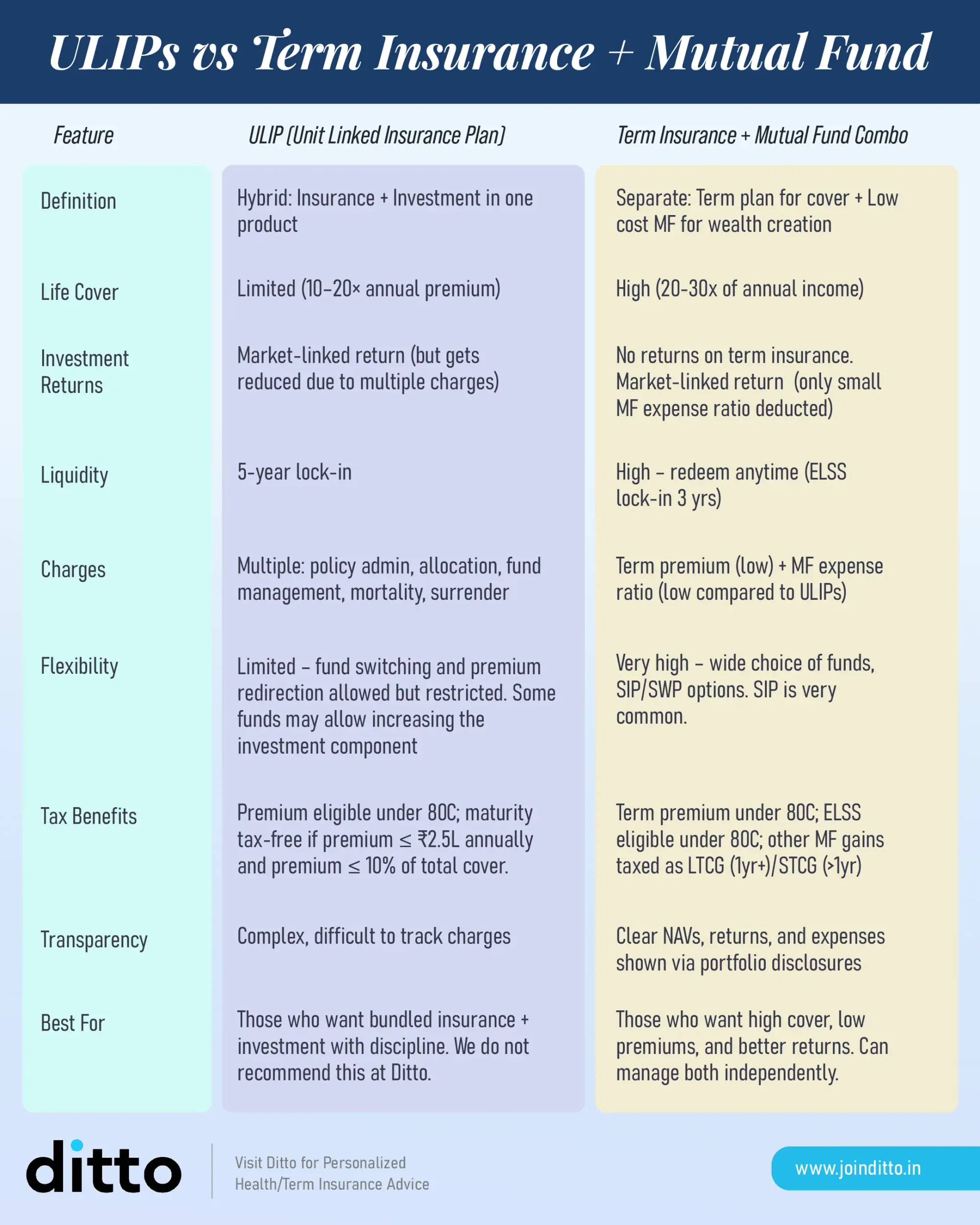

ULIP vs Term Insurance: Which is Better?

Premium Illustration

Let’s take an example of a 30-year-old, healthy, non-smoking male covered under SBI Smart Privilege Plus with a sum assured of ₹1,05,00,000, as per the policy brochure.

As per IRDAI guidelines, insurers are required to show ULIP returns of 4% and 8%.

In reality, your net yield is lower due to multiple charges. Even in well-performing funds, a 1-2% annual drag from charges can materially reduce long-term compounding, making ULIPs less efficient than standalone investments for pure wealth creation.

Term Insurance Premium Comparison

For this example, we’re considering healthy, non-smoking salaried profiles living in a tier-1 city like Delhi (pincode: 110010), covered until age 65 with a sum assured of ₹1 crore.

- As is evident from the premium examples above, term insurance is the better choice, offering pure protection with high life cover at a relatively low premium. If you’d like to learn more about term plans, you can also check out our detailed guide on the best term insurance plans in India.

- After buying a term plan, you can invest the remaining amount into any investment tool of your choice, such as mutual funds, Public Provident Fund (PPF), Fixed Deposits (FDs), etc.

- This separation offers better flexibility, transparency, and control over your finances.

For a deeper comparison between ULIPs and a term insurance plus mutual fund approach, refer to the attached infographic.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Take on SBI ULIP Plan

At Ditto, we do not recommend ULIPs at all. While SBI Life is a strong insurer, its ULIP plans are still not up to the mark due to an inefficient product structure. When you combine insurance and investment, you often end up with higher costs, lower flexibility, and suboptimal returns compared to simply buying a term plan and investing separately.

Full Disclosure: SBI Life is not a partner insurer of Ditto. This article is purely for informational purposes, and all the details above have been sourced from IRDAI annual reports, insurer websites, and publicly available data.

Frequently Asked Questions

Last updated on: