Overview

According to the IRDAI Annual Report 2024–25, pension and annuity products generated combined premiums of ₹1.67 lakh crore, accounting for nearly 18.87% of the Indian life insurance industry's total premium income. As retirement planning gains importance, choosing the right pension plan has become crucial.

This guide breaks down the most popular pension plans in India, including NPS, annuity plans, and retirement-focused products, to help you understand where each fits in your retirement strategy.

LIC Pension Plans: Jeevan Shanti and Saral Pension

1) LIC New Jeevan Shanti

A deferred annuity plan where you invest a lump sum today and start receiving a pension after a chosen deferment period. LIC New Jeevan Shanti is suited for those nearing retirement who want a predictable retirement income. There is no maturity benefit under this plan.

Key Features

2) LIC Saral Pension

An immediate annuity plan that begins pension payouts immediately upon purchase. Suitable for retirees seeking an immediate regular income. Saral Pension is a standardized product issued by IRDAI and offered by every life insurer.

Take Note: Pension plans are broadly classified as linked and non-linked. Linked pension plans are market-linked products, typically Unit Linked Insurance Plans (ULIPs)-based, where returns depend on fund performance.

Non-linked pension plans offer benefits that are not directly tied to market movements and may be structured as immediate annuities, deferred annuities, participating plans, or non-participating guaranteed-income plans.

National Pension System (NPS): Government-Backed Retirement Plan

National Pension System (NPS) is a Pension Fund Regulatory and Development Authority (PFRDA) regulated, market-linked retirement scheme that allows investors to choose their asset allocation and pension fund manager.

The scheme combines long-term wealth creation with retirement-income planning and offers attractive tax benefits. Unlike guaranteed pension plans, returns depend on market performance, making it better suited for investors with a long investment horizon and retirement-focused goals.

NPS offers tax benefits under multiple sections. You can claim deductions within the ₹1.5 lakh limit under 80CCD(1), an additional ₹50,000 under 80CCD(1B), and tax benefits on eligible employer contributions under 80CCD(2), subject to applicable conditions and tax regime rules.

NPS subscribers can choose from multiple PFRDA-registered pension fund managers and can switch between them when needed. There are 10 pension fund managers, including HDFC Pension Fund Management Ltd and LIC Pension Fund Ltd.

UPS, EPF & EPS: Important Retirement Alternatives

- Unified Pension Scheme (UPS): Available only to eligible Central Government employees covered under NPS. The Unified Pension Scheme offers an assured pension payout subject to prescribed conditions. The scheme provides a minimum assured pension of ₹10,000 per month after 10 years of qualifying service, with proportionate payouts available for service periods between 10 and 25 years.

- Employees' Provident Fund (EPF): This helps salaried employees build a retirement corpus through mandatory contributions from both employees and employers. Under EPF, employees contribute 12% (or 10% in eligible cases) of wages, while the employer contributes 8.33% toward EPS. Employees do not contribute directly to EPS.

- Employees' Pension Scheme (EPS): The scheme provides a monthly pension funded through employer contributions and government support. Employees earning up to ₹15,000 per month and contributing under EPF for a minimum period are eligible for the Employees' Pension Scheme.

Note: Under the old tax regime, investments in EPF, PPF, and certain eligible savings or annuity products may qualify for deductions under Section 80C, subject to the overall ₹1.5 lakh limit.

How to Select a NPS Fund Manager?

Private Insurer Annuity Plans: HDFC, ICICI, and SBI

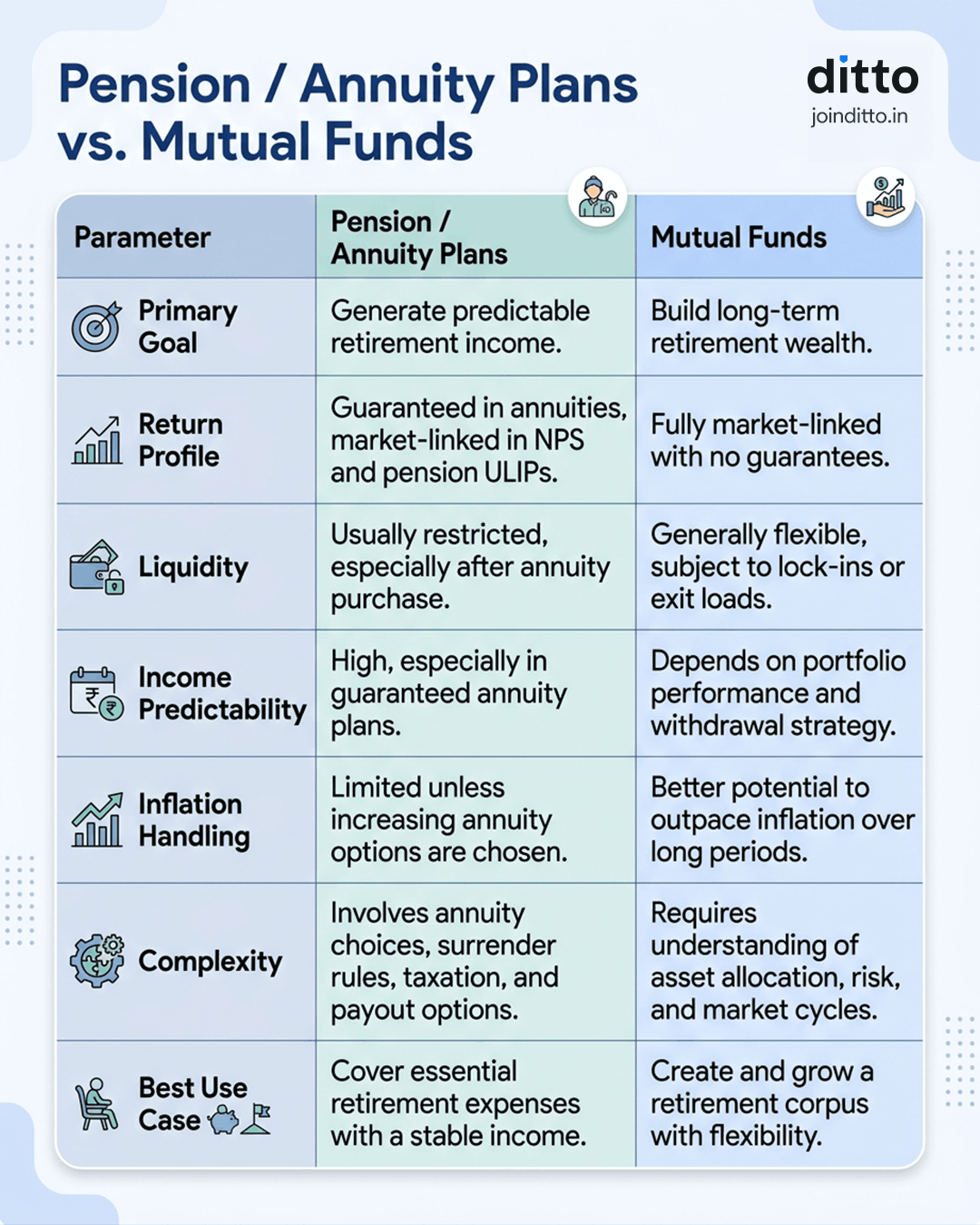

Pension Plans vs Mutual Funds: Which Is Better for Retirement?

Pension plans and mutual funds serve different retirement needs. Pension plans focus on creating a structured retirement income, while mutual funds primarily help build a retirement corpus.

For investors seeking a middle path, retirement-oriented mutual funds, such as those offered by most major Asset Management Companies (AMCs), can be worth considering. These funds typically follow a more balanced and conservative asset-allocation approach, gradually managing risk while aiming for long-term growth.

Take a look at the infographic, which compares pension/annuity plans with mutual funds.

How to Choose the Right Pension Plan for Your Needs

Accumulation vs Income

If retirement is years away, focus on building wealth through NPS, EPF, PPF, or mutual funds. Annuities make more sense as you get closer to retirement.

Need for Guaranteed Income

Use annuities to cover essential expenses such as food, utilities, rent, and healthcare, not your entire retirement corpus.

Liquidity Requirements

Keep a separate emergency fund. Pension and annuity products are not designed for easy and immediate access to money.

Tax Benefits & Employer Support

Maximize EPF, EPS, UPS, and NPS benefits first, especially if tax deductions are valuable for your situation.

Risk Tolerance

Use guaranteed products for stability and growth-oriented investments for long-term wealth creation.

Spouse Protection

Consider joint-life pension options if your spouse depends on your retirement income.

Inflation Protection

Retain some exposure to growth assets. Fixed pension income alone may lose purchasing power over time.

Note: Before choosing any pension plan, it helps to estimate how much retirement corpus you may actually need. Tools like the SEBI Annual Retirement Income Calculator and the NISM Retirement Calculator can help you project future expenses, inflation impact, required savings, and potential retirement income. This makes your planning more realistic and goal-driven.

Should You Buy a Pension Plan?

The right retirement strategy changes with age. What works in your 30s may be completely unsuitable in your 60s, so your pension planning should evolve as your financial goals, risk tolerance, and retirement timeline change.

- In Your 20s & 30s: Focus on building a retirement corpus. Market-linked options, such as NPS with higher equity allocation and equity mutual funds, offer better long-term growth potential.

- In Your 40s: Balance growth with stability. Hybrid funds, NPS Auto Choice, or a mix of equity and debt investments can help reduce risk while continuing to create wealth.

- In Your 50s & Near Retirement: Shift toward capital preservation and predictable income. Consider debt-oriented investments, Senior Citizens’ Savings Scheme (SCSS), PPF, high-quality fixed-income products, or deferred annuity plans for future pension income.

Did You Know?

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat on WhatsApp.

Conclusion

Pension plans have an important role in retirement planning. They can provide predictable income, reduce longevity risk, and create a financial safety net that continues even after your active earning years end.

- Use pension plans primarily for retirement income, not wealth creation.

- Build your retirement corpus first through vehicles such as NPS, EPF, PPF, and mutual funds.

- Consider annuity or pension products later to cover essential expenses like food, utilities, healthcare, and housing.

At Ditto, we believe insurance and investments work best when kept separate. Insurance should protect your family from financial risks, while investments should focus on growing wealth efficiently.

Retirement planning is highly personal. Risk tolerance, income needs, tax situation, retirement age, and family responsibilities all matter. Ditto is not a SEBI-registered investment advisor, so consider consulting a qualified financial advisor before making retirement investment decisions.

Our services are currently focused on health insurance and term life insurance, as these form the foundation of a strong personal financial plan and help protect against major financial risks.

Frequently Asked Questions

Last updated on: