Quick Overview

If you’ve ever been pitched the ICICI Pru Signature Plan, chances are that you’ve heard that your entire premium gets invested.

And all of this is technically true on paper. But what most people don’t realize is that ULIPs don’t become cheap just because allocation charges are zero. There are still multiple ongoing costs, and they quietly reduce your returns over time.

In this ICICI Pru Signature review, we break down how the plan actually works, where the costs are hidden, and whether it truly delivers better returns or just looks good on paper.

What Is the ICICI Pru Signature Plan?

The ICICI Pru Signature is a ULIP that works as follows:

- You pay a premium regularly.

- Your entire premium is invested in funds upfront (no allocation charge).

- At the same time, the insurer provides a life cover (sum assured).

Key Plan Details

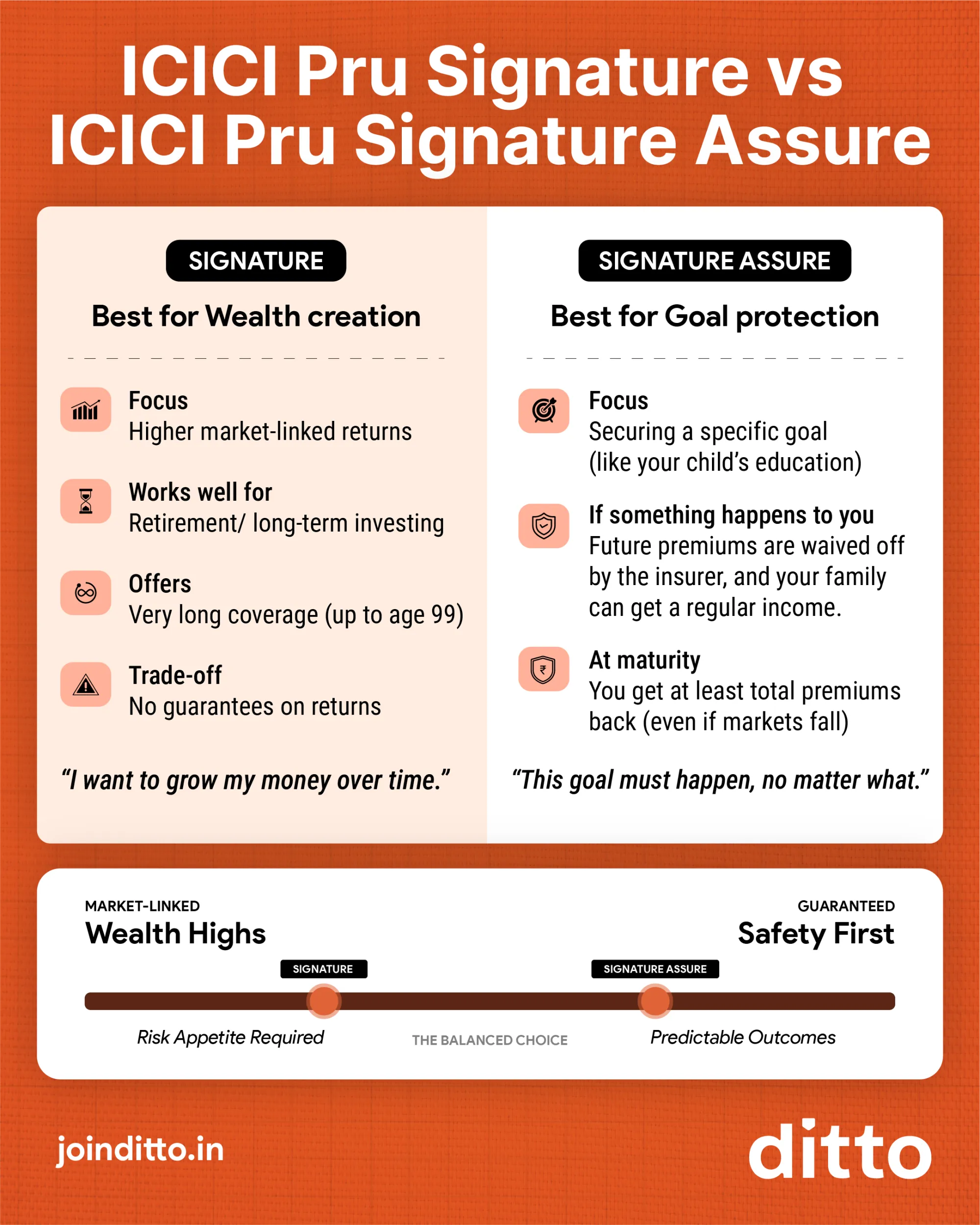

ICICI Pru Signature vs ICICI Pru Signature Assure

For more details, you can also check out our guide on ICICI Pru Signature Assure.

Fund Options, Portfolio Strategies & Wealth Boosters

Fund Options

The ICICI Signature Plan offers 25+ funds across different asset classes. You can broadly choose among equity (high risk, high return potential), debt (lower risk, stable returns), and balanced funds (a mix of equity and debt). For more details, you can go through pages 13 to 19 of the official ICICI Pru Signature policy brochure.

Portfolio Strategies

This is one of the key unique selling points of the ICICI Prudential Signature Plan. Instead of just picking funds, you can also choose how your portfolio is managed over time.

Fixed Portfolio Strategy (Do-It-Yourself)

Lifecycle Strategy (Auto-Pilot Mode)

Trigger Portfolio Strategy (Market-Timing Linked)

Target Asset Allocation Strategy (Disciplined Rebalancing)

Wealth Boosters

The ICICI Pru Signature rewards you for staying invested long-term through wealth boosters. 1.75% of your fund value is added as extra units at the end of the 10th year, and 2.5% is added every 5 years from the 15th year onwards.

Charges, NAV, & Returns

Charges

- Fund Management Charge (FMC): Up to 1.35% annually.

- Policy Administration Charge: 0.5% monthly (capped at ₹500/month).

- Mortality Charges: Depend on age and sum assured, and are deducted monthly.

- Discontinuance Charges: Up to 6% of premium/fund value (subject to caps) and applicable if you exit early.

Return of Mortality & Policy Administration Charges at Maturity

Net Asset Value (How Your Investment Value Is Calculated)

NAV is the price of one unit of your ULIP fund. It goes up or down based on market and fund performance, as well as FMC deductions. So even if the market performs well, charges reduce the net growth reflected in the NAV. While it is often presented as a “clean growth number” because it already accounts for FMC, it still doesn’t show the full impact of charges clearly.

Returns (Illustration from Policy Brochure)

For a 35-year-old paying an annual premium of ₹1 lakh, a premium payment term of 5 years, and a policy term of 15 years, here’s what your returns typically look like:

These 4% and 8% gross returns are mandated by IRDAI guidelines and are not actual expected returns.

Pros, Cons & Should You Invest in ICICI Pru Signature?

Should You Invest in ICICI Pru Signature?

You can consider the ICICI Signature Plan if:

- You prefer a structured, disciplined approach to investing.

- A combination of insurance protection and market-linked investment is appealing.

- You’re okay with investing for a long-term horizon of 10-15+ years.

However, if the goal is to maximize returns with full flexibility, this type of bundled product may feel restrictive due to lock-in and charges. Those who value simplicity and transparency often find standalone investments, such as mutual funds, easier to track and optimize.

Additionally, when the primary objective is pure life coverage, a term insurance plan typically offers much higher coverage at a lower cost compared to bundled insurance-investment products. For more details, refer to our detailed guide on ULIPs vs. term insurance.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Frequently Asked Questions

ICICI Prudential Customer Reviews

Last updated on: