What is SBI Life Smart Elite?

The SBI Life Smart Elite Plus plan (UIN: 111L146V01) is a Unit Linked Insurance Plan (ULIP) underwritten by SBI Life Insurance Company Limited, a joint venture between the State Bank of India (SBI) and BNP Paribas Cardif.

In this guide, we will walk you through the SBI Life Smart Elite Plus plan details, its features, benefits, charges, and key considerations to help you decide whether it’s the right choice for you.

What Is the SBI Life Smart Elite Plus Plan?

SBI Life Smart Elite Plus is an evolution of the original Smart Elite plan. While they share the same target audience of HNIs, the "Plus" version is an exquisitely crafted product offering enhanced flexibility and opportunities for wealth creation.

There are some key overlaps, too, that can be analyzed by examining the features offered by both plans.

Common Features of SBI Life Smart Elite Plus and Smart Elite Plans

- Dual Protection: Choice between the Gold option (death benefit is the higher of sum assured or fund value) and the Platinum option (death benefit is sum assured plus fund value).

- In-built Accident Cover: Includes Accidental Death Benefit (ADB) and Accidental Total & Permanent Disability (ATPD) coverage at no extra premium cost.

- Reduced Charges: No premium allocation charges (PACs) are deducted from the 6th policy year onwards to boost fund growth.

Key Features of SBI Life Smart Elite Plus

- Expanded Fund Options: Smart Elite Plus provides access to 9 varied fund options, whereas older versions of the standard plan were documented with 8.

- Digital Accessibility: The Plus version is explicitly noted as available for online sale, making it more accessible than traditional, offline-only products.

- Higher Investment Ceiling: It is designed to "maximize savings" by providing more granular control over the investment portfolio than the legacy version.

- Flexible Premium Payment: Limited Pay (7, 10, or 12 years) or Single Pay options; multiple premium frequencies available.

- Fund Switch and Premium Redirection: First two switches per year are free; thereafter, ₹100 per switch.

- Partial Withdrawal: No full/partial withdrawals in the first 5 years. Liquidity from the 6th policy year onwards, up to 15% of fund value.

- Settlement Option for Death Benefit: Nominees can receive the death benefit in installments over 2–5 years, continuing market participation.

Quick Note: At the time of purchasing the SBI Life Smart Elite Plus plan, you must select either the Gold or the Platinum option. This is a permanent choice that cannot be changed during the policy term. Here’s a comparison of the two key variants:

SBI Life Smart Elite Plus Gold vs Platinum Option

Takeaway: Choose Gold if you are comfortable with either fund value or sum assured being paid (whichever is higher). Choose Platinum if you are a young policyholder with dependents, and want both components, sum assured and fund value, to be paid to your nominee.

Eligibility Criteria for SBI Life Smart Elite Plus

Key Implication: The life cover provided by SBI Life Smart Elite Plus is usually small relative to what most families need. For instance, the sum assured is ₹17.5 lakh (7x) at a yearly premium of ₹2.5 lakh. That is nowhere near a serious level of protection for most earners.

