Pension plans are retirement-focused financial products designed to help individuals build a corpus during their working years and convert it into a regular income after retirement.

Common retirement options in India include the National Pension System (NPS), Atal Pension Yojana (APY), saving schemes like Public Provident Fund (PPF), employer-linked benefits like Employees’ Provident Fund (EPF), and insurer-backed annuity plans.

Insurers like Life Insurance Corporation of India (LIC) offer annuity pension plans like LIC Jeevan Akshay VII, while pension plans by private insurers include HDFC Life Guaranteed Pension Plan. However, at Ditto, we generally encourage individuals to evaluate retirement planning in a broader context. For many people, this may include a combination of adequate insurance protection along with other investment options. This guide is for those exploring pension plans in India.

Retirement may feel distant today, but the cost of not planning for it can be enormous. With NPS assets under management reaching ₹15.95 lakh crore in 2026, more Indians are actively building retirement income instead of relying solely on savings or family support.

In the next few minutes, this guide will walk you through pension plans, their types, popular ones in India, and whether you need one.

Unsure whether or not a pension plan will align with your future needs? Book a free call or chat on WhatsApp with a Ditto advisor, and let us help you out.

What Is a Pension Plan And How Does It Work?

A pension plan is a retirement-focused financial product that helps create a regular income after retirement. You can either build a retirement corpus over time and later convert it into pension income, or invest a lump sum and receive periodic payouts.

Here’s how the product works:

Accumulation Phase: During your working years, you contribute regularly or invest a lump sum/policy premium to build a retirement corpus. The money grows through market-linked returns, bonuses, or other product-specific benefits, depending on the plan.

Distribution Phase: After retirement, the accumulated corpus is used to generate income. This can come through annuity payouts, lump sum withdrawals, or a guaranteed pension, depending on the retirement product chosen.

Note: Insurance-based pension plans often provide life cover during the accumulation stage, offering financial protection to your family in case of your death. At retirement, these plans typically require a part of the accumulated corpus to be used for purchasing an annuity that generates regular pension income.

Did You Know?

According to the IRDAI Annual Report 2024–25, pension and annuity products generated combined premiums of ₹1.67 lakh crore, accounting for nearly 18.87% of the Indian life insurance industry's total premium income. This highlights the growing focus on retirement planning among Indian savers.

Types of Pension Plans in India

Type

What It Means

How It Usually Works

Example

Government-Offered

Retirement schemes backed or regulated by the government.

You contribute during working years and receive a pension, annuity, or lump sum retirement corpus later.

NPS and PPF

Insurance-Based

Pension and annuity plans offered by life insurance companies.

You pay premiums regularly or a lump sum and receive a regular income after retirement.

Retirement plans and Saral Pension

Employer-Sponsored

Retirement benefits provided through an employer.

Employers and/or employees contribute during employment, with benefits paid on retirement or exit.

EPF

Insurance-based pension plans can be further classified into three broad categories:

Immediate annuities start pension payouts soon after investment.

Deferred annuities, where income begins after a chosen deferment period.

Take Note: IRDAI has introduced standardized insurance products to improve transparency and simplify comparisons across insurers. Saral Pension is one such immediate annuity plan that every life insurer in India must offer.

CTA

Key Features to Look For in a Pension Plan

Whether you are exploring HDFC pension plans or any other pension plans, here are the features to consider.

Guaranteed vs Market-Linked Returns: Choose between predictable income and growth potential. Guaranteed annuities offer certainty, while market-linked options like NPS can build a larger retirement corpus.

Annuity Option: The annuity choice determines your pension payout and what happens after death. Common options include life annuity and joint-life annuity.

Return of Purchase (ROP) Price: ROP returns the original investment to the nominees after death. While attractive, it usually results in a lower monthly pension than non-ROP options.

Inflation Protection: A fixed pension loses purchasing power over time. Consider increasing annuity options or maintaining a separate growth-oriented retirement portfolio.

Liquidity & Exit Rules: Many pension and annuity plans have limited withdrawal flexibility. You should review surrender conditions and exit restrictions in the benefit illustration before investing.

Payout Frequency: Check whether income is paid monthly, quarterly, half-yearly, or annually. Monthly payouts make it easier to manage monthly household expenses.

Tax Benefits & Taxation: Understand available tax deductions and how pension, annuity income, and withdrawals are taxed before making a decision. Premiums paid toward these plans qualify for tax deductions under Section 80CCC(old regime), subject to the overall ₹1.5 lakh limit under Section 80C.

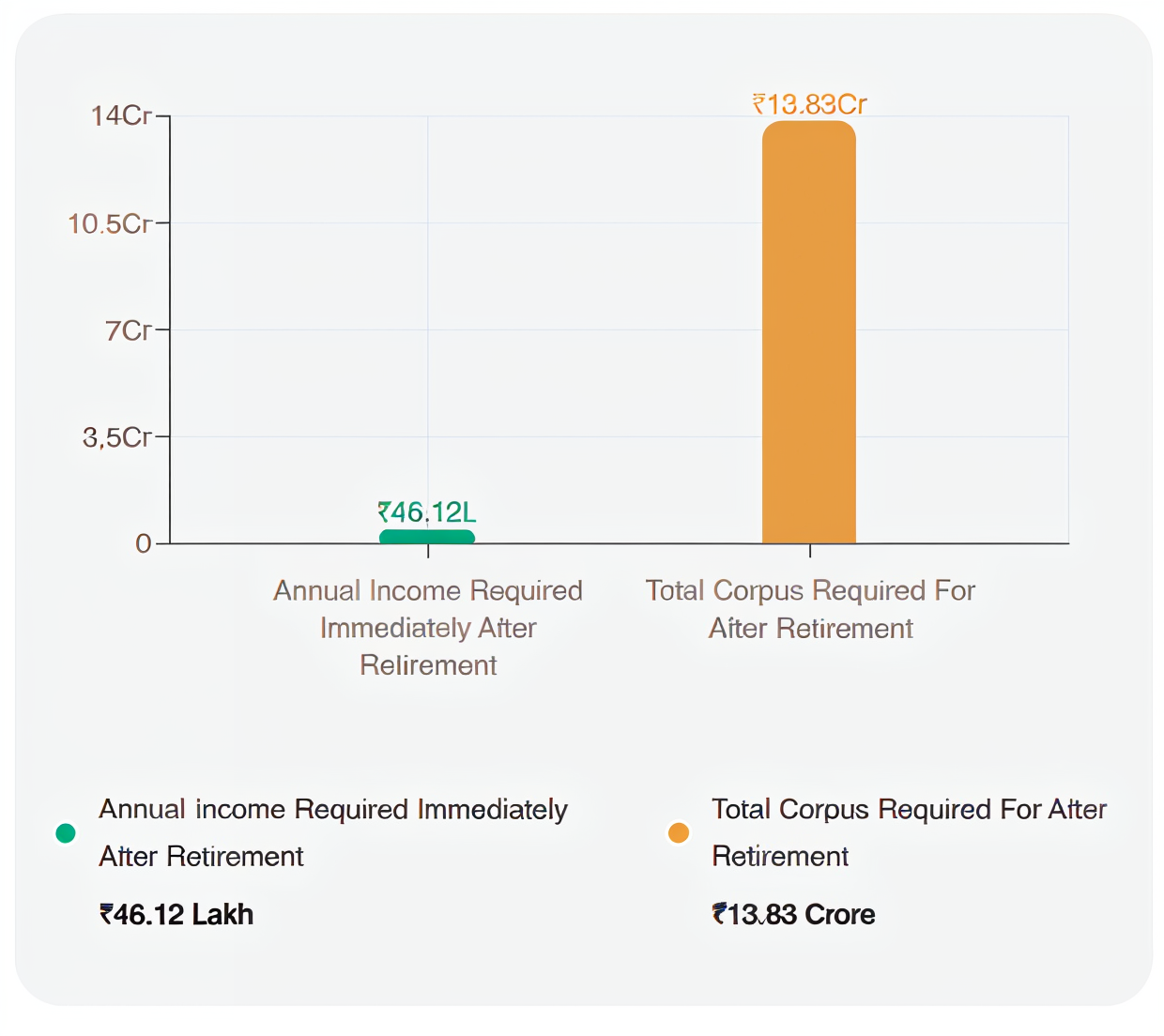

How to Calculate Your Retirement Corpus?

To calculate your retirement corpus, factors like expected retirement age, monthly expenses after retirement, life expectancy, existing savings, and anticipated investment returns are required.

A retirement calculator can help convert these assumptions into a target corpus and estimate how much you need to save regularly to achieve it. Let’s take an example to generate a personalized estimate.

Additionally, you can use the NISM Corpus Making Calculator to estimate the retirement corpus you may need for your future goals. This helps you to find out how much you must invest regularly to build that corpus over time.

Popular Pension Plans in India

01

National Pension System

A market-linked retirement scheme suitable for long-term corpus creation. It offers low costs, tax benefits, and professional fund management, though returns are not guaranteed.

02

Atal Pension Yojana

A government-backed pension scheme designed primarily for eligible workers in the unorganized sector. It provides a fixed pension, though the payout amount is relatively modest.

03

LIC Jeevan Akshay VII

An immediate annuity plan that converts a lump sum into guaranteed lifelong income. Suitable for retirees seeking pension income right away.

04

LIC New Jeevan Shanti

A deferred annuity plan that locks in annuity rates at purchase and starts pension payments later. LIC New Jeevan Shanti is best for those planning retirement income in advance.

05

HDFC Life Systematic Retirement Plan

A deferred annuity plan that allows systematic premium payments and offers guaranteed income options after retirement.

06

ICICI Pru Guaranteed Pension Plan

Provides immediate and deferred annuity choices with multiple payout structures, including joint-life and return-of-purchase-price options.

07

SBI Life Smart Annuity Plus

Offers guaranteed retirement income with flexible payout frequencies, immediate or deferred annuity options, and multiple annuity variants.

Note: The plans/schemes listed above are examples of well-known retirement products, not personalized recommendations.

Should You Buy a Pension Plan?

A pension plan deserves consideration if retirement is approaching and you want a predictable income stream for life. It can also suit those who prefer not to manage investments actively during retirement.

Additionally, a joint-life annuity option can help ensure income continuity for a spouse. If you already have adequate liquid savings and growth-oriented investments, a pension plan can serve as a stable income foundation for people who are worried about interest rate fluctuations. Finally, it may be useful for covering essential monthly expenses through guaranteed and dependable cash flows.

How Do Pension Plans Compare to a Combination of Term Insurance and Systematic Investment Plans (SIPs)?

The two are not competing products, but can be strategized well. A pension plan can make sense if you prefer a structured approach to retirement planning and value predictable income after retirement. It is particularly useful for those who want a hands-off solution without actively managing investments or making ongoing portfolio decisions.

On the other hand, a term insurance plan combined with separate investments offers greater flexibility, liquidity, and control over wealth creation. The need for term plans is decided based on working years left, loans and liabilities, and financial dependents. The right choice depends on your financial discipline, risk appetite, retirement goals, and whether you prioritize guaranteed income or long-term growth potential.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 24,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat on WhatsApp.

Conclusion

A pension plan can play an important role in retirement security, especially for those who value predictable income and financial stability. The right choice varies person to person.

Government-Offered: Works well for salaried, self-employed, government employees, and informal-sector workers.

Insurance-Based: People seeking a predictable and guaranteed retirement income.

Employer-Sponsored: Employees in the organized sector with workplace retirement benefits.

While pension planning is important, Ditto’s services are limited to health insurance and term life insurance. Those looking to build retirement wealth may also consider the combination of adequate term insurance and disciplined investments through SIPs, which can offer greater flexibility and long-term growth potential depending on their financial goals. If you are looking for investment advice or retirement planning advice, consult a SEBI-registered advisor.

Frequently Asked Questions

What is a pension plan, and how does it work in India?

A pension plan is a retirement-oriented financial product that helps you build a corpus during your earning years and convert it into a steady income after retirement. During the accumulation phase, you invest regularly or make a lump-sum contribution, and the money grows. After retirement, the distribution phase begins, where the accumulated corpus provides income. You can use a pension plan calculator to estimate how much money you need to save today to maintain your current lifestyle after retirement. Young people can explore plans like NPS or PPF, while senior citizens can opt for the Senior Citizens’ Savings Scheme (SCSS).

What are the main types of pension plans available in India?

Pension plans in India can broadly be grouped into three categories. Government-backed options include the National Pension System (NPS), Atal Pension Yojana (APY), Public Provident Fund (PPF), and Senior Citizen Savings Scheme (SCSS). Insurance-based pension plans include immediate annuities, deferred annuities, and pension ULIPs offered by life insurers. Employer-sponsored retirement schemes include the Employees’ Provident Fund (EPF) and Employees’ Pension Scheme (EPS) for salaried workers. Each option serves a different purpose. The right choice depends on factors such as your age, income stability, risk appetite, and retirement income requirements.

Is an NPS or an LIC pension plan better for retirement planning?

NPS and LIC pension plans are designed for different retirement needs. NPS is a market-linked retirement scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It offers flexibility, low costs, and the potential for higher long-term growth through professionally managed investments. LIC pension plans, on the other hand, focus on guaranteed income and predictability. Plans such as LIC Jeevan Akshay VII provide fixed annuity payouts for life, making them attractive for retirees seeking certainty. The better option depends on whether you prioritize guaranteed income or long-term wealth creation.

What tax benefits are available on retirement plans in India?

Tax benefits on retirement plans depend on the product chosen and the tax regime you follow. Under the old tax regime, investments in EPF, PPF, SCSS, and certain eligible savings or annuity products may qualify for deductions under Section 80C, subject to the overall ₹1.5 lakh limit. Contributions to eligible pension or annuity plans offered by insurers may qualify under Section 80CCC, which shares the same combined limit. NPS offers additional tax advantages under Section 80CCD, including an extra deduction of up to ₹50,000 under Section 80CCD(1B), subject to applicable conditions.

Why are health insurance, term insurance, and an emergency fund important for retirement planning?

Retirement planning is not just about earning higher returns. It is also about protecting your retirement corpus from unexpected setbacks. A medical emergency, loss of income, death of an earning member, or sudden cash requirement can force you to withdraw long-term investments at the wrong time. That is why every retirement plan should rest on three foundations: adequate health insurance to cover medical expenses, term life insurance to protect dependents during earning years, and an emergency fund for short-term financial shocks. These safeguards help your retirement corpus remain invested, compound over time, and support long-term financial security.

What is Atal Pension Yojana, and who should invest in it?

The Atal Pension Yojana (APY) is a government-backed pension scheme launched in 2015 to provide retirement security, especially for workers in the unorganized sector. Under APY, subscribers receive a guaranteed monthly pension ranging from ₹1,000 to ₹5,000 from age 60. Joining is subject to eligibility criteria, including age 18–40, an eligible bank/post office account, and non-income-taxpayer status. Contributions are automatically deducted from a linked savings bank account. APY is particularly suitable for daily-wage earners, self-employed individuals, small business owners, and workers who do not have access to employer-sponsored retirement benefits or formal pension schemes.

What is the Saral Pension Plan introduced by IRDAI?

Saral Pension is a standardized immediate annuity plan introduced by IRDAI to make retirement income products simpler and easier to compare. Every life insurer in India is required to offer this product with a common structure and core features. The standardization helps eliminate confusion caused by varying annuity products and complex policy terms across insurers. Since the plan follows uniform guidelines, buyers can focus on comparing annuity rates and service quality rather than product features. Saral Pension is best suited for retirees who want a simple, transparent, and guaranteed source of income without dealing with complicated retirement products.

Should a pension plan be the first retirement product I buy?

For most working professionals, the answer is usually no. Before investing in a pension or annuity plan, it is important to build a strong financial foundation. This includes adequate health insurance, term life insurance if you have dependents, and an emergency fund. These safeguards help protect your retirement savings from unexpected medical expenses, income disruptions, or emergencies. Once these essentials are in place, products such as NPS, EPF, PPF, and mutual funds can play a larger role in retirement planning. Pension and annuity plans often become more relevant closer to or after retirement, when a stable income becomes a priority.

What returns can you expect from different pension plans?

Immediate annuity plans generally provide an equivalent yield of around 5% to 7%, depending on your age and the annuity option selected. Deferred pension plans may show higher projected returns because the corpus gets more time to grow before payouts begin. Guaranteed pension plans offer stability and a predictable income. Pension ULIPs may generate net returns of roughly 5.5% to 6.5% based on an assumed 8% gross return after charges. As of now, the PPF offers 7.1% interest, the EPF offers 8.25% interest, and the SCSS provides 8.2% interest.

What should I do for retirement planning at my age?

Retirement planning looks different at every stage of life. In your 20s, focus on starting early, building investing habits, and securing health insurance. In your 30s, increase investments, create an emergency fund, and buy term insurance if you have dependents. In your 40s, reassess retirement goals, boost retirement contributions, and reduce high-cost debt. In your 50s, focus on protecting your accumulated wealth and planning how retirement savings will generate income. After 60, prioritize stable cash flow, healthcare planning, liquidity, and financial security for both you and your spouse rather than chasing higher returns.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.