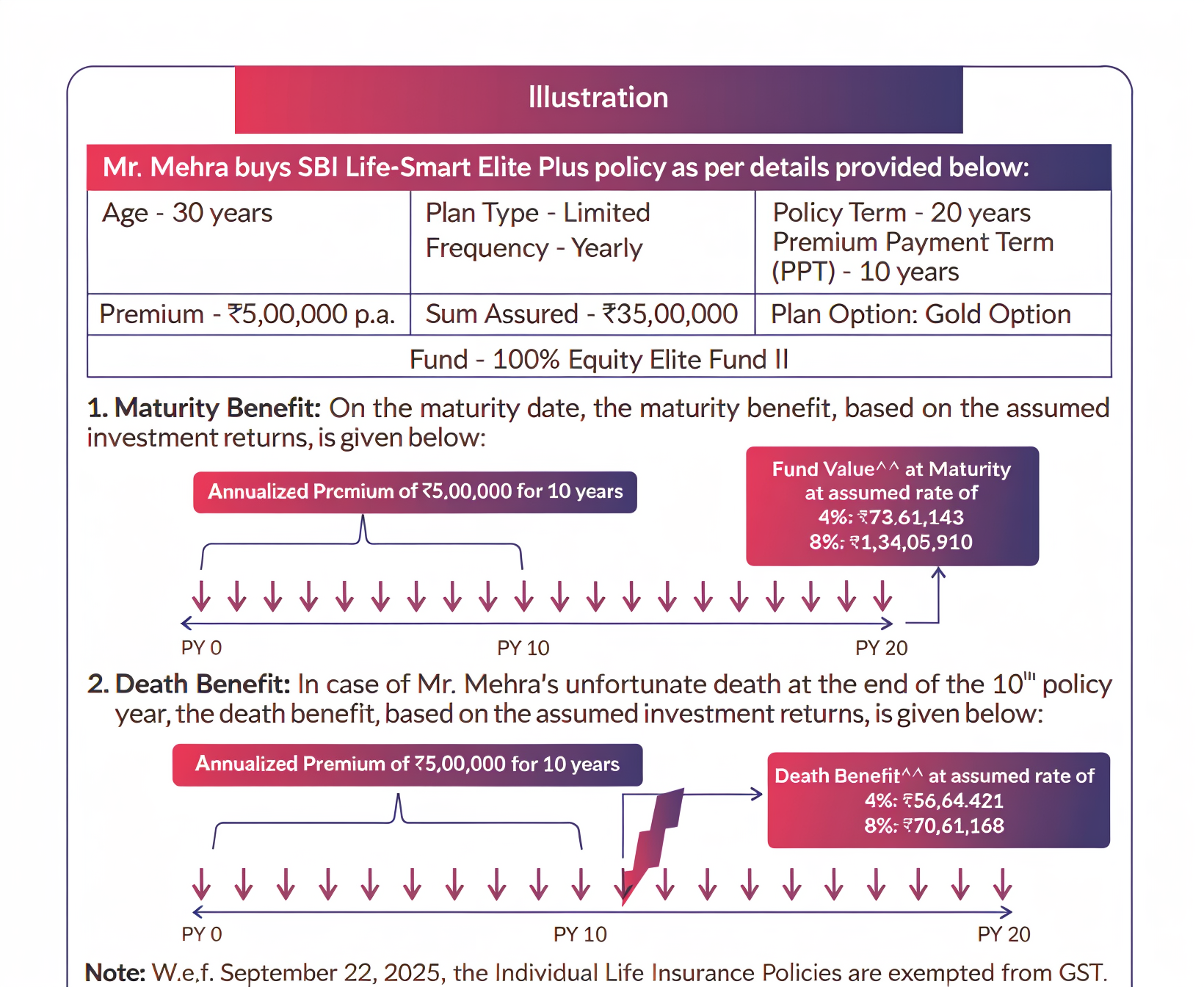

SBI Life Smart Elite Returns and Investment Benefits

Unlike traditional insurance plans in India that offer guaranteed returns or declared bonuses, SBI Life Smart Elite Plus generates returns through direct participation in capital markets. Your premiums, after deduction of applicable charges, are converted into units of the investment funds you choose. The value of these units changes daily based on each fund's Net Asset Value (NAV), which reflects the performance of the underlying securities (equities, bonds, or money market instruments).

This means that when markets perform well, your investment value can grow much faster than traditional fixed-income options. However, when markets fall, your fund value can also decrease. That’s why this plan is better suited for long-term goals (15 years or more). The following illustration from the SBI Life Smart Elite Plus brochure can help you understand the process better:

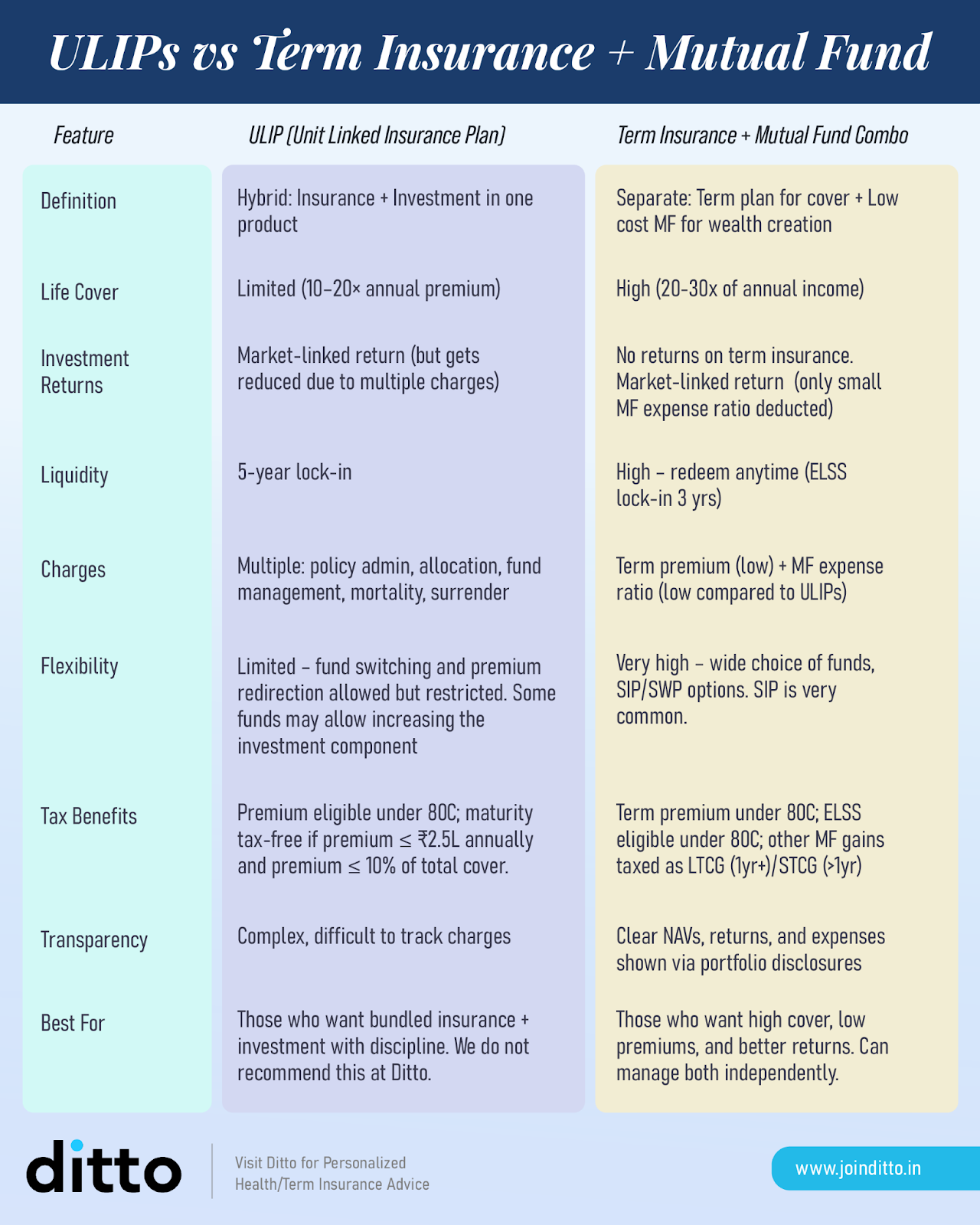

On that note, if you want to learn more about the differences between term insurance plans + mutual funds and ULIPs, refer to the infographic below:

Tax Benefits Under SBI Life Smart Elite Plus

Note: For ULIPs issued on or after February 1, 2021, the maturity proceeds are only tax-exempt under Section 10(10D) if the aggregate annual premium across all your ULIP policies does not exceed ₹2.5 lakhs in any year.

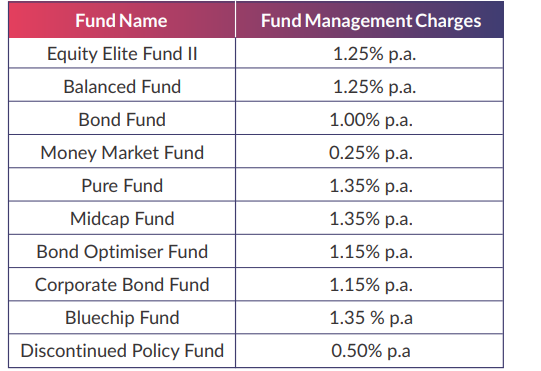

SBI Life Smart Elite Fund Value and Fund Options

You can easily invest in any one or a combination of the following funds (in multiples of 1%):

- Equity Elite Fund: Provides high equity exposure, targeting higher long-term returns.

- Balanced Fund: Provides accumulation of income through investments in both equities and fixed income securities

- Bond Fund: Allows debt instruments and accumulation of income through investment in fixed-income securities.

- Money Market Fund: Allows you to temporarily deploy funds into liquid, safe instruments to avoid market risk.

- Bond Optimizer Fund: Allows investments in government Securities, corporate bonds, money market instruments, and up to 25% in equity instruments.

- Pure Fund: Provides high equity exposure, targeting better long-term returns.

- Midcap Fund: Provides high equity exposure targeting higher returns in the long term by investing predominantly in midcap companies.

- Corporate Bond Fund: Helps you invest in debt instruments and optimize returns through medium-term corporate bonds.

- Bluechip Fund: Enables long-term growth through large-cap equity.

- Discontinued Policy Fund: This is a segregated fund for policies discontinued during the compulsory 5 year lock-in and is not offered as an investment choice. It aims to generate stable, low-volatility returns by primarily investing in debt and other fixed-income instruments.

Learn more about the assets and risks associated with these funds, including their calculations, in the SBI Life Smart Elite brochure.

Charges, Benefits and Policy Advantages of Smart Elite

There are certain charges on the premiums paid for SBI Life Smart Elite Plus (Page 20 of the brochure). Here’s an overview:

- Premium Allocation Charges (in %): Deducted at the time of the receipt of premiums.

- Policy Administration Charge: Deducted by cancelling units at the prevailing unit price on the first business day of each policy month (subject to a cap of ₹500 per month).

- Fund Management Charges: A certain fixed percentage of the asset value of the relevant fund before calculating the NAV (subject to a cap of 1.35% except for discontinued policy funds).

- Discontinuance or Surrender Charge: Expressed as a percentage of one annualized premium, single premium, or fund value.

Note: The NAV is declared daily for each segregated fund for policyholders to track the performance of their selected funds.

Net Yield And Cost Impact

Profile: Premium ₹5,00,000 Per Annum (P.A.) for 10 years

Policy Term: 20 years

Gold Option

100% Equity Elite Fund II

Sum Assured ₹35,00,000.

Brochure Maturity Fund Value (After All Applicable Charges):

- At Assumed 4% Return: ₹73,61,143

- At Assumed 8% Return: ₹1,34,05,910

Note: These 4% and 8% rates are illustrative scenarios only, not guarantees.

1) “Net Yield” To The Investor (IRR)

Treat this cash flow like an investment: You pay ₹5,00,000 each year for 10 years (total ₹50,00,000), then you receive the maturity value at the end of year 20.

Brochure Scenario Maturity Value Implied IRR (Net Yield)

- 4% Illustration ₹73,61,143 = 2.51% to 2.68% P.A.

- 8% Illustration ₹1,34,05,910 = 6.46% to 6.90% P.A.

Why Consider a Range: The calculation depends on whether you model premiums as paid at the start of each policy year (lower IRR) or at the end of each year (higher IRR). Either way, the numbers above are the clean “effective return” implied by SBI Life’s own maturity values.

Return Drag vs Illustration Rate:

- The 4% illustrated scenario becomes 2.5% to 2.7% net, so drag is 1.3% to 1.5% per year.

- The 8% illustrated scenario becomes 6.5% to 6.9% net, so drag is 1.1% to 1.5% per year.

2) Cost Impact In Rupees (How Much Lower The Corpus Looks)

A simple way to show “impact of costs” is to compare:

A No-cost Scenario: Every ₹5 lakh is fully invested and compound at the same gross rate (4% or 8%) until year 20, vs. the brochure maturity value (which is calculated after necessary charges).

No-cost Future Value (Same Premiums, Same Gross Rate):

- At 4%: ₹88.86 lakh to ₹92.41 lakh

- At 8%: ₹1.56 crore to ₹1.69 crore

Compared to Brochure Maturity Values:

- At 4%: The brochure shows ₹73.61 lakh, so the gap is ₹15.25 lakh to ₹18.80 lakh lower

- At 8%: The brochure shows ₹1.34 crore, so the gap is ₹22.32 lakh to ₹34.83 lakh lower

This “gap” is the combined effect of all policy costs and insurance charges over time (not just one fee). Apart from the benefits of fund allocation, here are additional benefits of SBI Life Smart Elite Plus.

Should You Invest in SBI Life Smart Elite Plus?

Note: If you meet all these criteria, then SBI Life Smart Elite Plus can be a “structured wrapper” for long-term market-linked investing. The Gold option is usually the most sensible default if wealth creation is your priority.

Alternatively, you should avoid SBI Life Smart Elite Plus if any of these describe you:

- You want maximum insurance cover at minimum cost (this is a weak insurance-first product).

- You want flexibility to pause, top-up, change SIPs, or use the money earlier.

- You are cost-sensitive and prefer simple, transparent investing (ULIP charge stack is real).

If you want to understand the concept in-depth, check out our guide on What are ULIPs (Unit Linked Insurance Plans).

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a 30-minute call or chat on WhatsApp with our expert IRDAI-certified advisors.

Ditto’s Take on SBI Life Smart Elite Plus

SBI Life Smart Elite Plus might seem appealing to many as a ULIP. However, the multiple charges, the 5-year lock-in period, and the dependence on market performance can impact the overall return on investment.

While the plan also offers tax benefits and flexibility in switching funds, it may not always be the most cost-effective solution, especially if you’re looking for high insurance coverage or low fees. For those seeking lower premiums, better control, and more flexibility over their investments, term insurance combined with mutual funds could be a more suitable alternative.

Since SBI Life Smart Elite Plus is aligned towards high-net-worth individuals, we would also recommend that you take a look at how term insurance for HNIs works differently in India.

Additionally, whether this plan is the right choice depends on your long-term financial goals and risk tolerance.

Disclaimer: SBI Life is not a partner insurer of Ditto. Our assessment here is completely independent and based solely on publicly available data and the evaluation framework we use for all insurers. At Ditto, we do not recommend ULIPs in general due to their structural inefficiencies compared to buying a term plan and investing separately. Our services are limited to retail term and health insurance products.

Frequently Asked Questions

Last updated on: